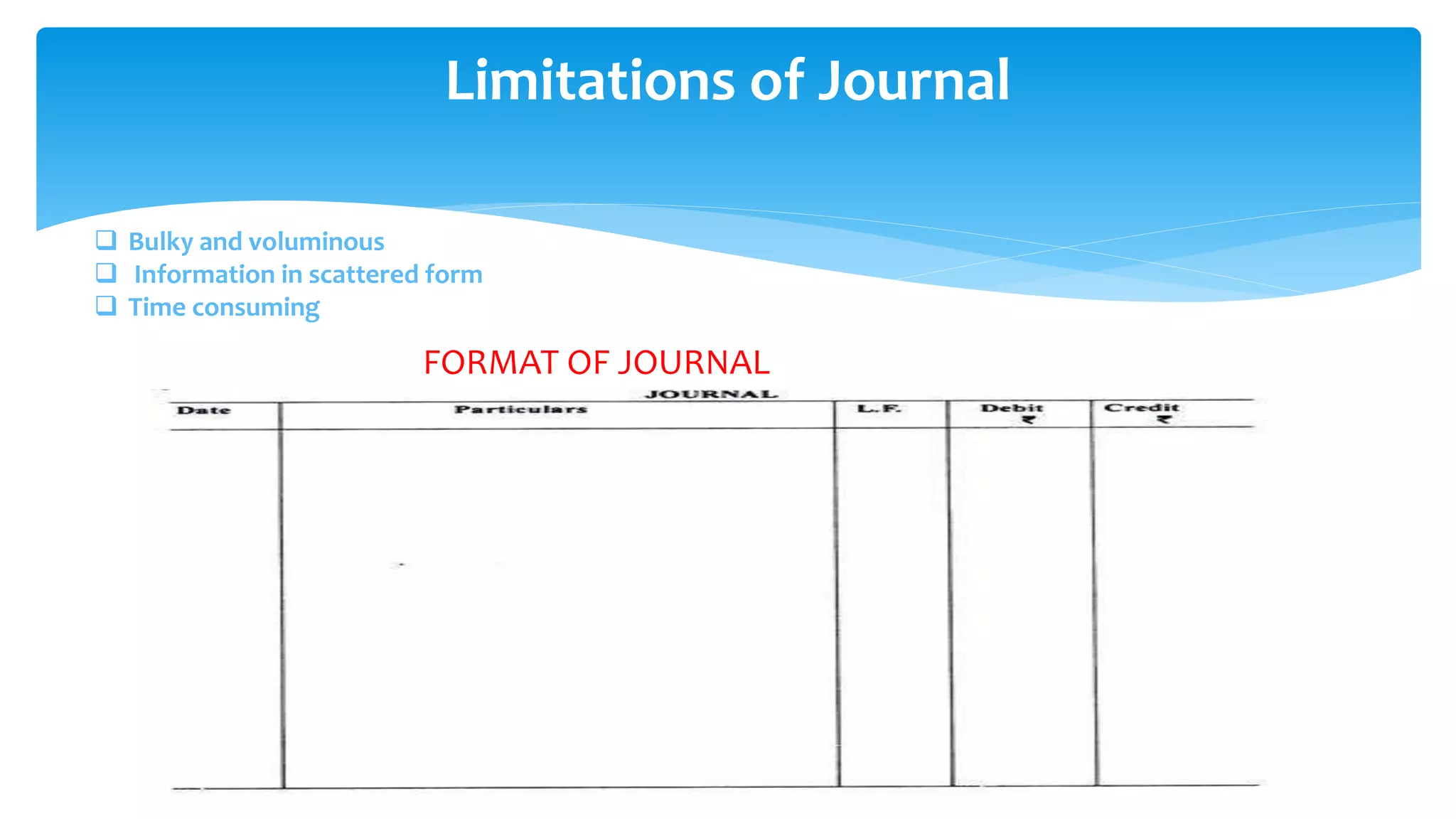

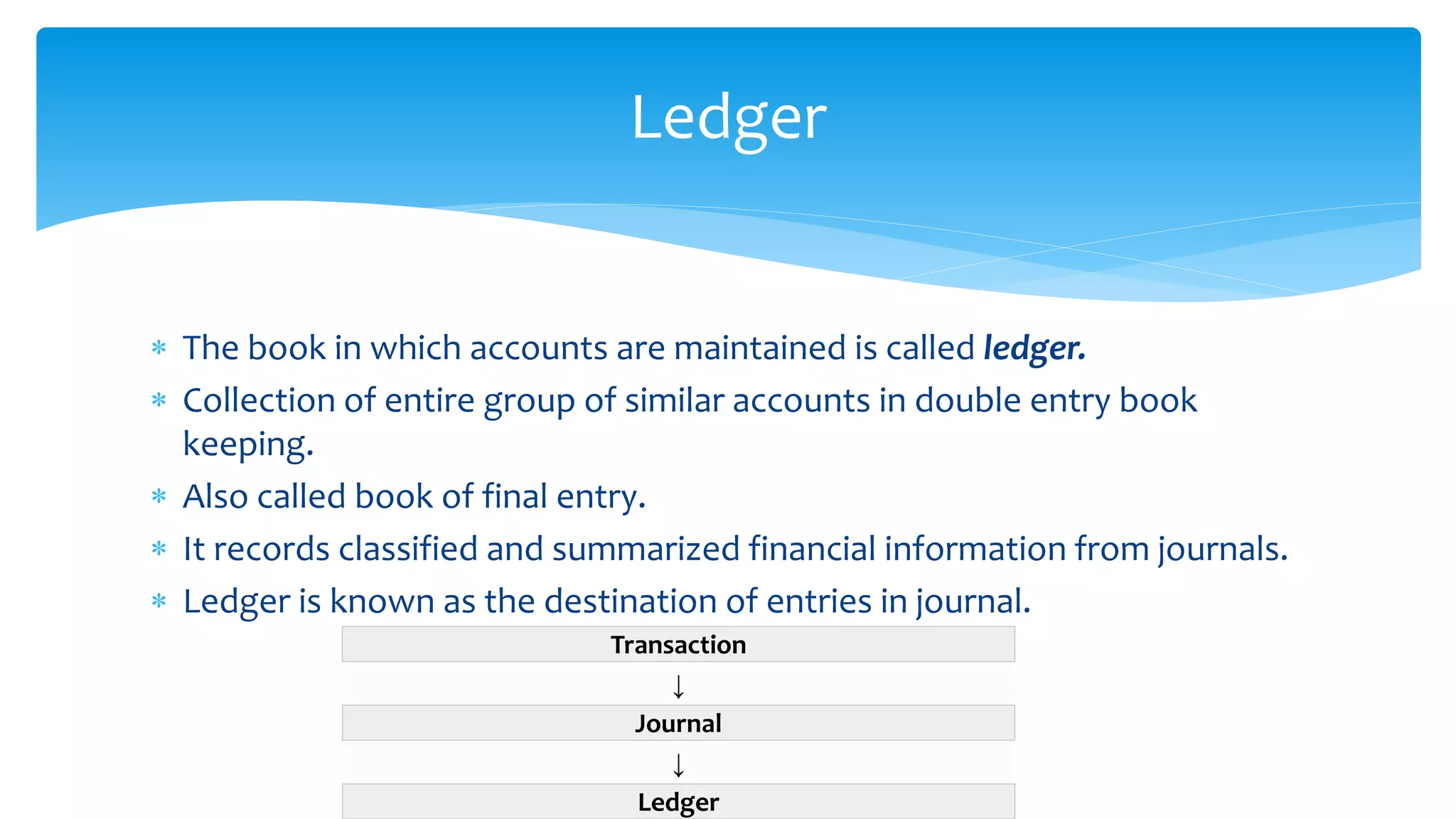

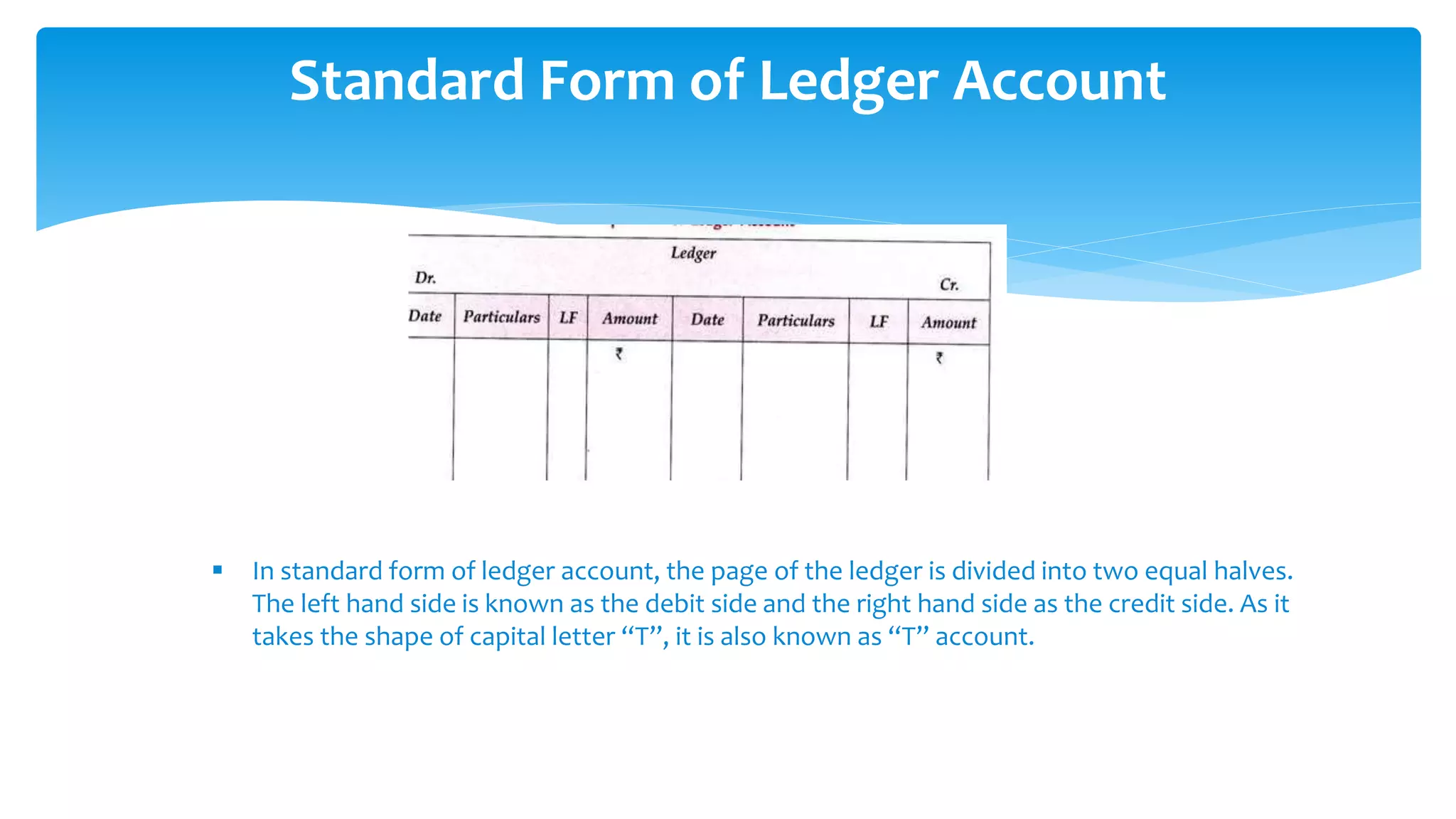

