Download to read offline

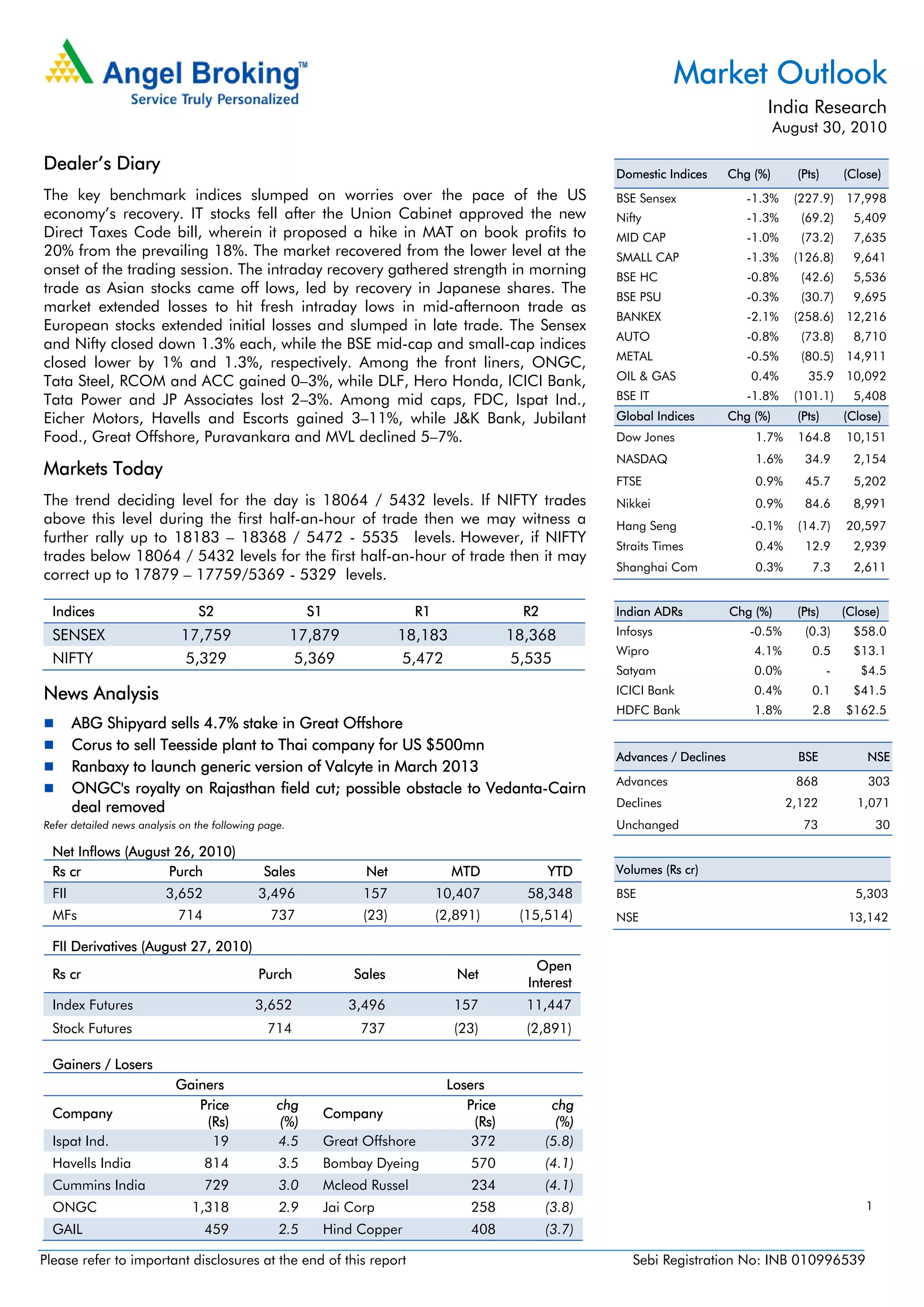

The key Indian stock market indices slumped over 1% due to worries about the pace of the US economic recovery and a proposed hike in taxes on book profits in India. IT stocks fell sharply. Metals and oil & gas stocks showed some gains. Several mid- and small-cap stocks rose or fell over 3-11%. News items discussed corporate deals, a royalty dispute resolution, and upcoming company results.