Downloaded 38 times

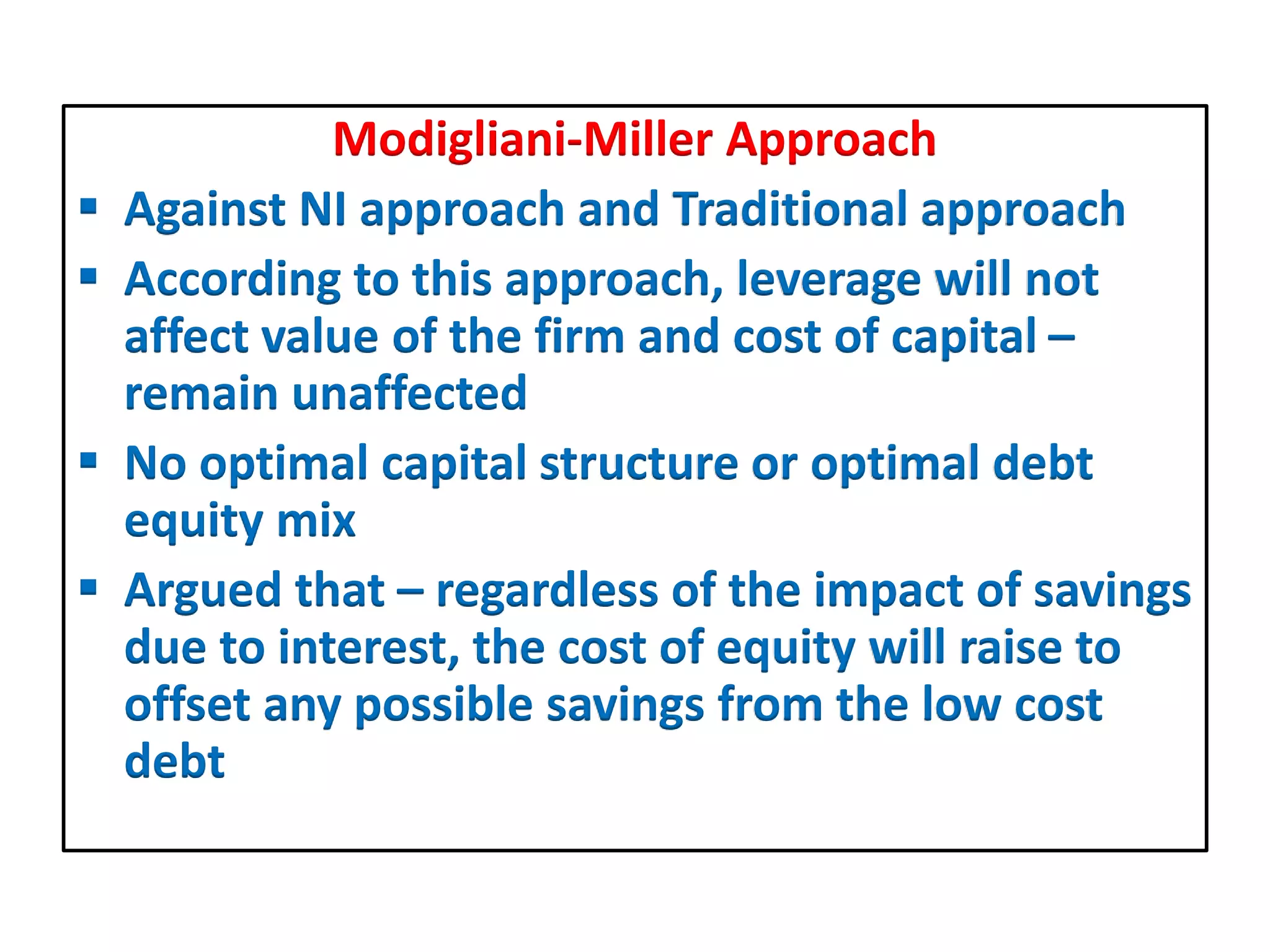

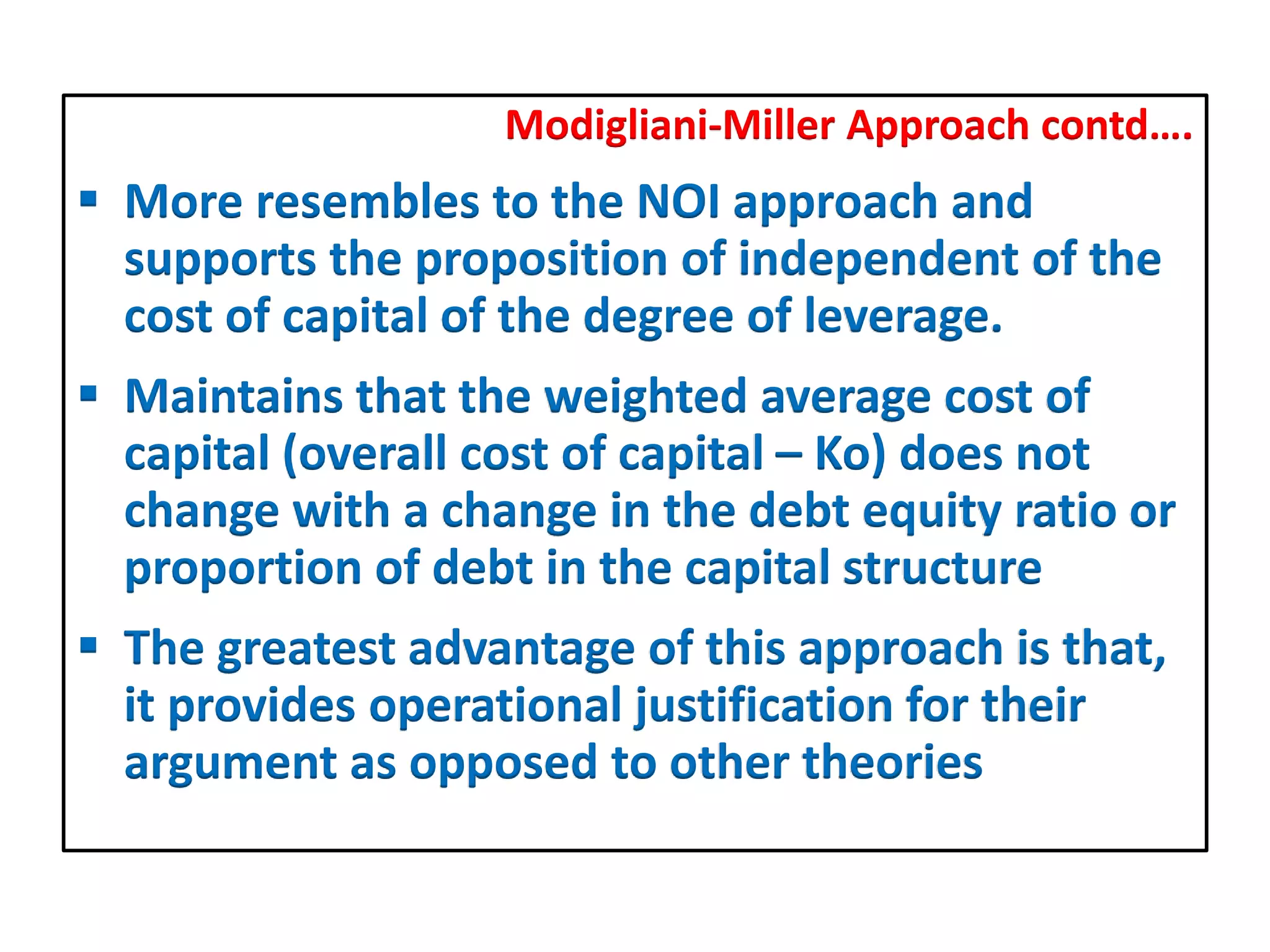

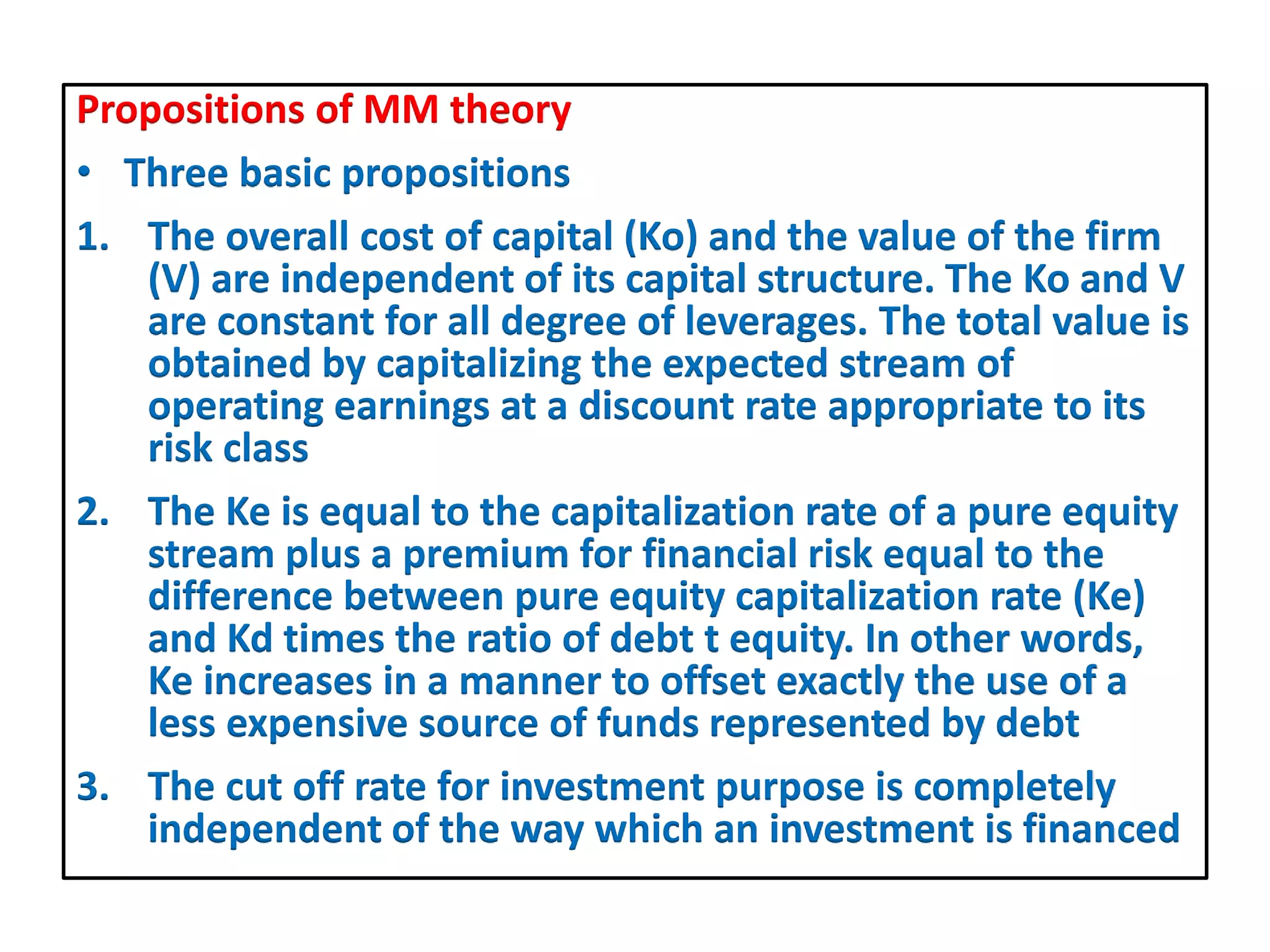

