Downloaded 40 times

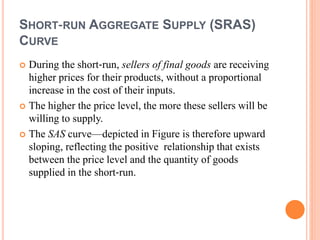

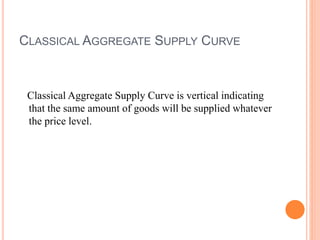

The document discusses aggregate supply curves, including short-run aggregate supply (SRAS) and long-run aggregate supply (LRAS) curves. The SRAS curve slopes upward as producers are willing to supply more output when prices are higher in the short-run before input prices adjust. The LRAS curve is vertical at the natural level of output, as prices and costs have fully adjusted in the long-run. The document also discusses factors that can cause shifts in the SRAS and LRAS curves such as changes in input prices, taxes, and economic growth.