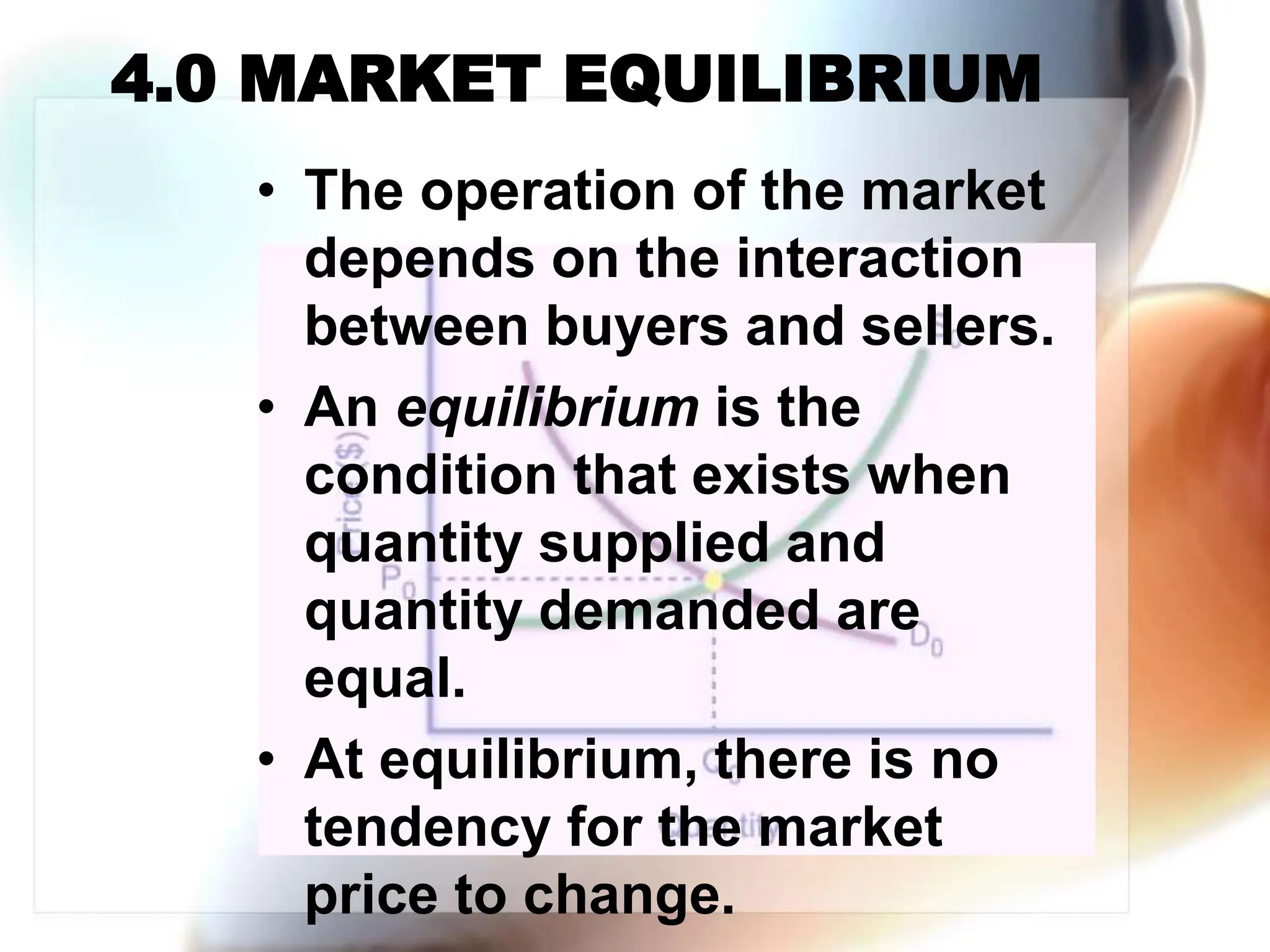

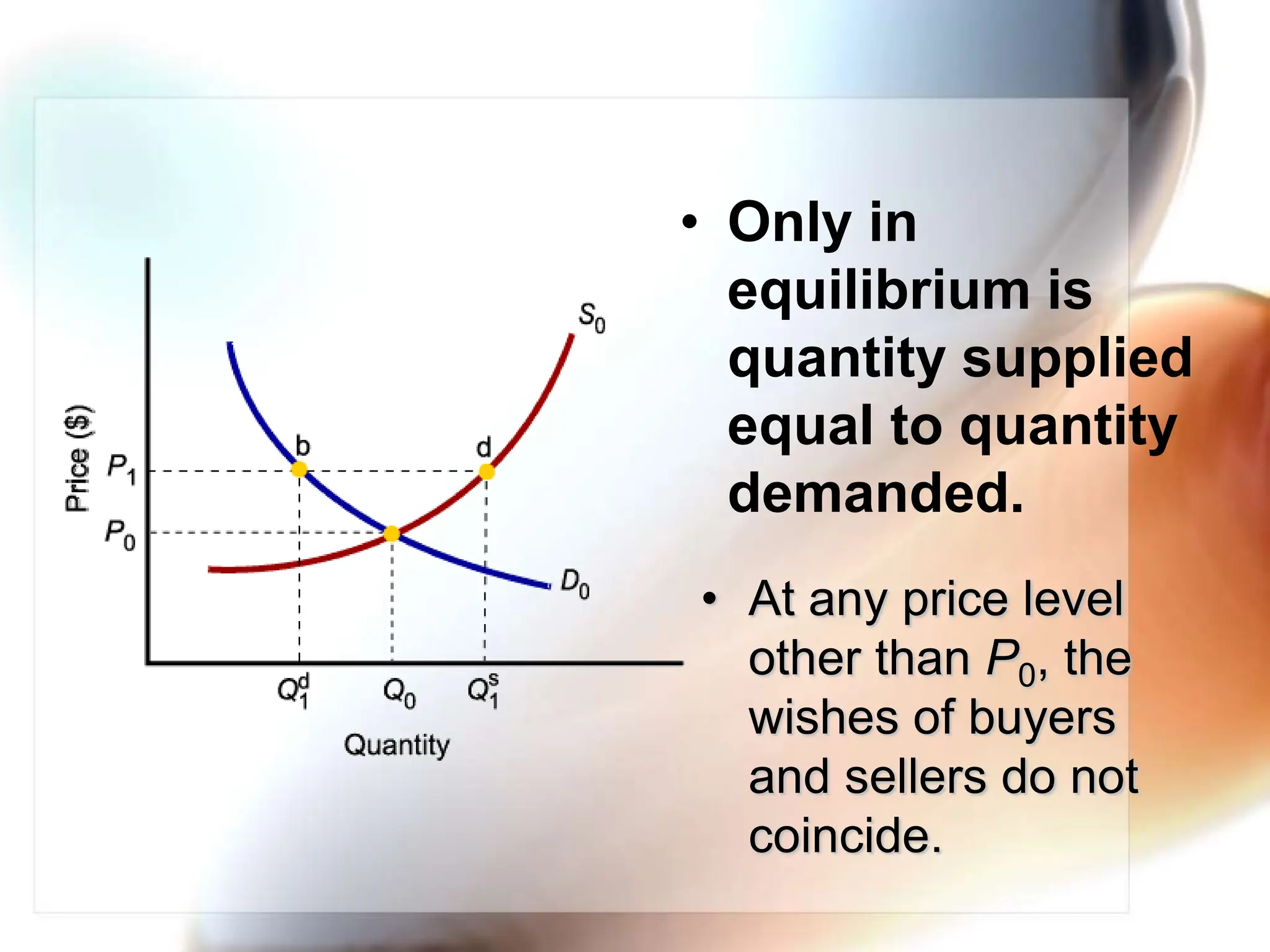

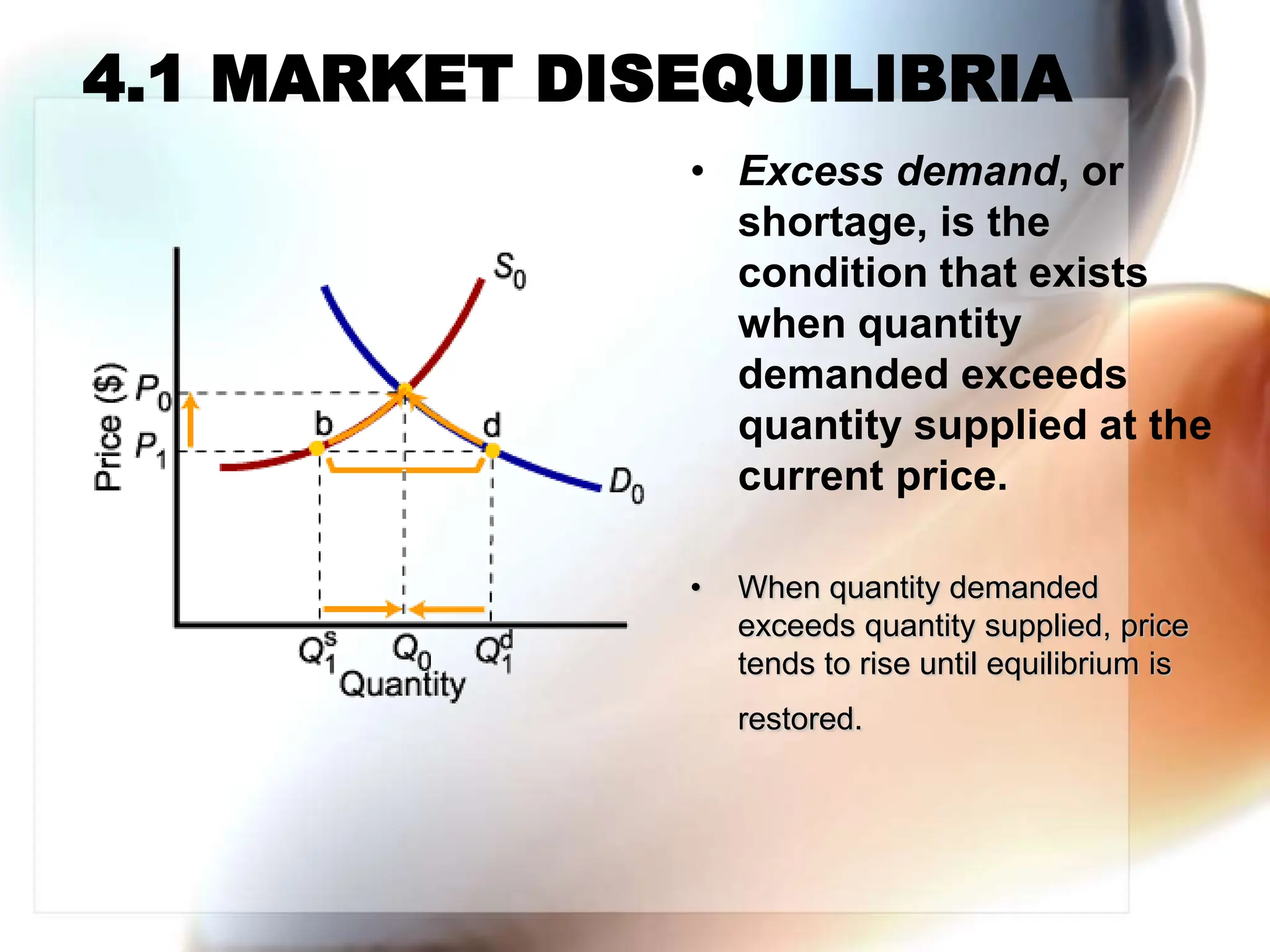