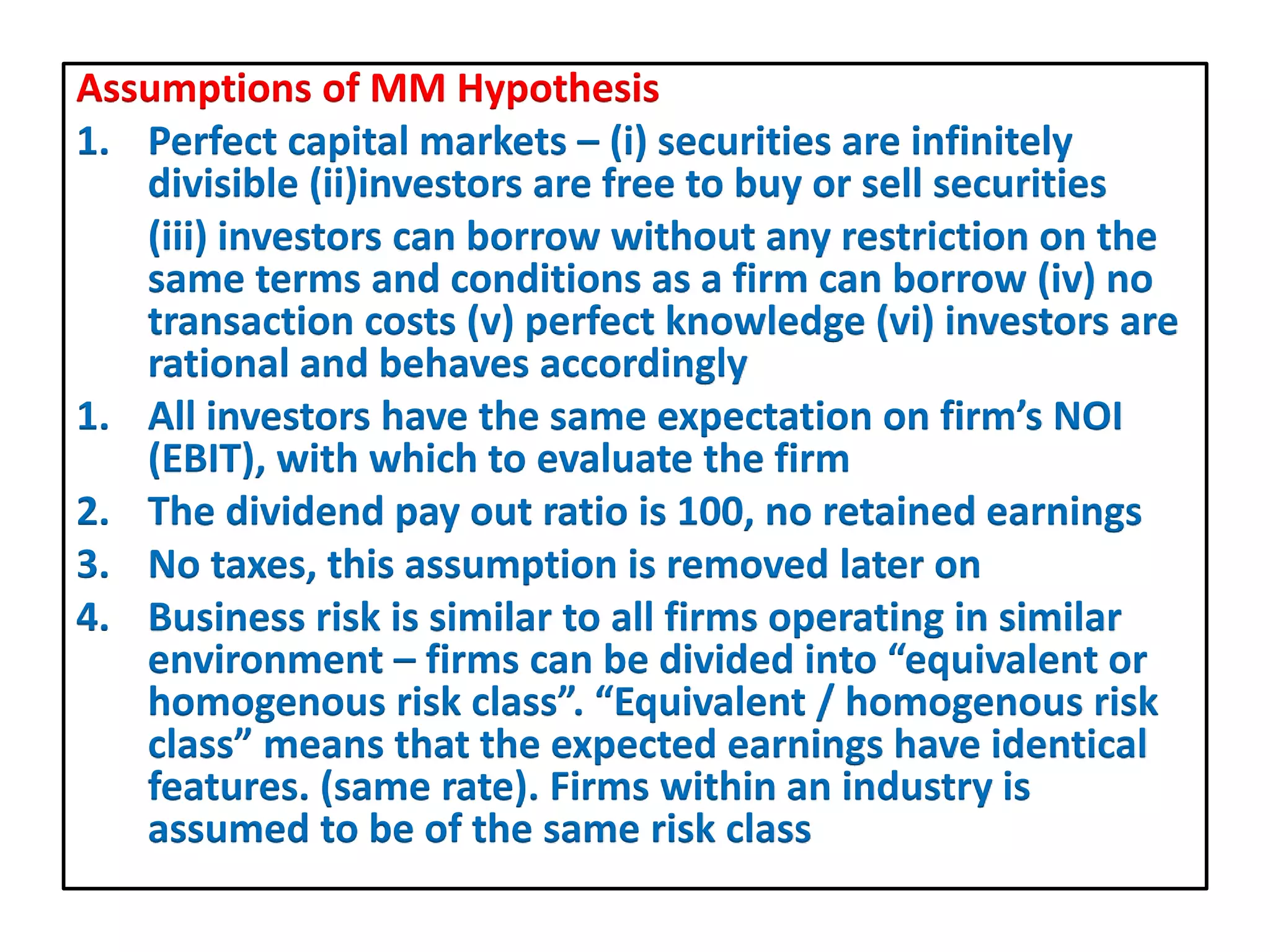

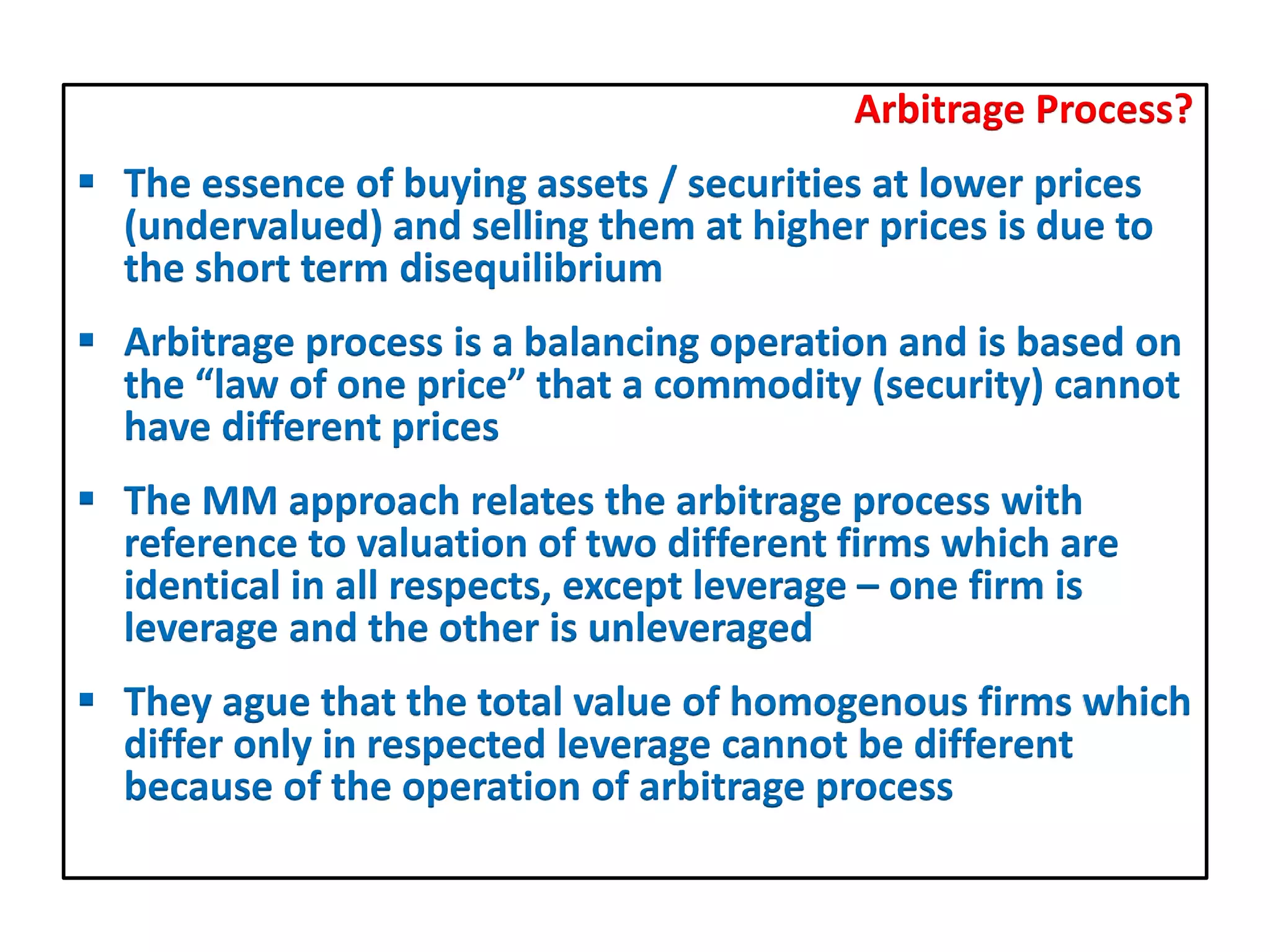

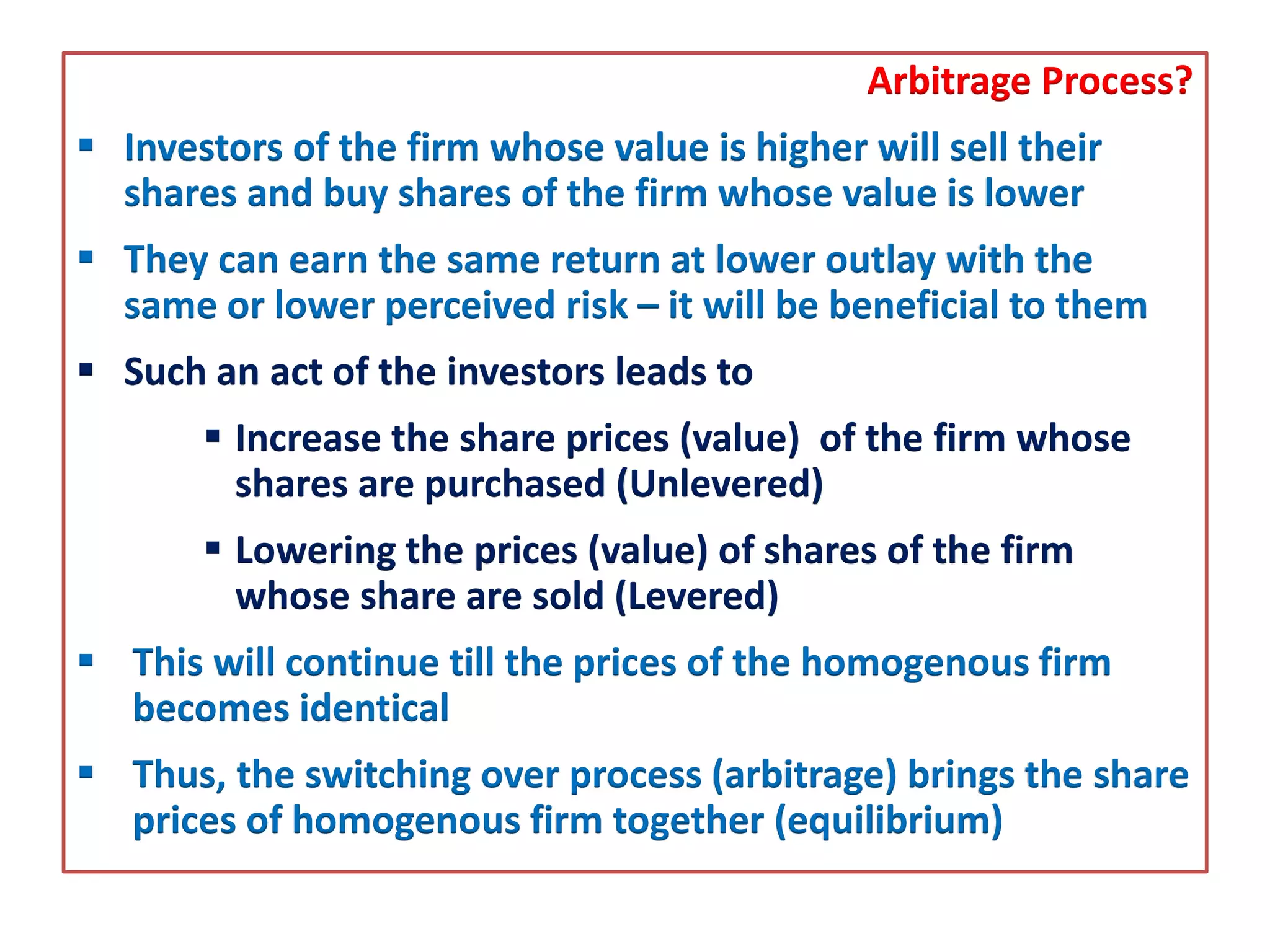

