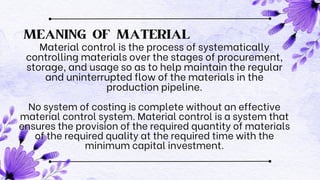

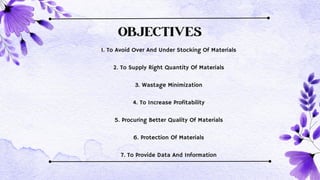

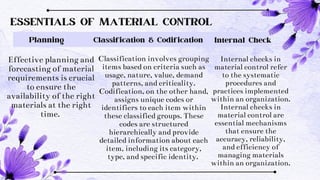

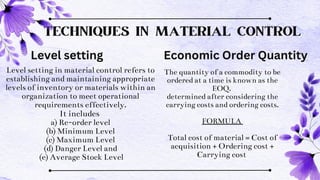

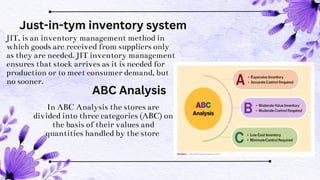

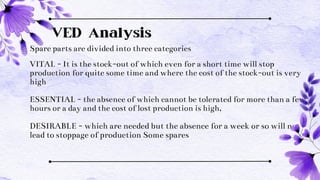

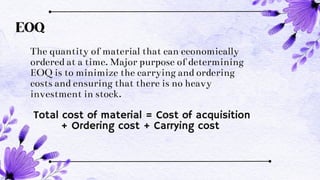

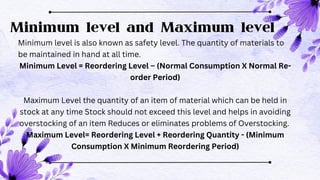

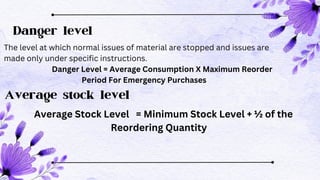

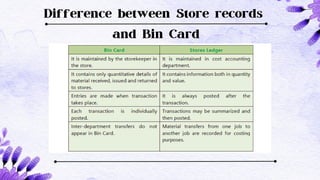

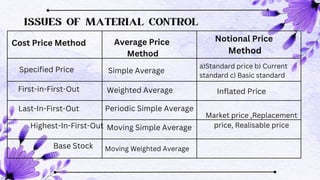

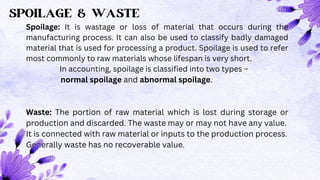

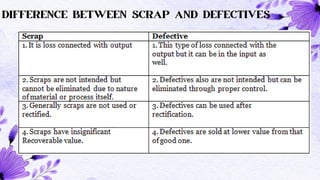

Material control is a systematic process ensuring the right quantity and quality of materials at the right time while minimizing costs and wastage. Key objectives include preventing overstocking, increasing profitability, and maintaining quality, with essential techniques like Economic Order Quantity (EOQ) and Just-In-Time (JIT) principles used to manage inventory effectively. The document also discusses categories of inventory, loss causes, and pricing methods, emphasizing the significance of effective material management in production.