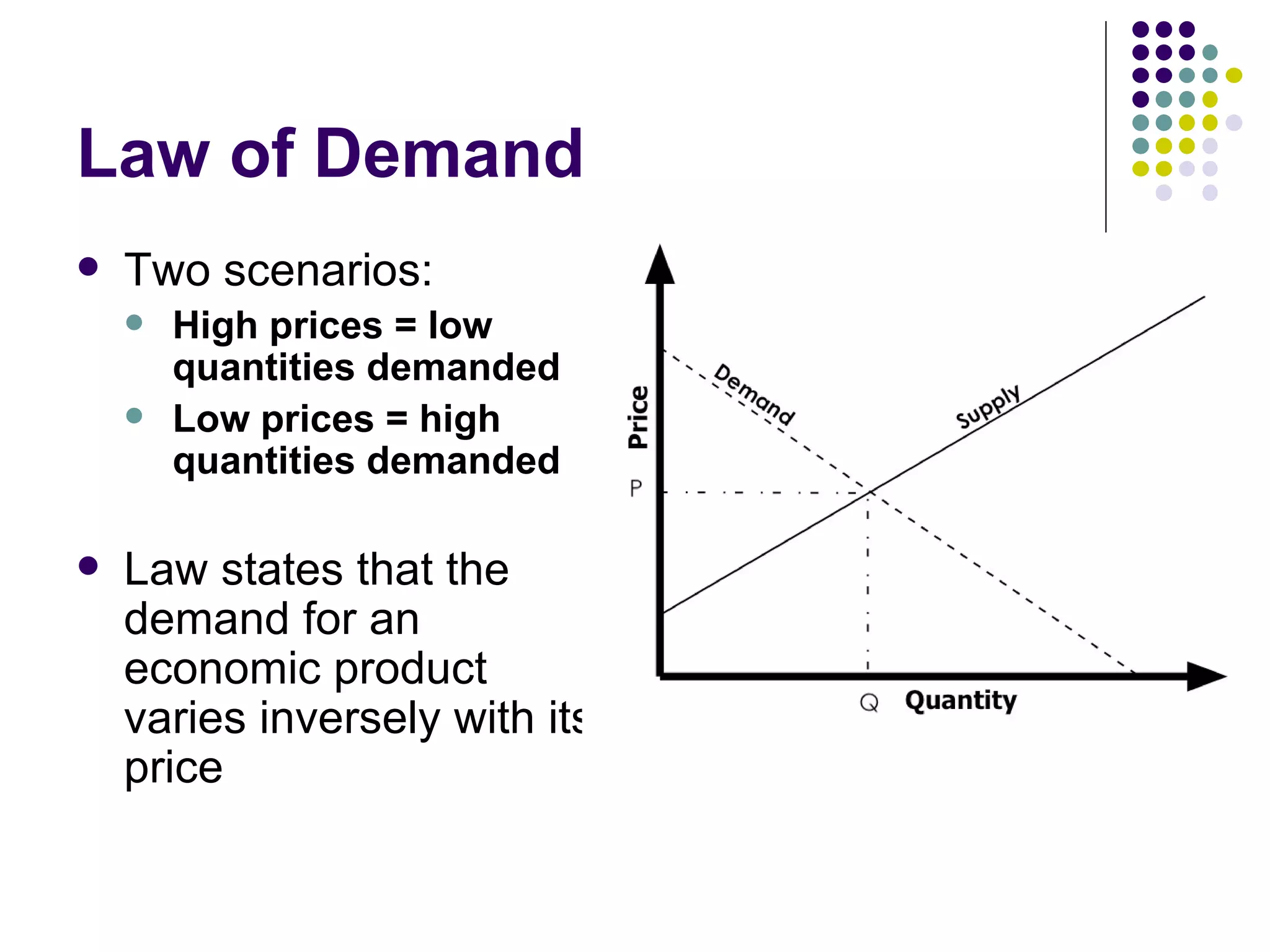

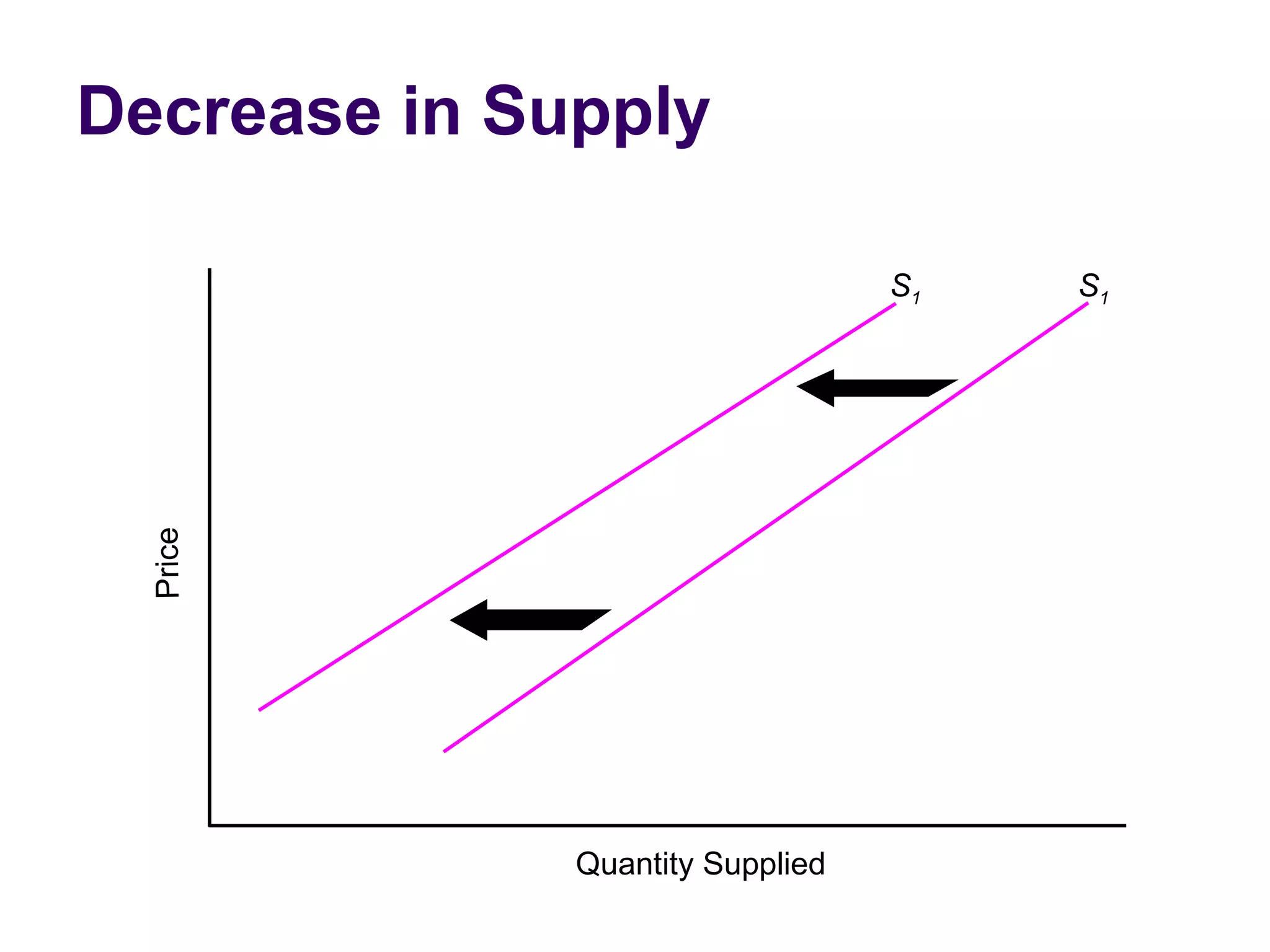

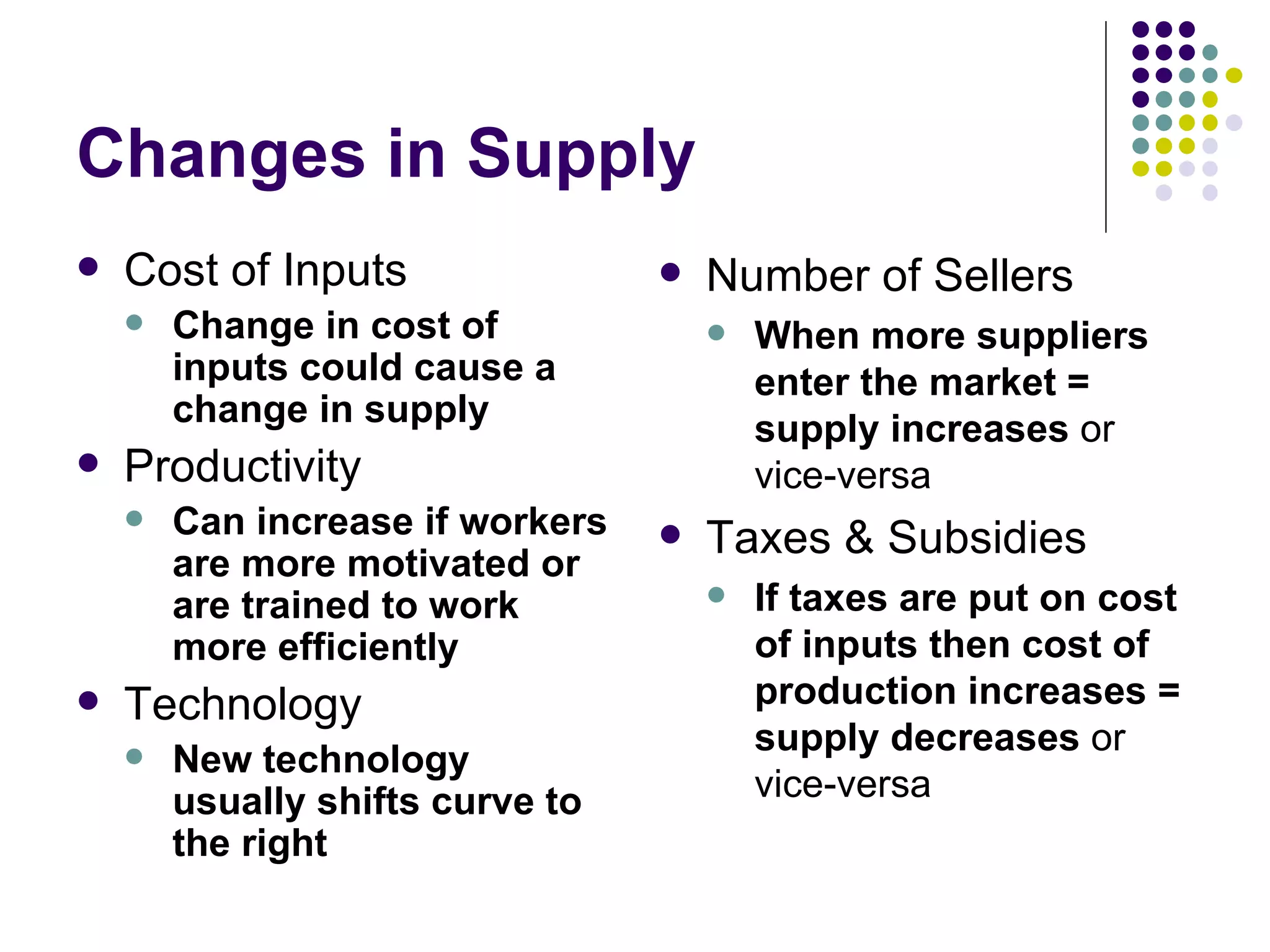

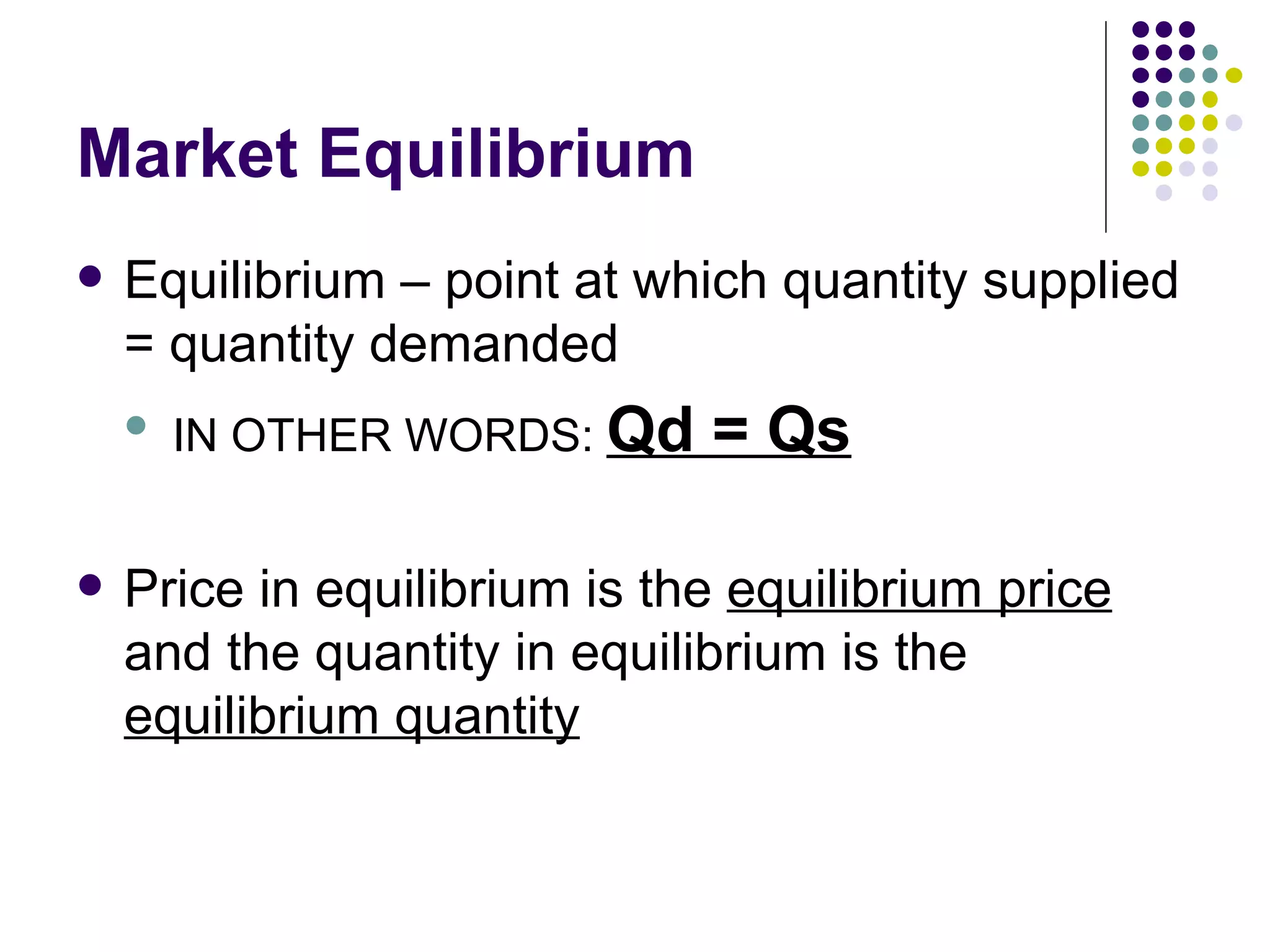

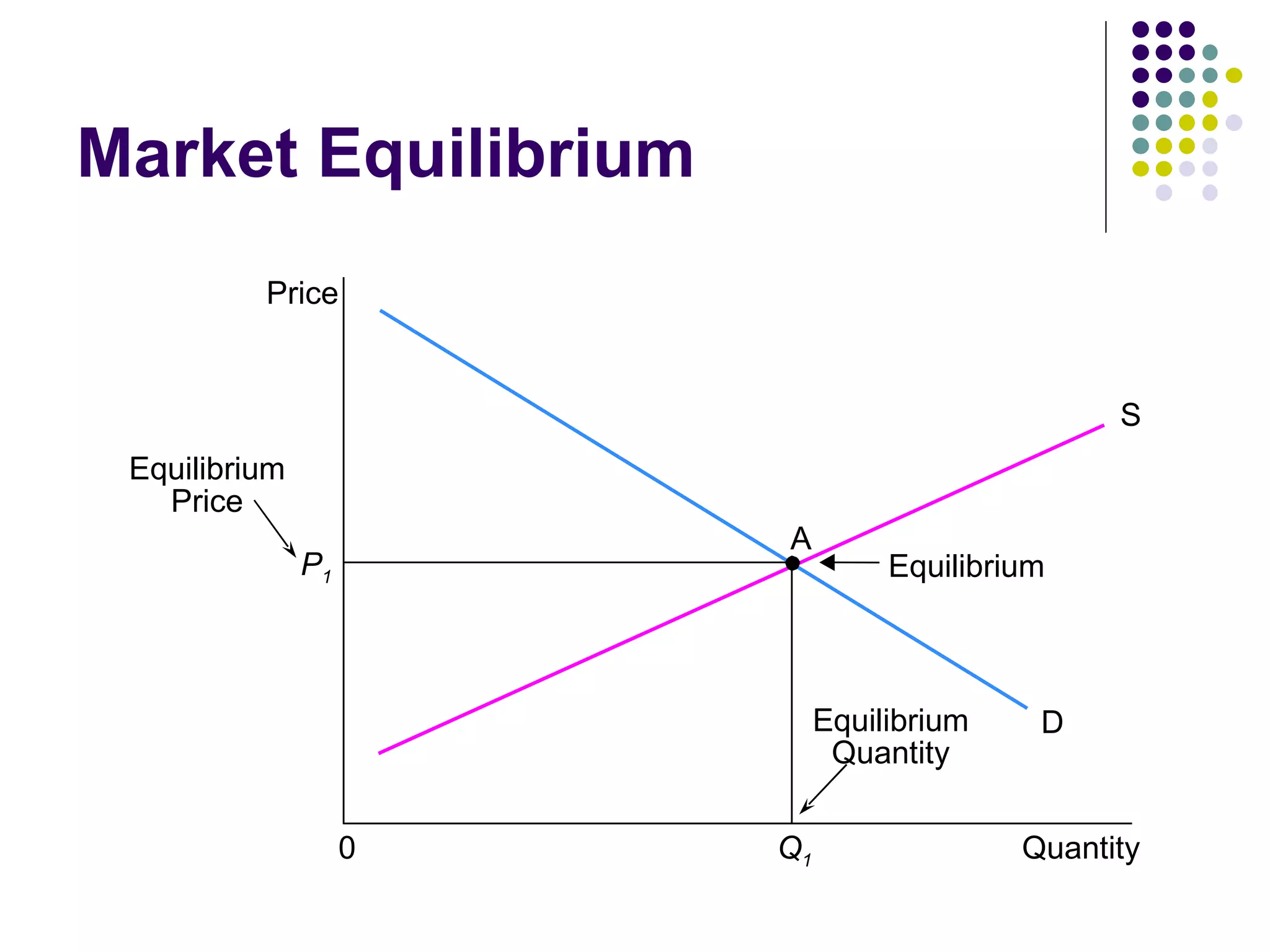

The document discusses the concepts of supply and demand in markets. It defines demand as the desire, ability, and willingness to buy a product, which is represented by a demand schedule and demand curve. The law of demand states that price and quantity demanded have an inverse relationship. Supply is defined as the quantity of a good producers will offer for sale at a given price, represented by a supply schedule and supply curve. The law of supply says price and quantity supplied have a direct relationship. Equilibrium occurs when quantity supplied equals quantity demanded at the market clearing price. [/SUMMARY]

![Lesson 7--supply[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-7-supply1-130409201835-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)