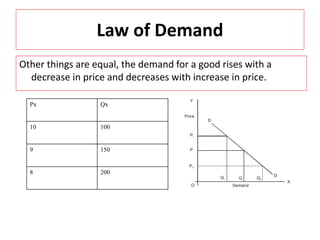

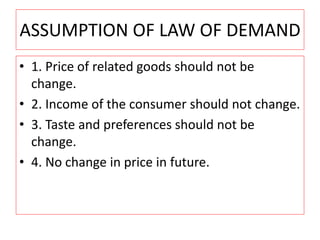

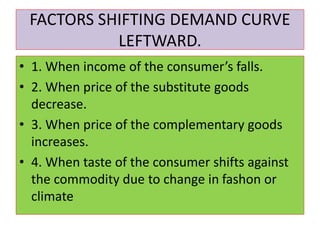

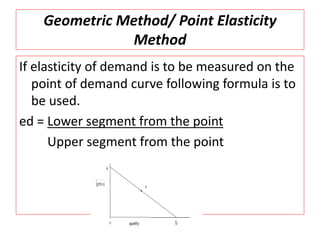

This document discusses demand, factors that affect demand, and the elasticity of demand. It defines demand as the quantity of a commodity a consumer is willing to buy at a given price and time. Demand is affected by the price of the commodity, prices of substitutes and complements, income, tastes, and expectations. The law of demand states that, all else equal, demand increases when price decreases and decreases when price increases. Elasticity of demand measures responsiveness of quantity demanded to price changes. It is measured using total expenditure, percentage, and point elasticity methods. Factors like availability of substitutes and nature of the good impact elasticity. Demand can be perfectly elastic, perfectly inelastic, or elastic.