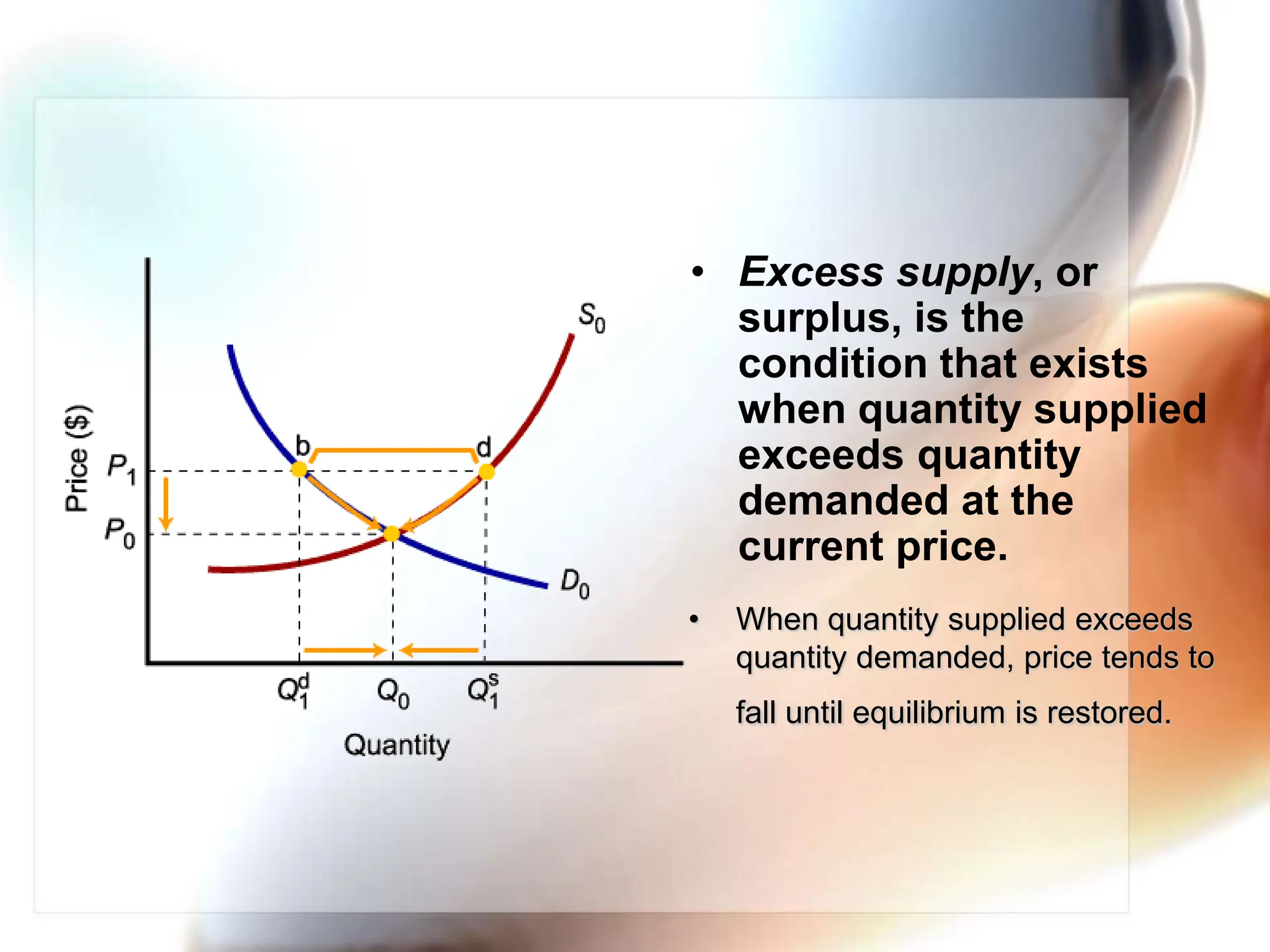

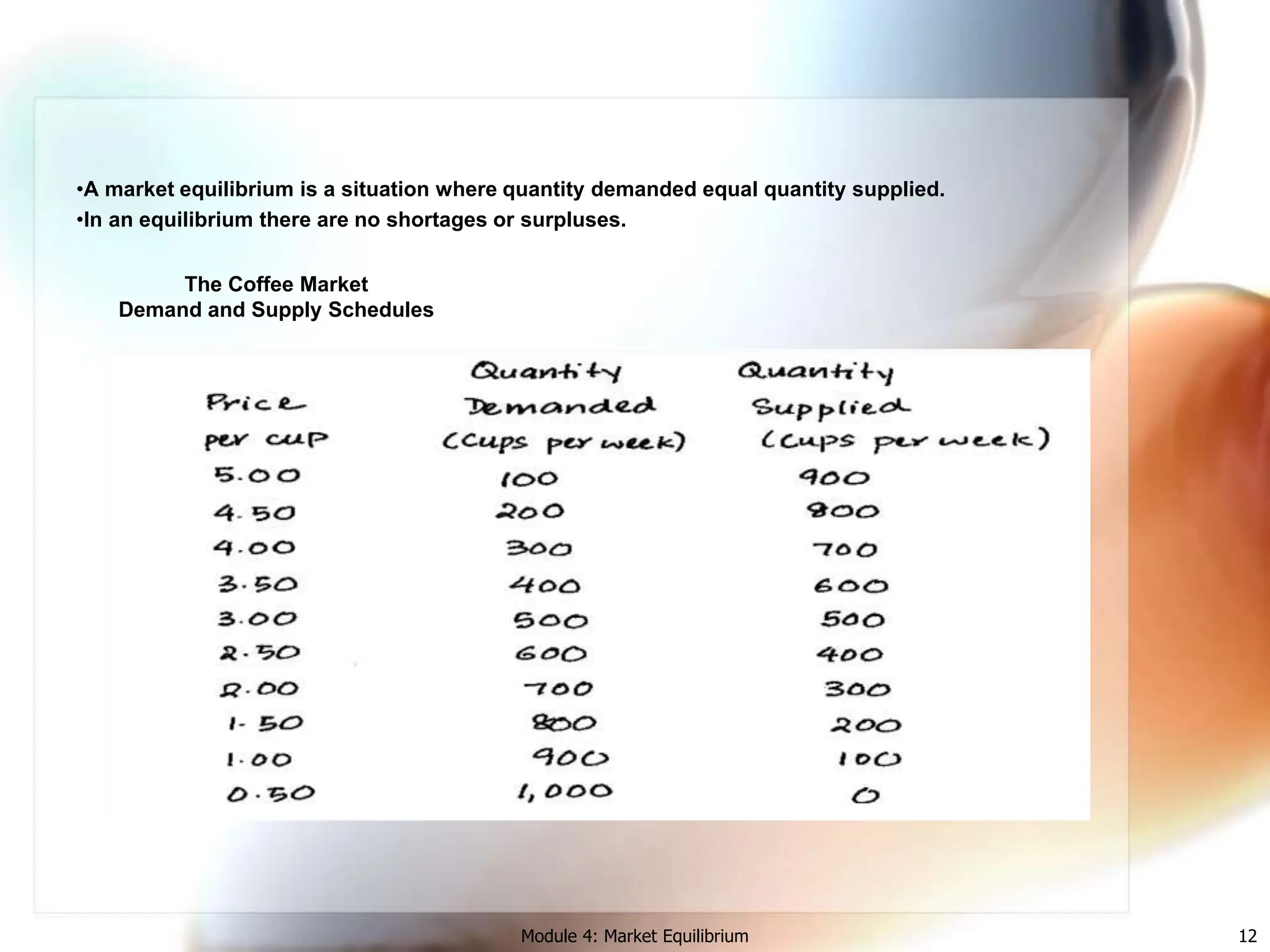

Chapter 4 of microeconomics focuses on market equilibrium, describing it as the state where quantity supplied equals quantity demanded, leading to no price changes. It explains excess demand and supply conditions, their effects on prices, and how shifts in demand and supply impact equilibrium. Additionally, the chapter discusses government interventions through price ceilings and floors, highlighting their potential to create shortages and surpluses.