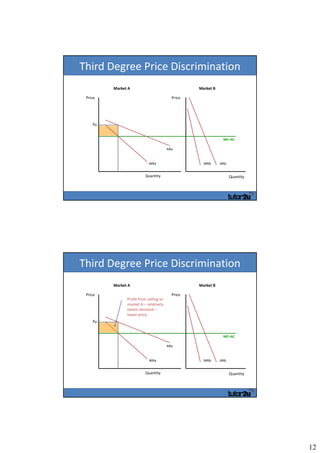

This document discusses the concept of price discrimination, which involves a firm charging different prices to different consumers for the same good or service. It provides definitions and key conditions for price discrimination, including that the firm must have some control over prices. It also gives examples of different degrees of price discrimination, including perfect 1st degree discrimination, 2nd degree excess capacity pricing, and 3rd degree market segmentation. The document outlines some potential advantages of price discrimination and notes that in practice, factors beyond just demand elasticity can influence price differences. It concludes by providing links to additional resources on the topic.

![Eco 6th Lecture[1]](https://cdn.slidesharecdn.com/ss_thumbnails/eco6thlecture1-1253256517118-phpapp03-thumbnail.jpg?width=640&height=640&fit=bounds)