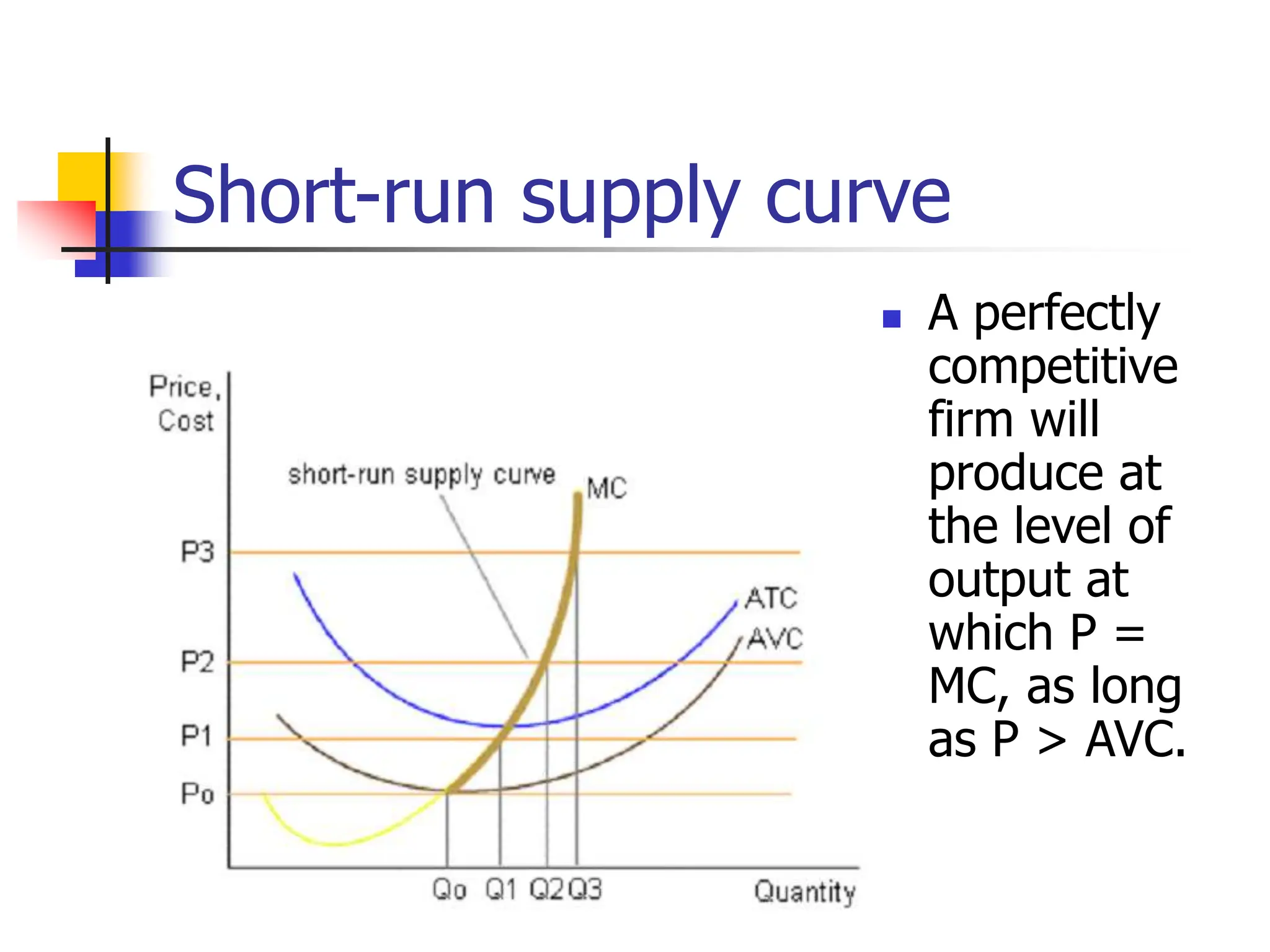

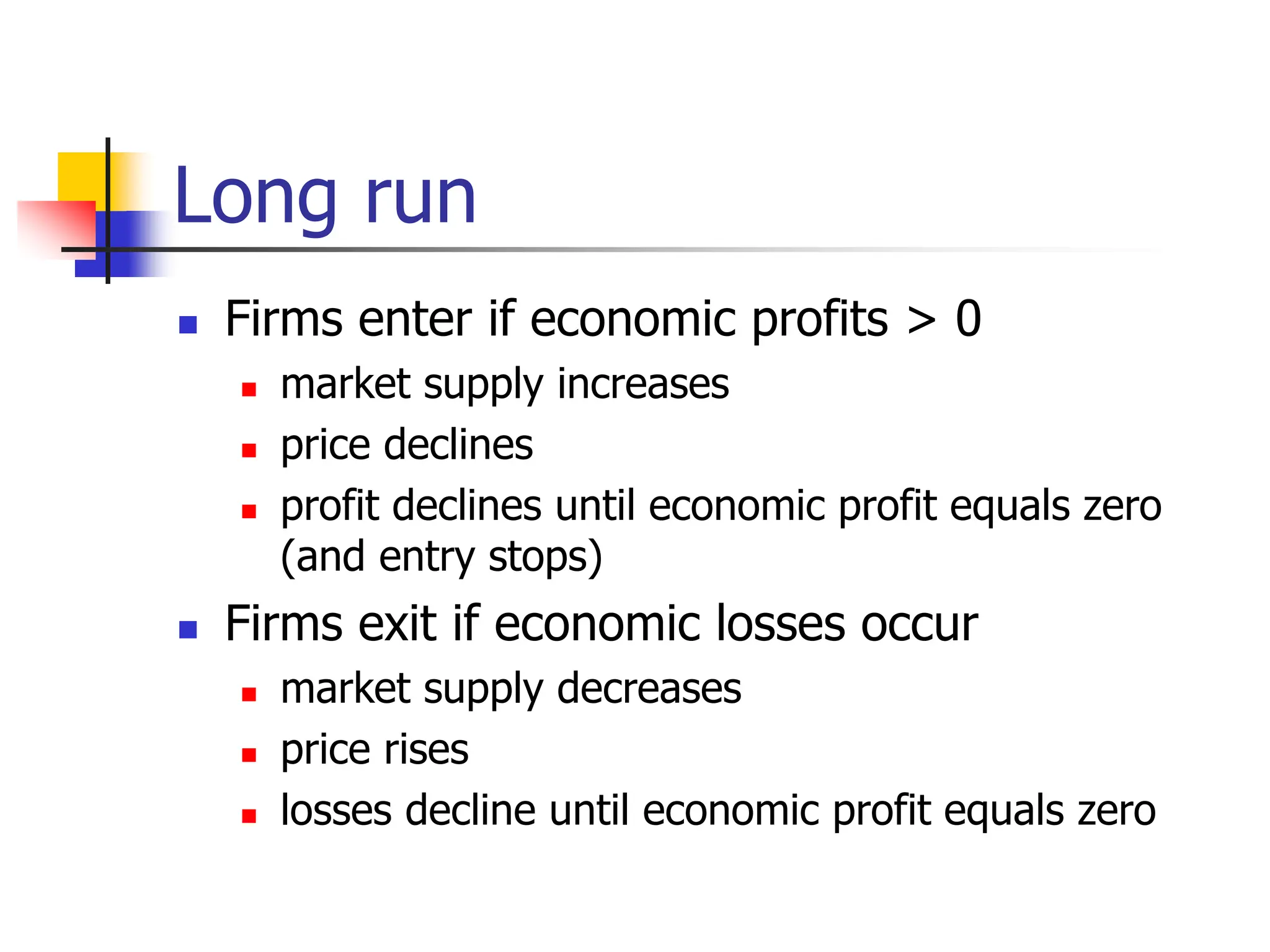

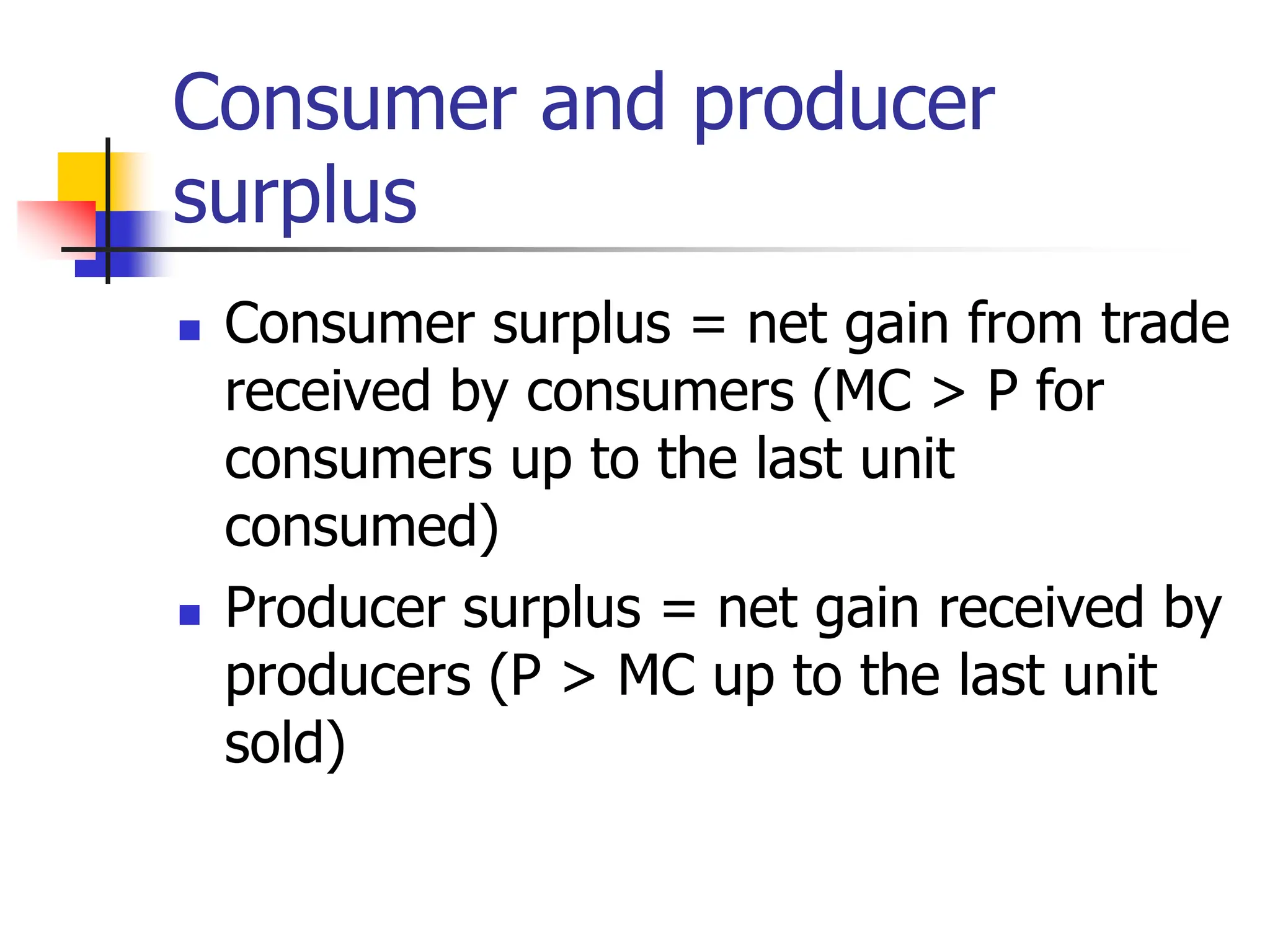

Chapter 8 discusses the characteristics of a perfectly competitive market, including many buyers and sellers, homogeneous products, and no barriers to entry or exit. It explains profit maximization strategies for firms, including conditions under which firms should shut down or continue operating based on average variable cost and average total cost. Lastly, the chapter covers long-run equilibrium and economic efficiency, emphasizing the relationship between price, marginal cost, and average total cost, as well as consumer and producer surplus.