Downloaded 81 times

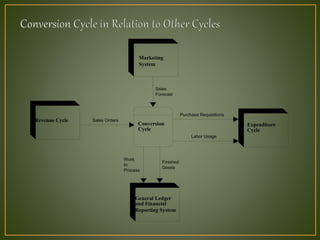

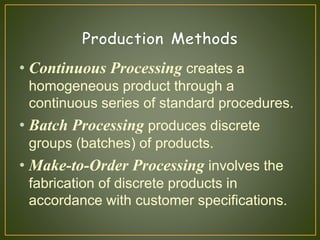

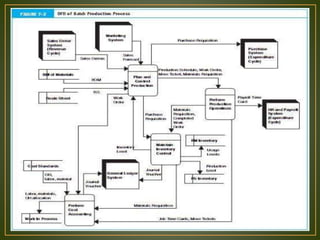

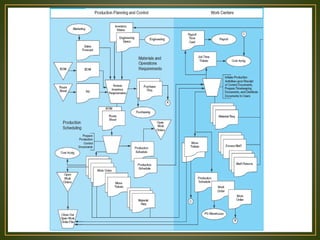

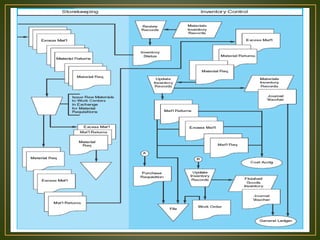

The document discusses the conversion cycle in traditional production processes and accounting. It describes the key elements and procedures of the physical production system and cost accounting information system. These include production scheduling, bills of materials, route sheets, move tickets, and material requisitions that control inventory and track costs. Shortcomings of traditional accounting in lean manufacturing are also noted.