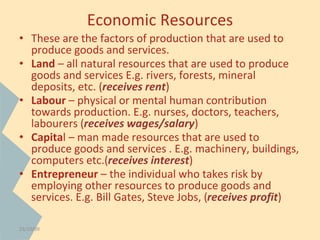

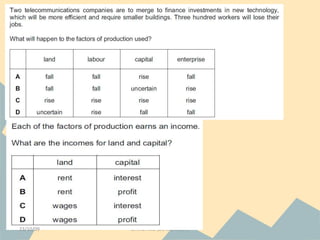

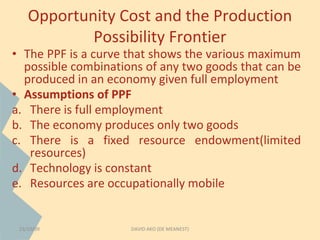

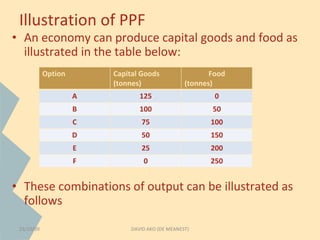

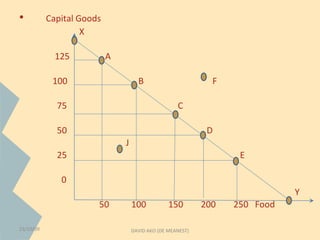

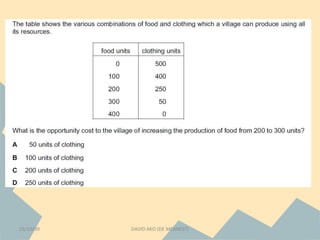

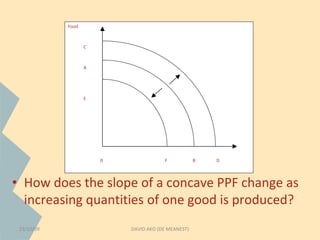

The document discusses the basic economic problem of scarcity and opportunity cost. It defines the key concepts of needs and wants, and explains that while needs are necessities, wants are pleasurable but not necessary goods. Resources used to produce goods and services are finite but human wants are unlimited, creating an economic problem. The concept of opportunity cost, which is the next best alternative forgone when making a choice due to scarce resources, is introduced and illustrated using a production possibilities frontier diagram showing the tradeoffs between producing two goods.