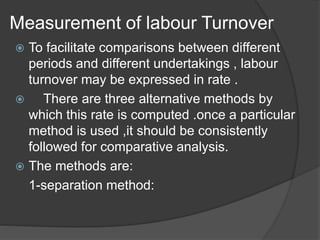

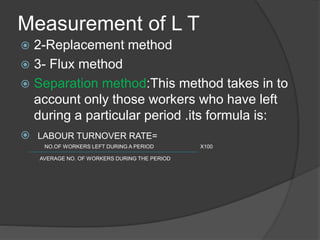

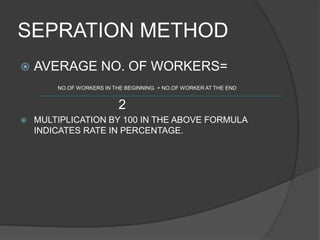

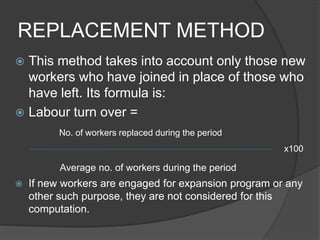

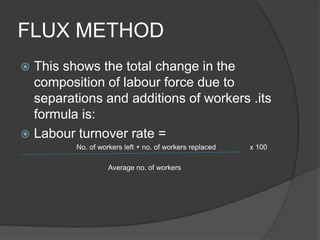

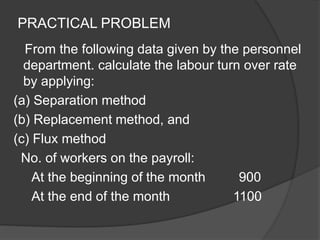

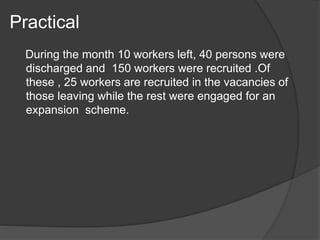

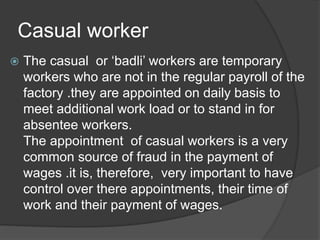

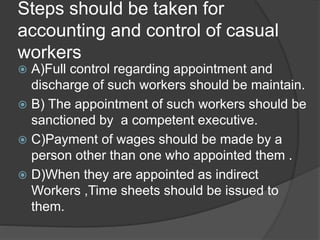

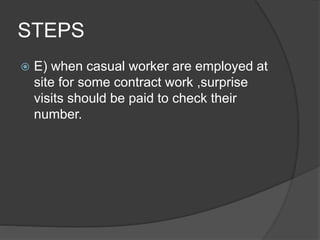

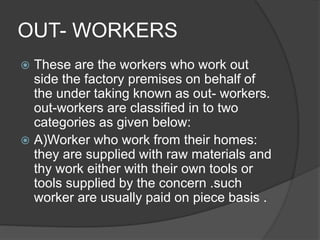

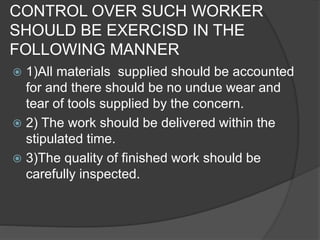

This document discusses various aspects of labour cost, including direct labour, indirect labour, labour turnover, and idle time. Direct labour refers to workers who directly produce goods, while indirect labour provides supporting functions. Labour turnover measures the rate at which workers leave and are replaced. Idle time represents time workers are paid for but do not spend on production, which can be normal or abnormal depending on its controllability. The document also covers topics like casual workers, out-workers, and overtime pay.