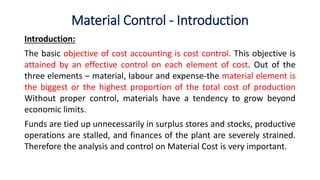

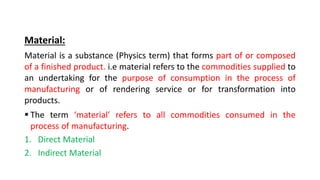

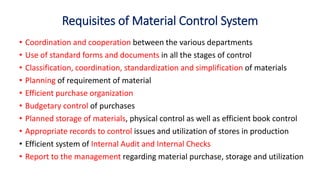

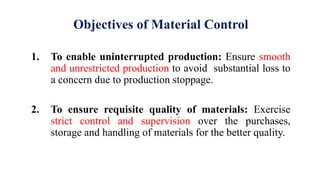

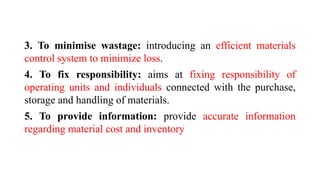

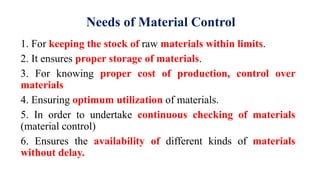

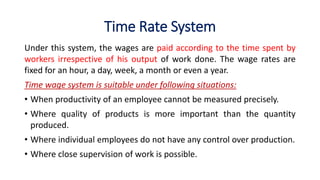

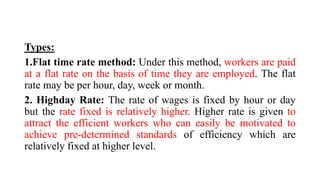

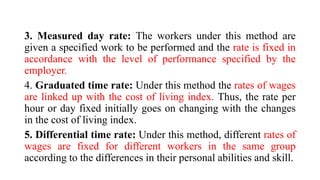

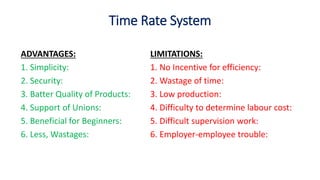

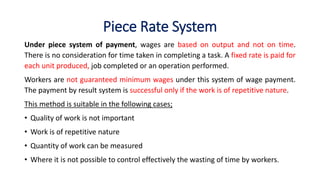

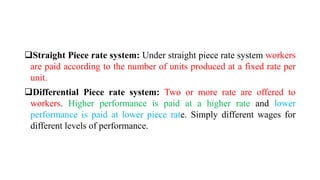

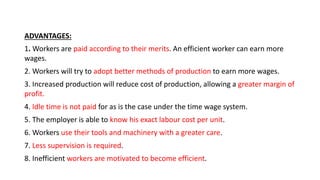

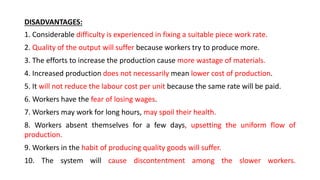

This document provides an overview of material and labour cost control. It discusses material control techniques like ABC analysis, VED analysis, inventory levels, and economic order quantity. It describes the steps in material control like purchase requisition, selection of suppliers, and receipt of materials. Pricing methods for material issues like FIFO, LIFO, and average cost are explained. The document also covers labour cost elements like direct and indirect labour. It defines idle time and overtime, and discusses causes of idle time like administrative, productive and economic causes. Time rate and piece rate systems for labour remuneration are introduced.