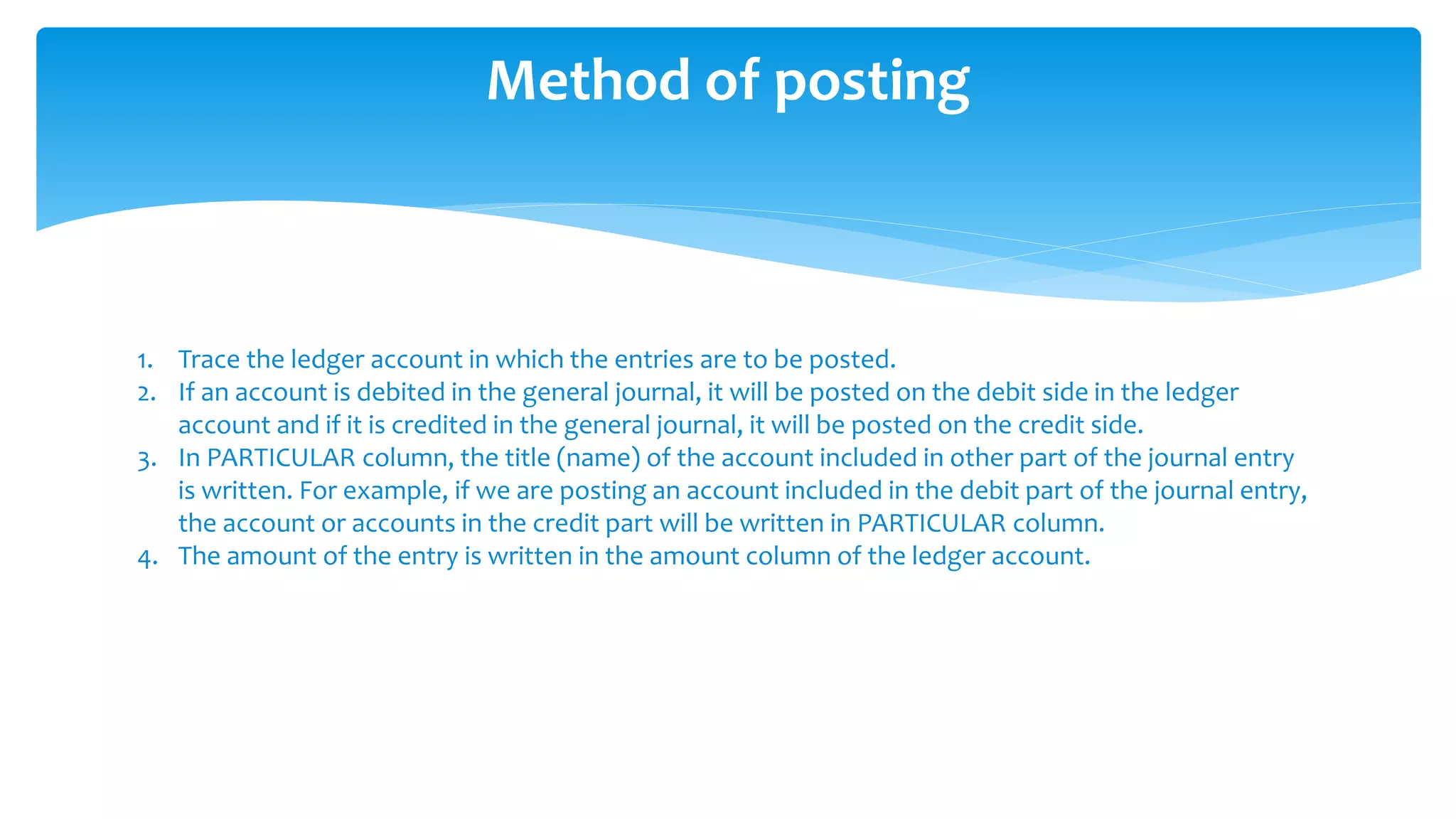

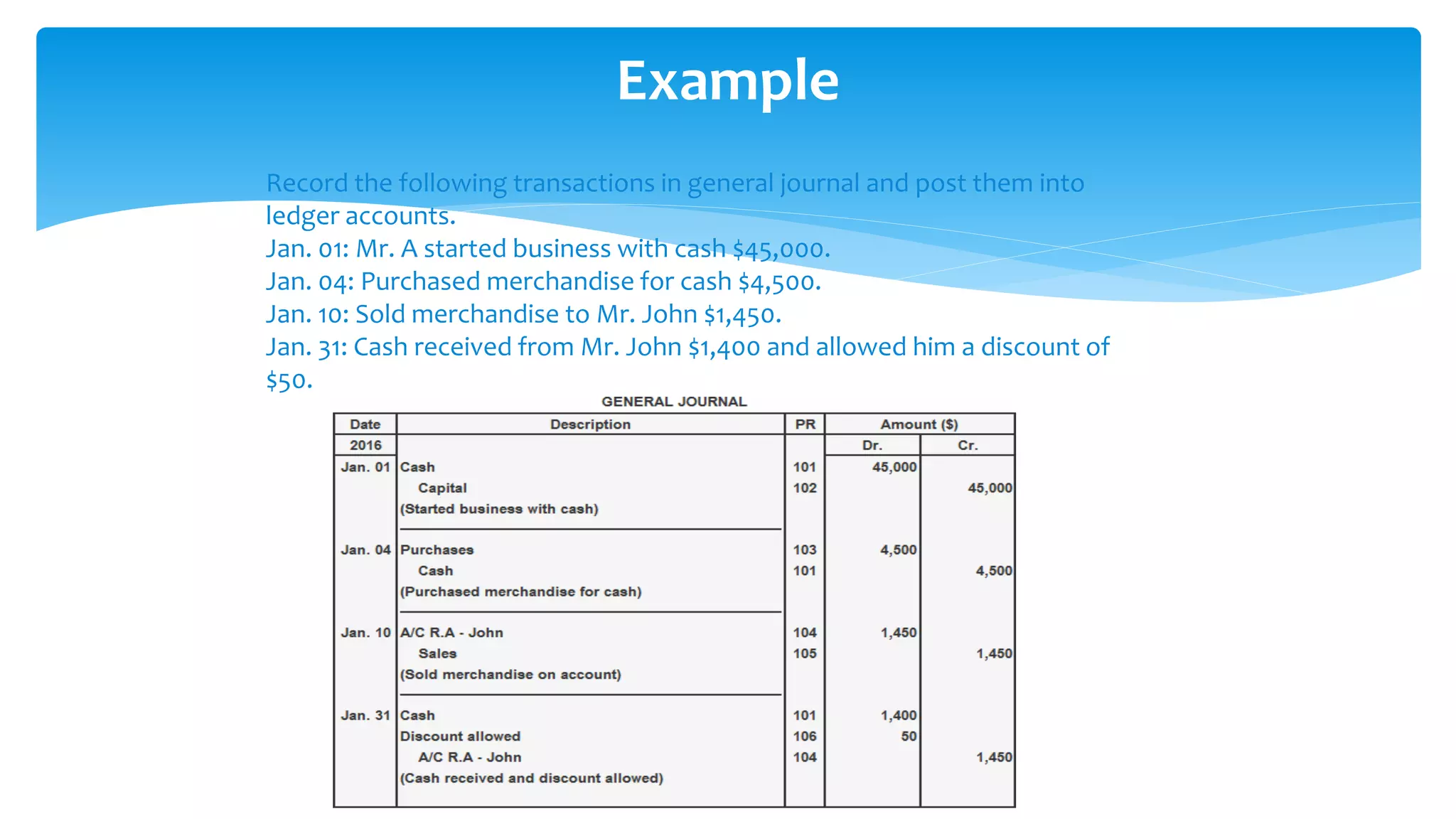

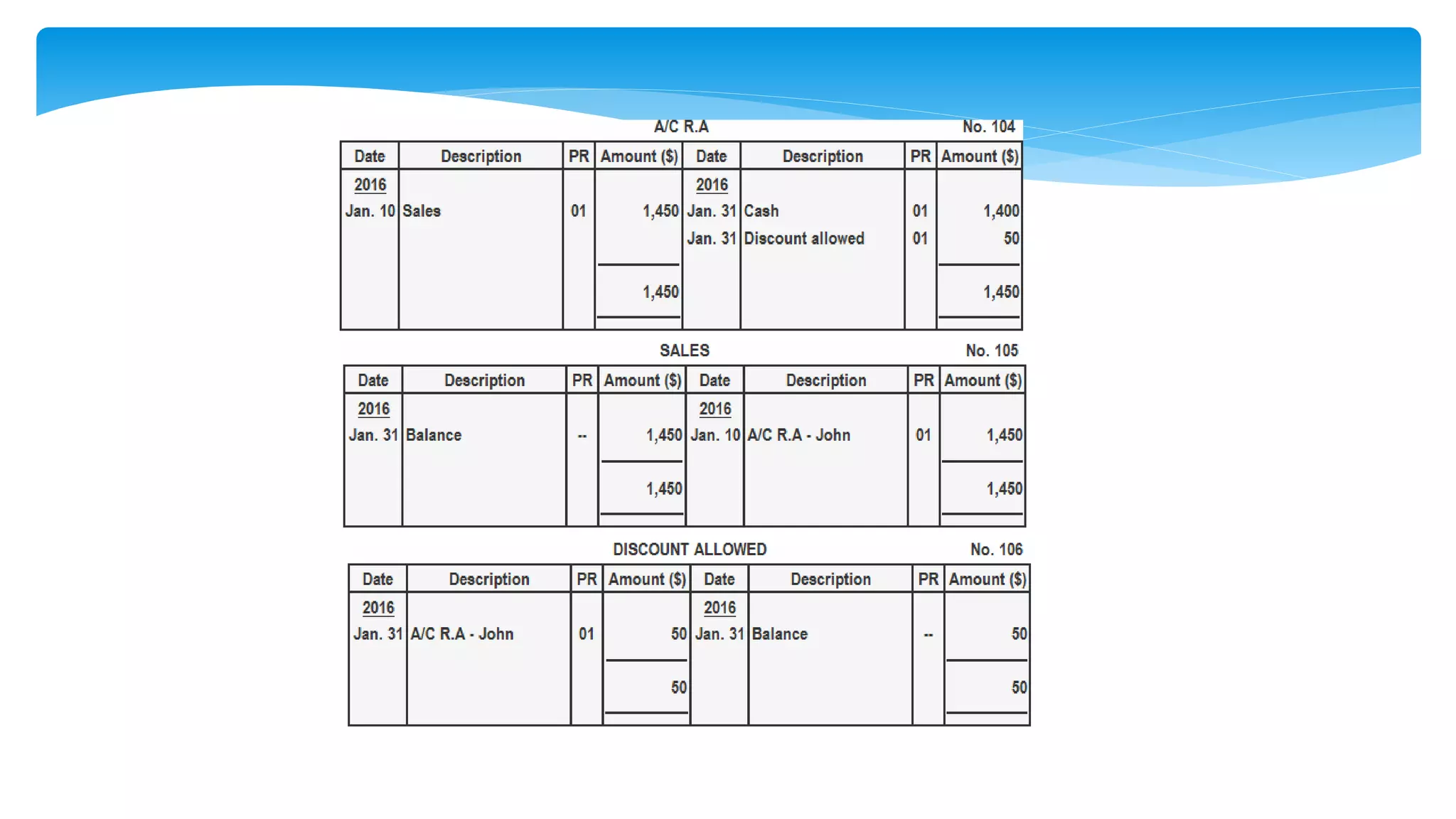

