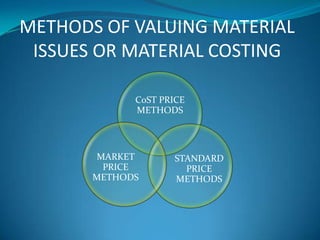

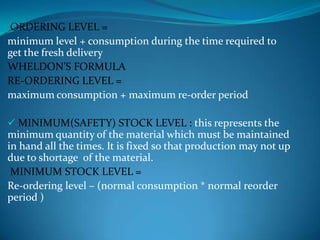

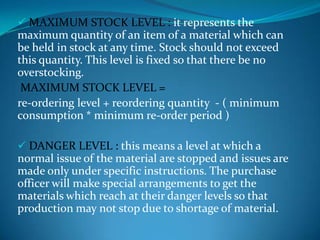

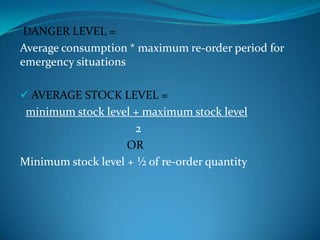

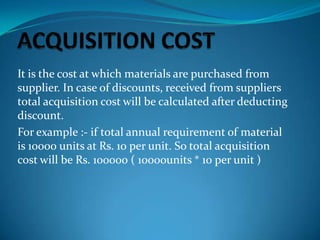

The document discusses material control and management. It defines direct and indirect materials. Direct materials form part of the finished product, while indirect materials cannot be allocated to a specific product. The summary maintains proper control over purchasing, storing, and using materials to minimize costs while ensuring production is not interrupted due to lack of materials. It also covers accounting and operational aspects of material control.

![Getting Started with Apache Spark: Big Data Made Simple [Free Meetup]](https://cdn.slidesharecdn.com/ss_thumbnails/apachesparkgettingstarted-260203175547-8361bcc3-thumbnail.jpg?width=640&height=640&fit=bounds)