Downloaded 81 times

![© Michael Allison. Author’s permission required for external use.

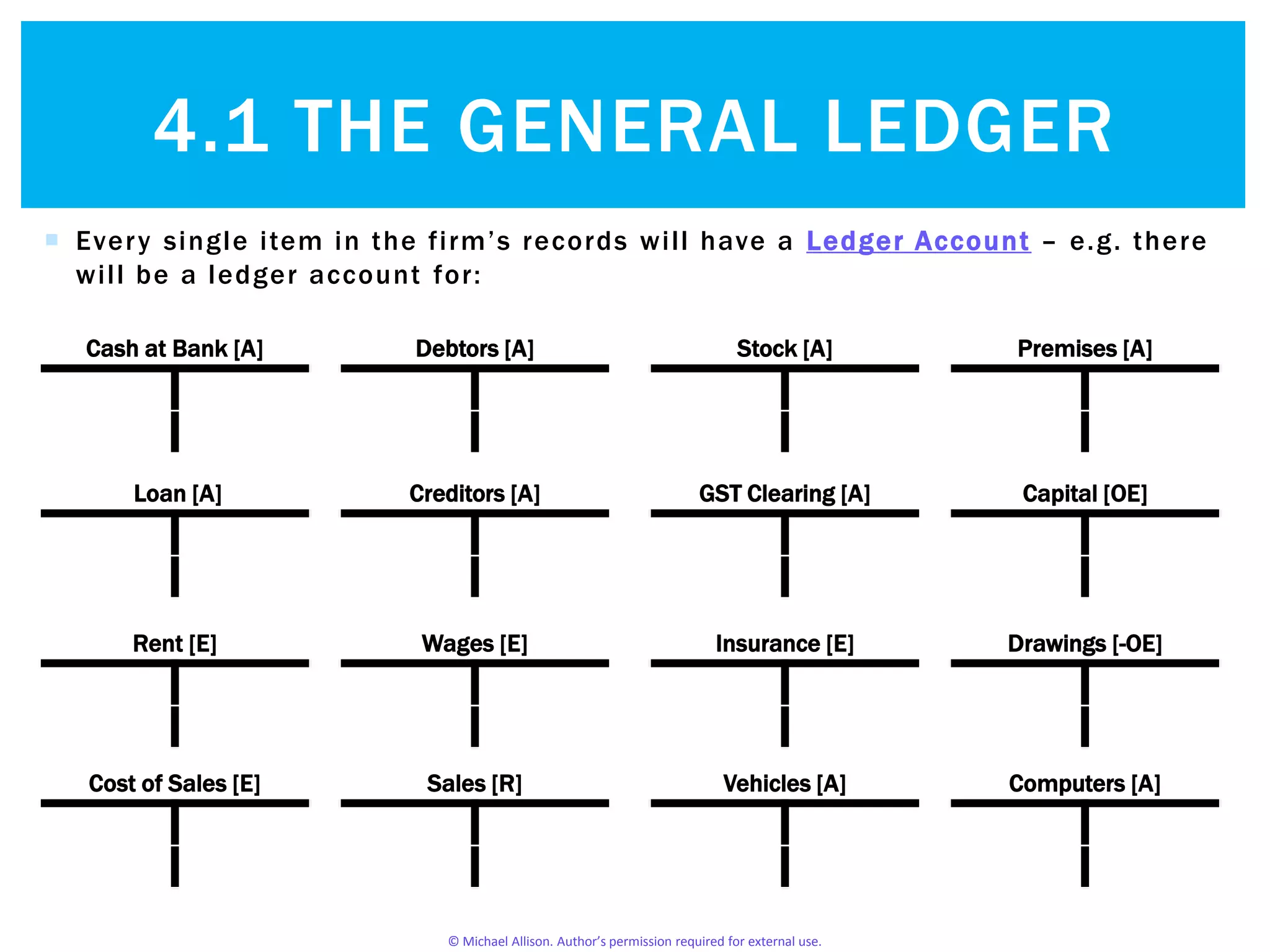

Every single item in the firm’s records will have a Ledger Account – e.g. there

will be a ledger account for:

Cash at Bank [A] Debtors [A] Stock [A] Premises [A]

Loan [A] Creditors [A] GST Clearing [A] Capital [OE]

Rent [E] Wages [E] Insurance [E] Drawings [-OE]

Cost of Sales [E] Sales [R] Vehicles [A] Computers [A]

4.1 THE GENERAL LEDGER](https://image.slidesharecdn.com/4-150225161313-conversion-gate01/75/4-1-The-General-Ledger-6-2048.jpg)

![© Michael Allison. Author’s permission required for external use.

Collectively, all of the Ledger Accounts are called the General Ledger

4.1 THE GENERAL LEDGER

The General Ledger

Cash at Bank [A] Debtors [A] Stock [A] Premises [A]

Loan [A] Creditors [A] GST Clearing [A] Capital [OE]

Rent [E] Wages [E] Insurance [E] Drawings [-OE]

Cost of Sales [E] Sales [R] Vehicles [A] Computers [A]](https://image.slidesharecdn.com/4-150225161313-conversion-gate01/75/4-1-The-General-Ledger-7-2048.jpg)

The document discusses the general ledger's role in accounting, emphasizing that balance sheets are not created after every transaction, but rather at the beginning and end of a period. It explains that the general ledger comprises various ledger accounts for all financial records of a firm. Additionally, it outlines the process of recording financial transactions within these accounts.