This document discusses supply, including the law of supply, supply schedules and curves, determinants of supply, and supply elasticity. The key points are:

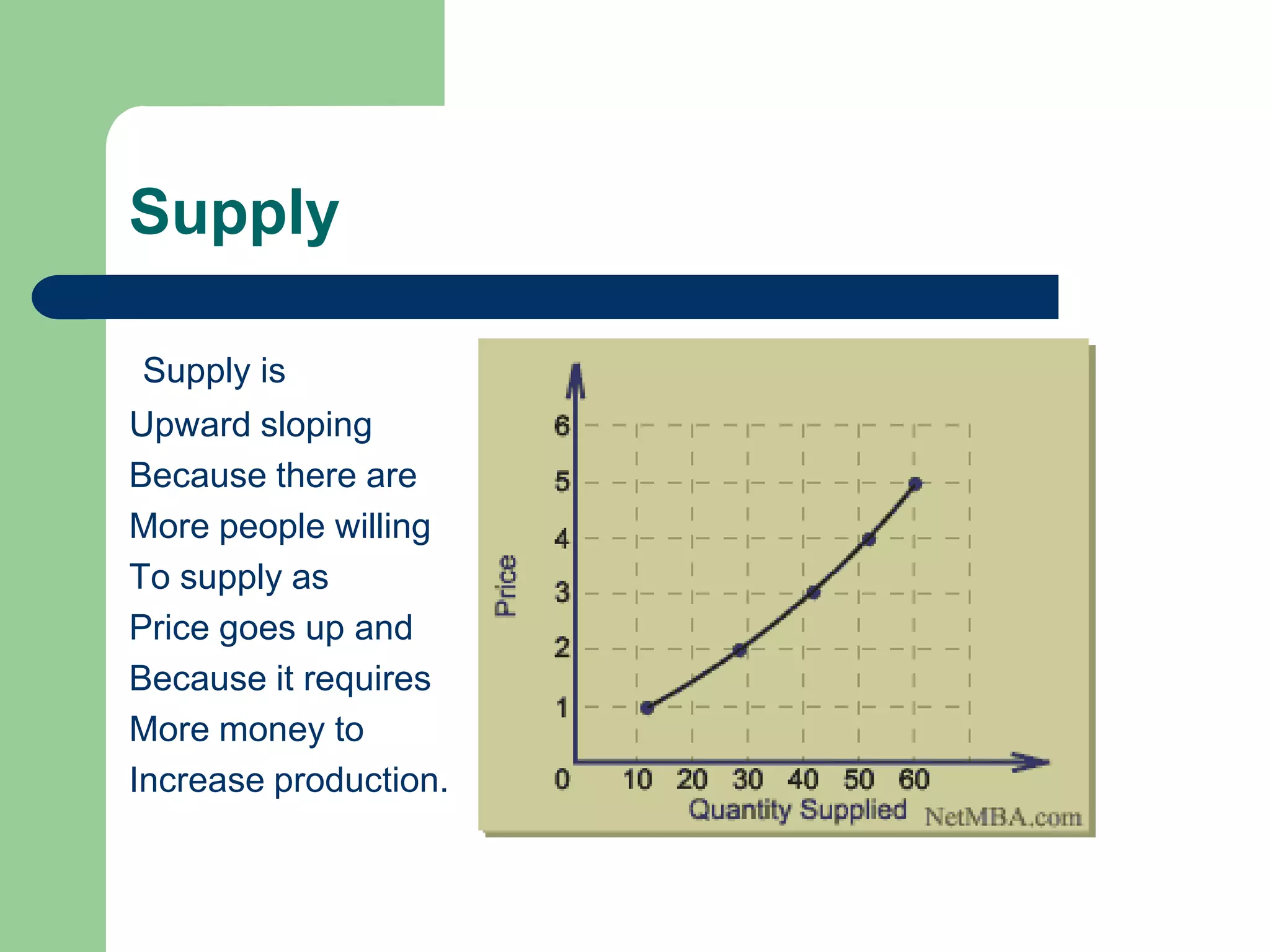

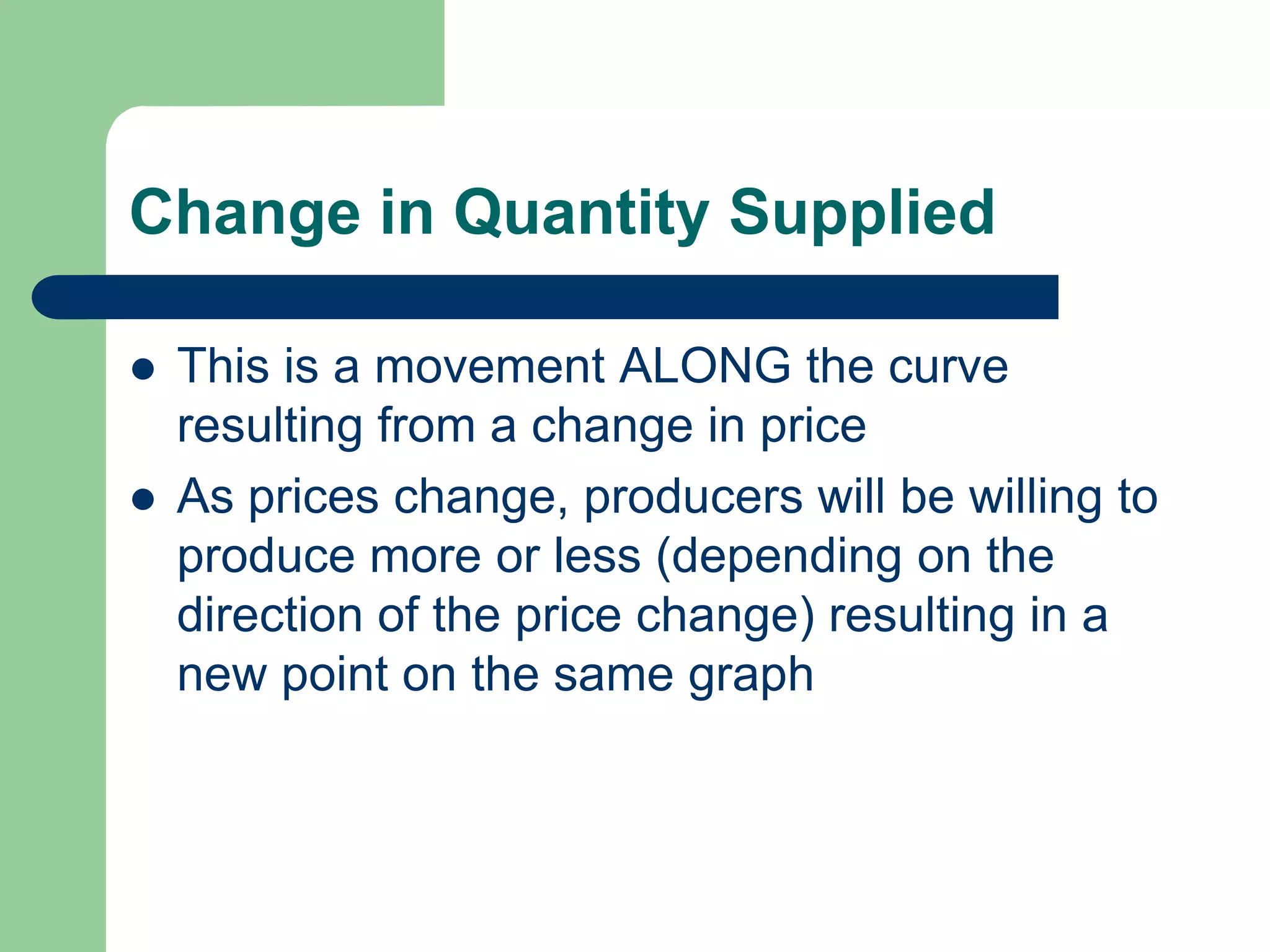

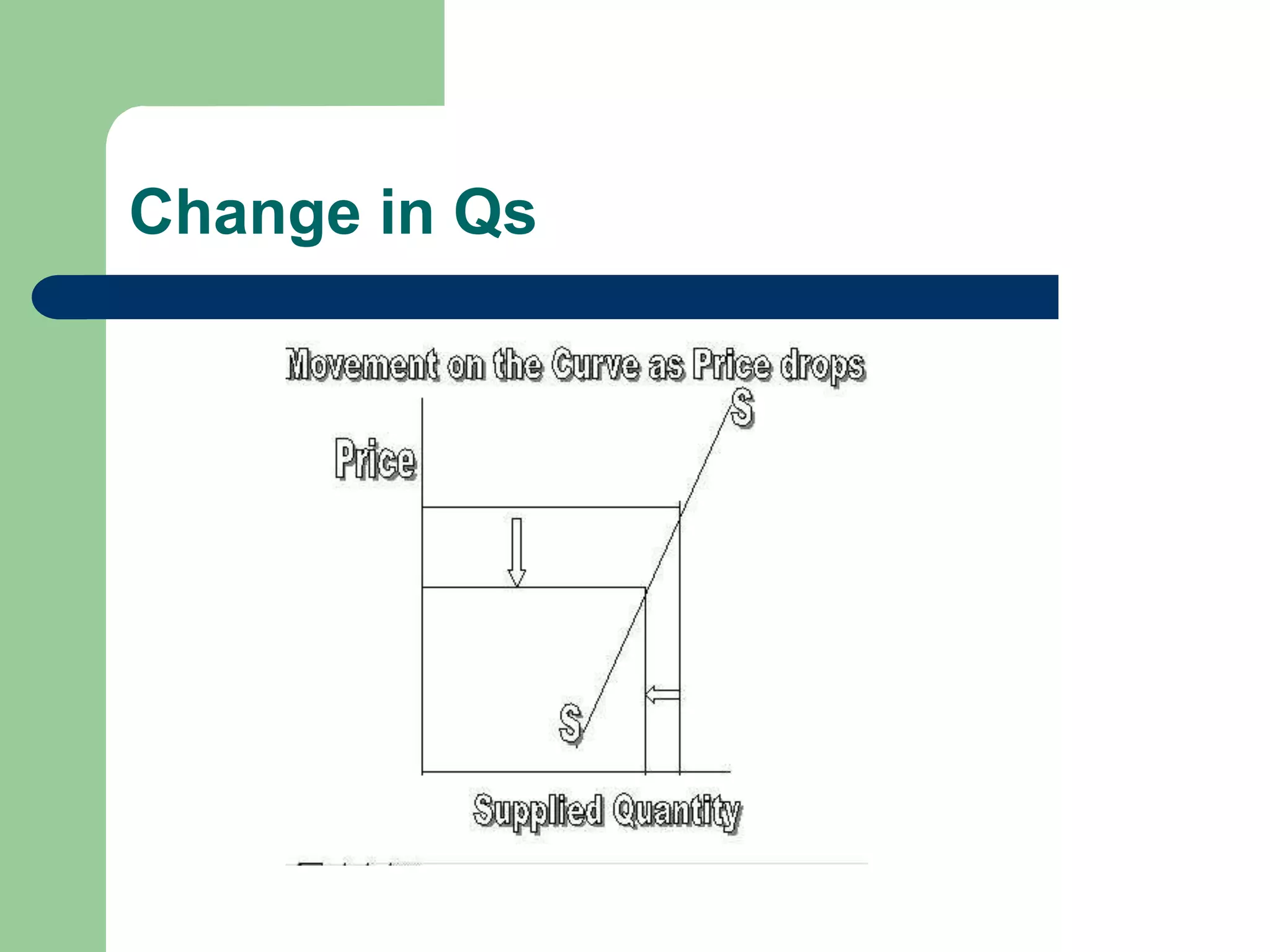

1) The law of supply states that the quantity supplied varies directly with price - producers will supply more of a product as the price increases.