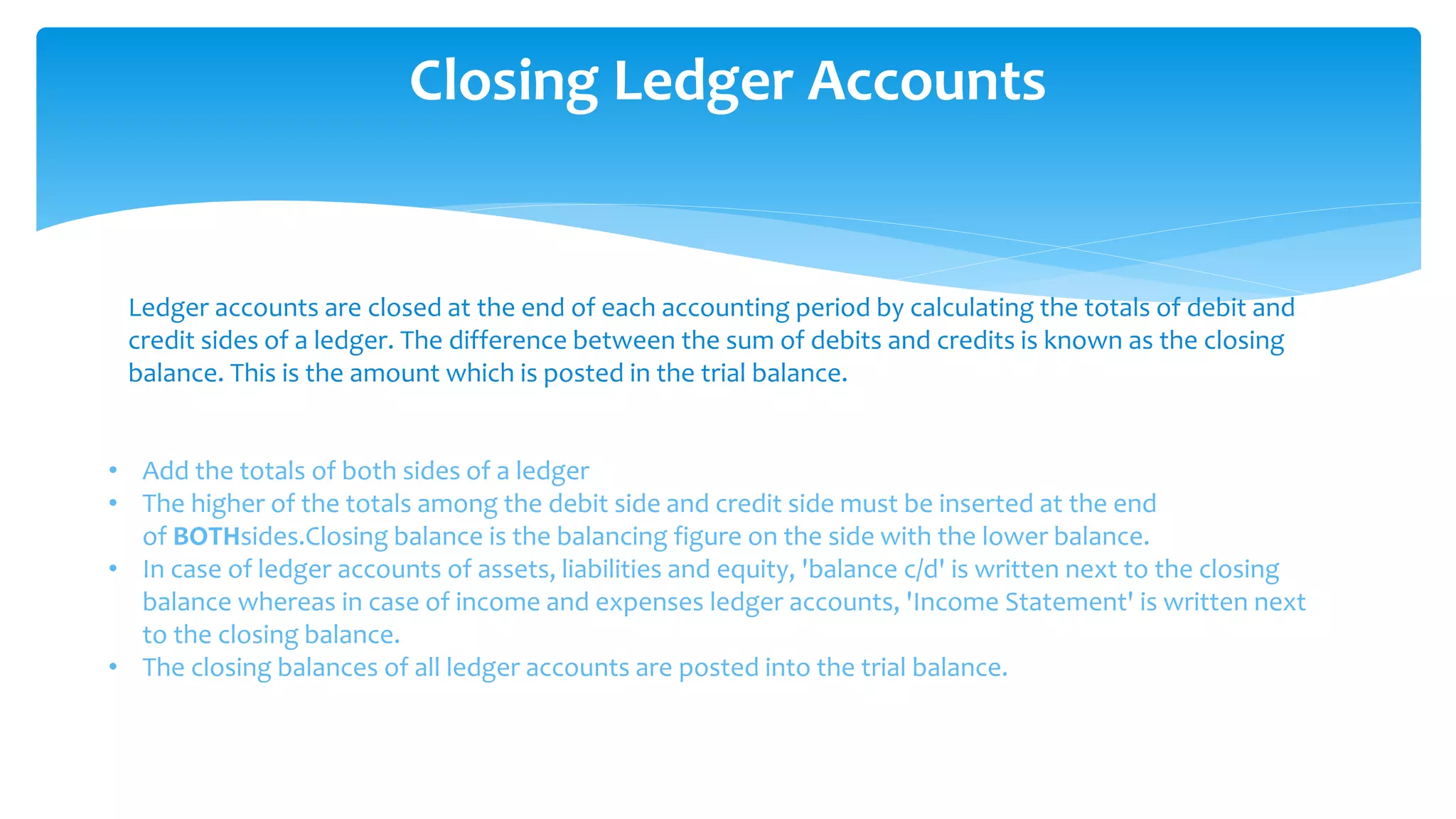

The document provides an overview of accounting, detailing the systematic process of recording and summarizing financial transactions through methods such as double entry accounting. It explains essential components like journals and ledgers, including their advantages and limitations, as well as how to prepare a trial balance for accurate financial reporting. It also highlights the historical background of double entry systems and key accounting terms, emphasizing the importance of accurate record-keeping in business finance.