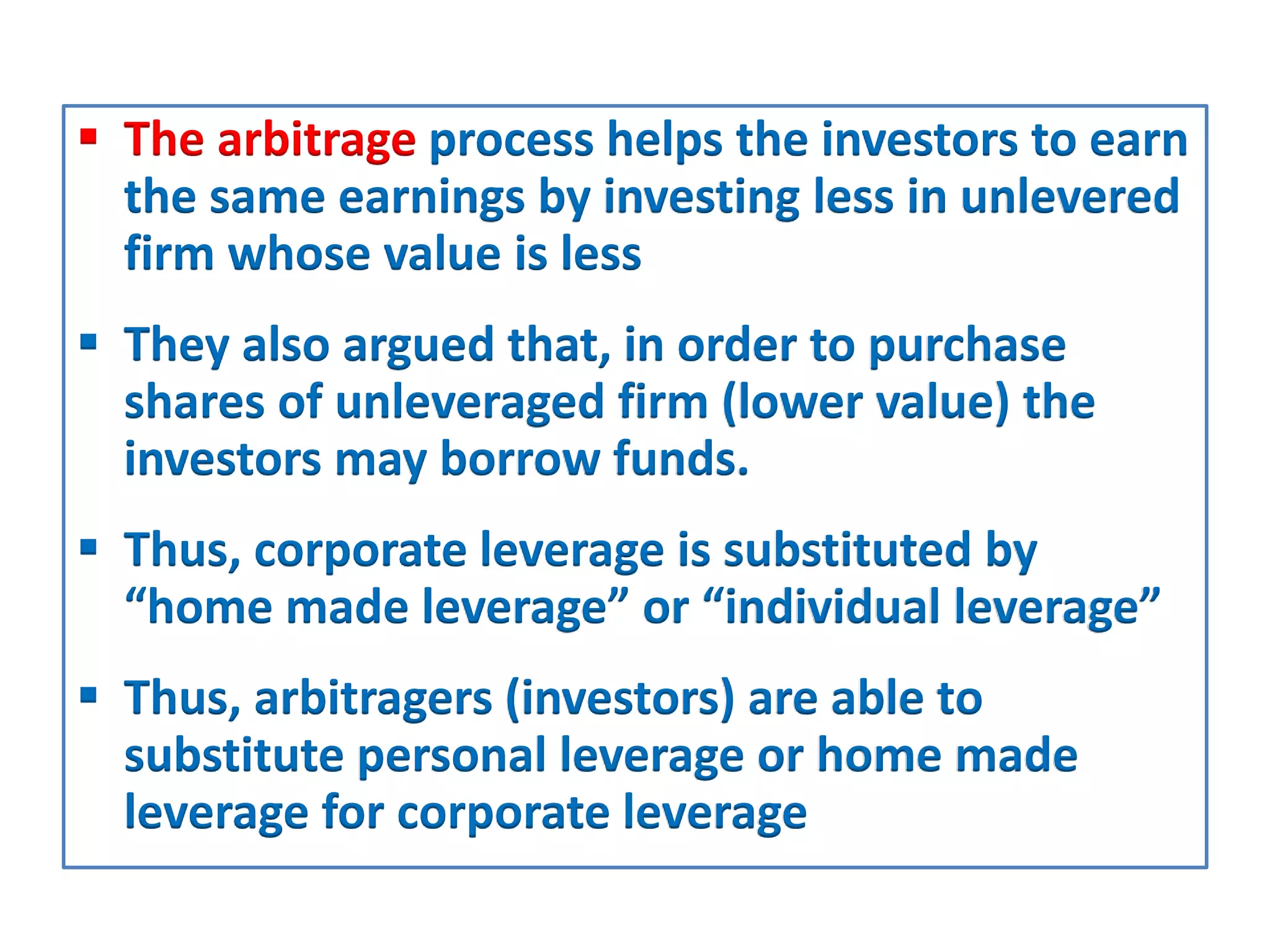

The document summarizes the Modigliani-Miller approach to capital structure. Some key points: 1) According to MM, leverage will not affect a firm's value or cost of capital. There is no optimal capital structure. 2) The cost of equity will rise to exactly offset any savings from low-cost debt, keeping the weighted average cost of capital constant regardless of capital structure. 3) MM relies on the concept of arbitrage to argue that investors can substitute "homemade leverage" to achieve the same returns, keeping firm values and costs constant across different structures. 4) MM later incorporated taxes, recognizing debt provides a tax shield that lowers the weighted average cost of capital