Downloaded 150 times

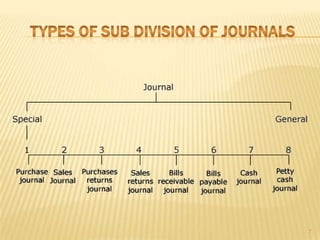

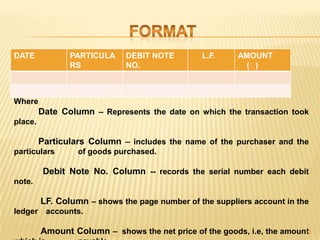

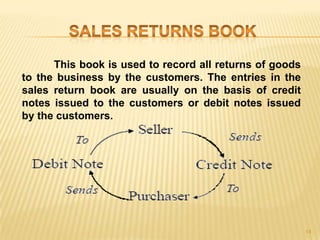

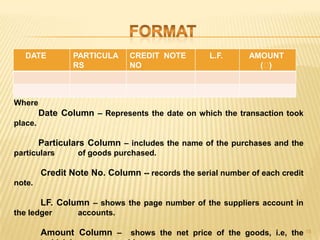

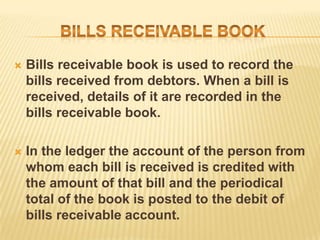

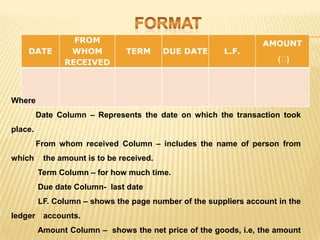

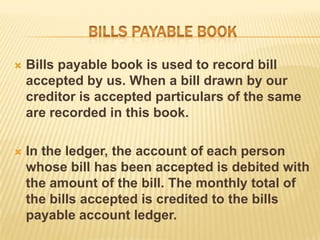

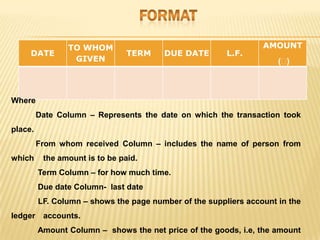

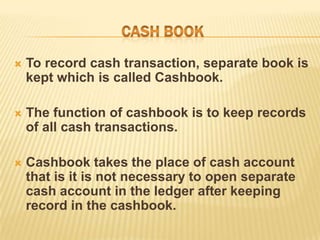

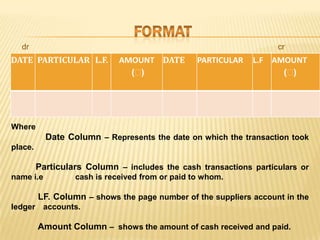

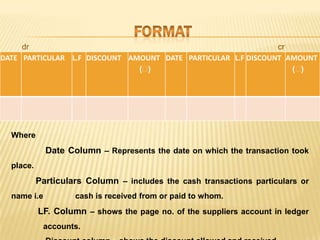

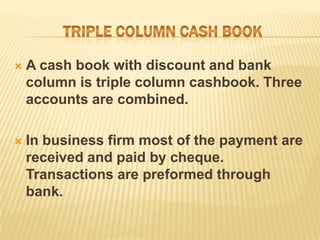

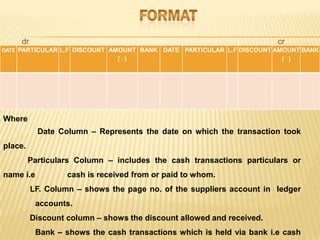

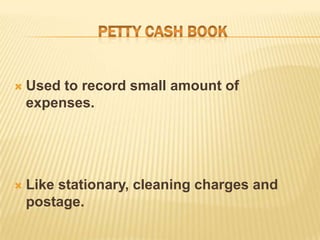

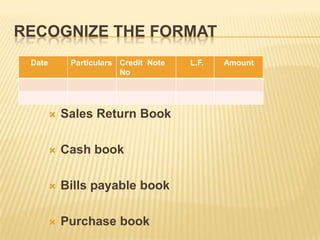

This document provides an overview of various accounting journals used to record business transactions. It discusses that journals are the primary record of transactions and may be subdivided for large businesses. It then explains that subsidiary journals were introduced to simplify recording of numerous transactions classified by type. Various journals are described, including purchases journal, sales journal, purchases returns book, sales returns book, bills receivable book, bills payable book, cash book including simple, double and triple column variations, and petty cash book. Their purpose and format including standard columns is outlined for each journal.

![Jammu ford[1]](https://cdn.slidesharecdn.com/ss_thumbnails/jammuford1-131101022912-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)