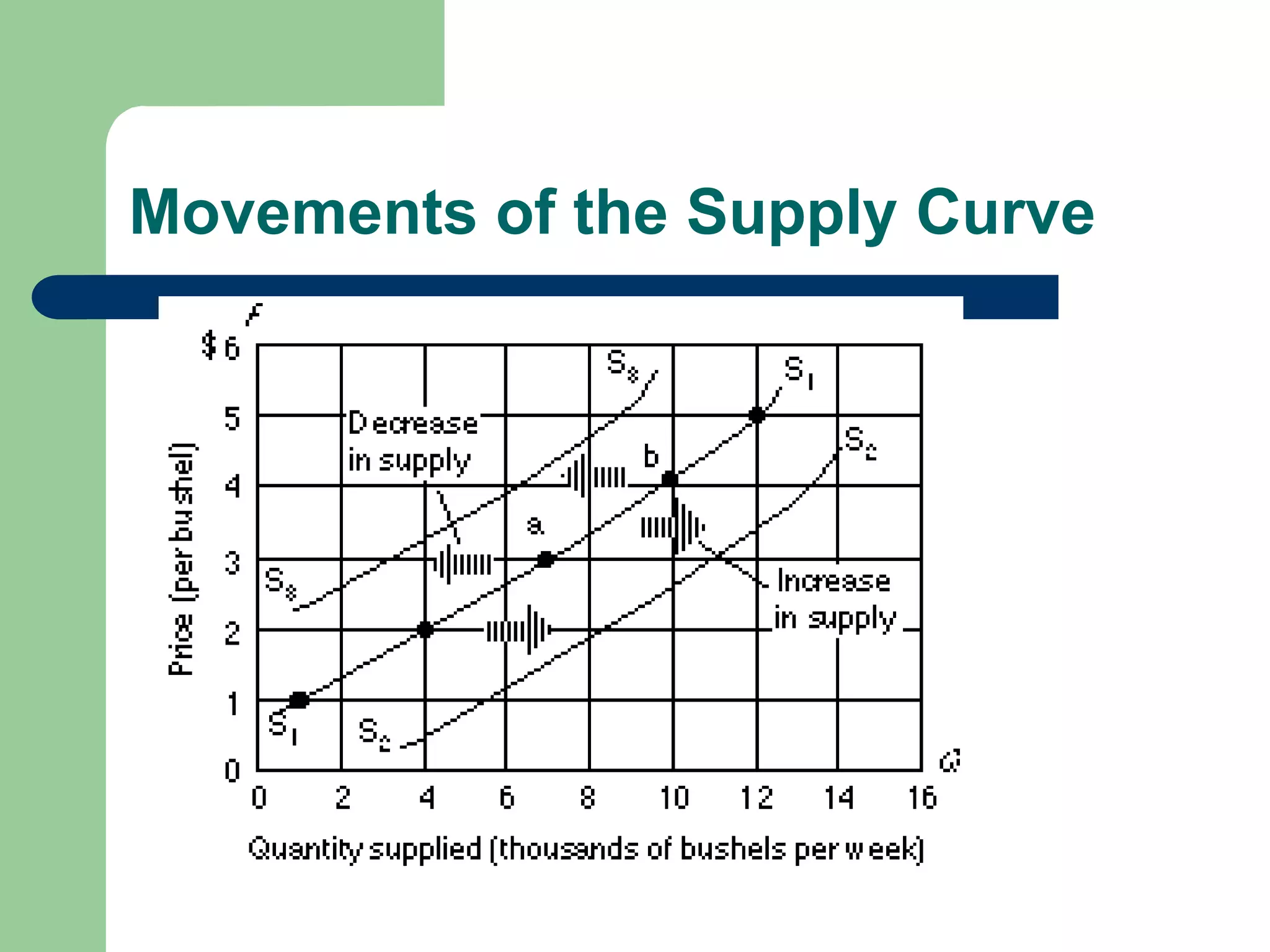

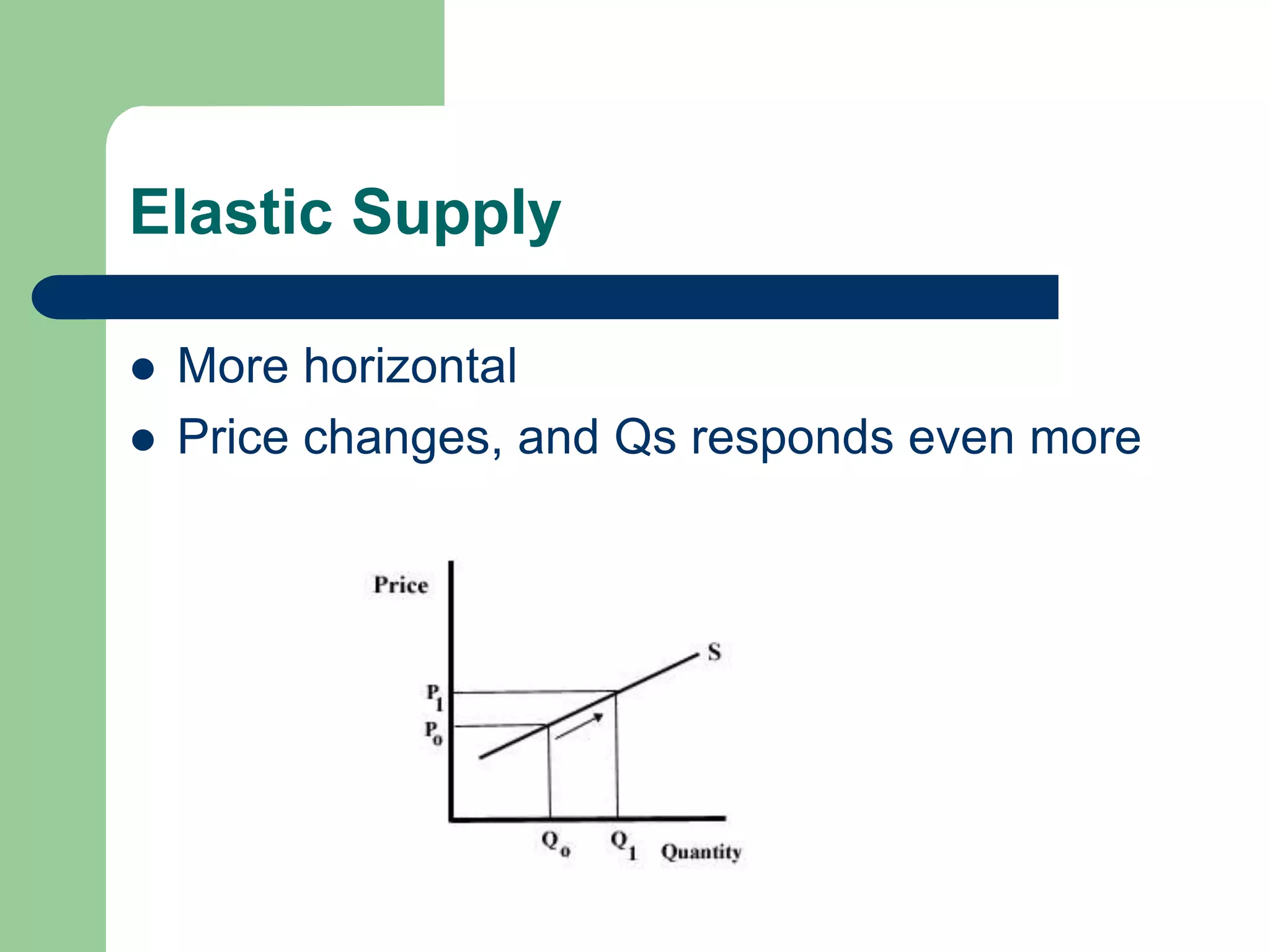

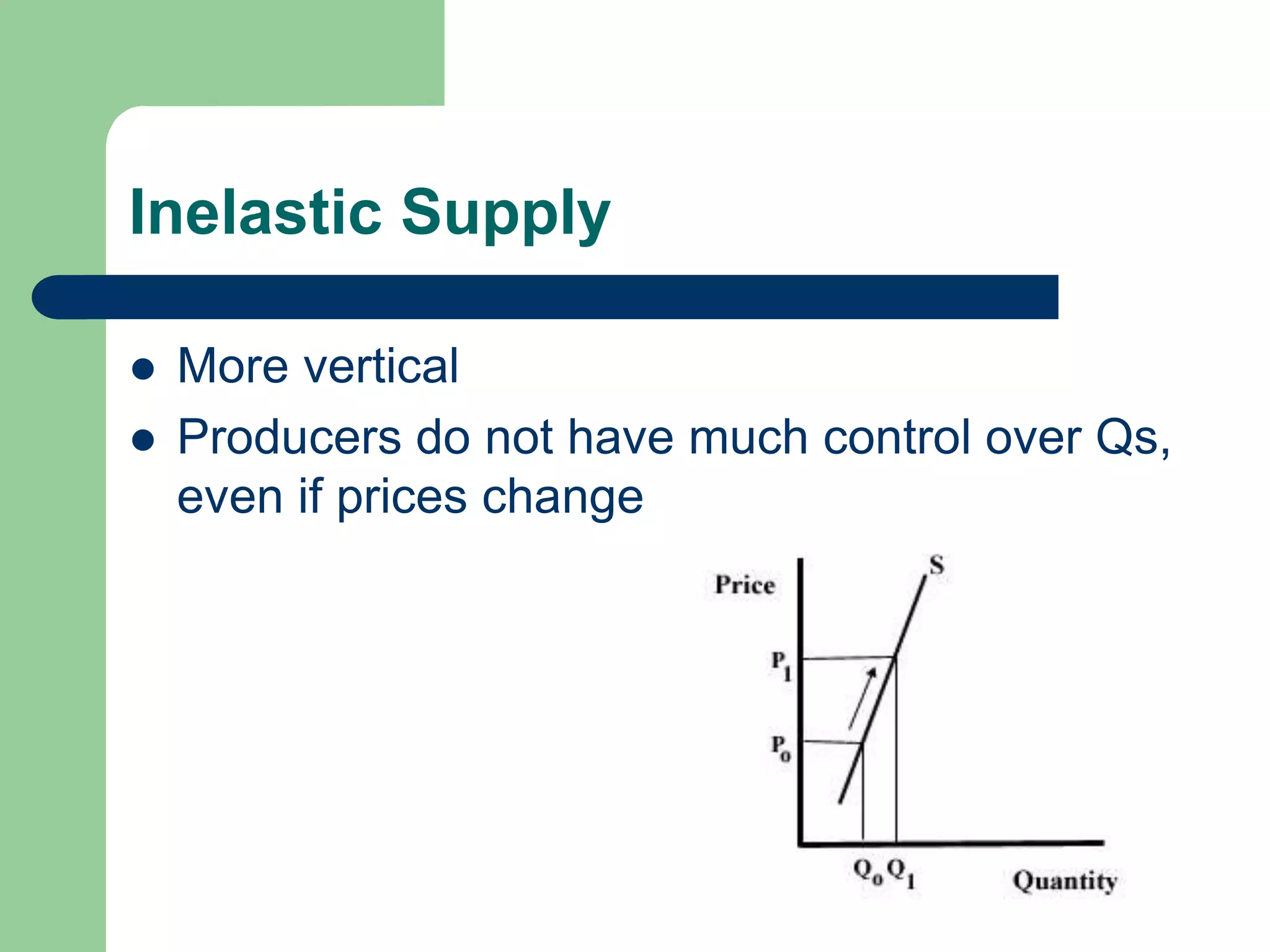

2) Supply curves show the different quantities producers will supply at different price points. They are generally upward sloping.

3) Determinants that can shift the supply curve include factor costs, technology, regulations, expectations, and the number of firms in the industry. Anything that impacts production costs or ability will shift the supply curve.

![Lesson 2--what-is-econ[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-2-what-is-econ1-130409195930-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![Lesson 6--demand[1]](https://cdn.slidesharecdn.com/ss_thumbnails/lesson-6-demand1-130409195933-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)