Downloaded 591 times

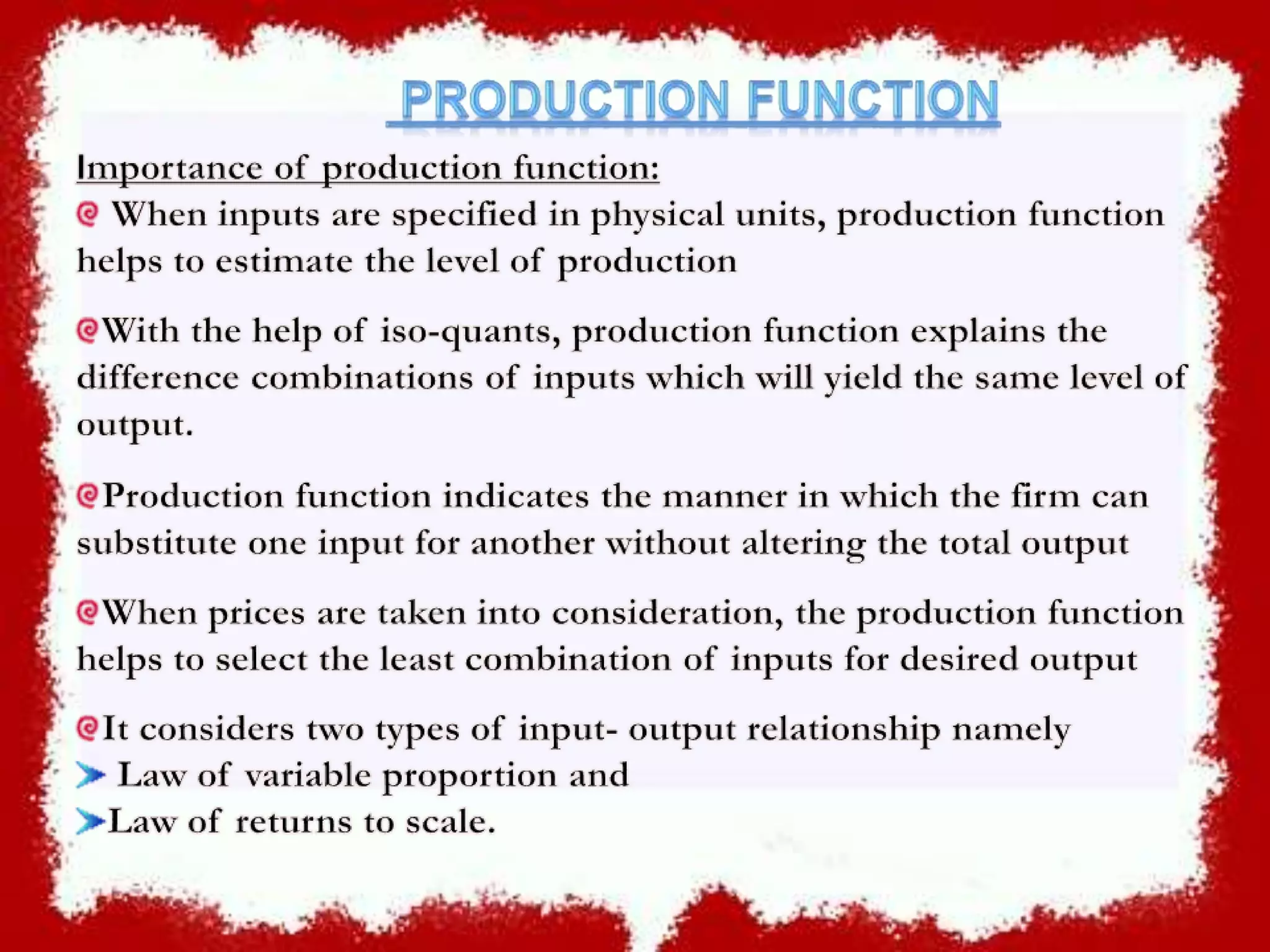

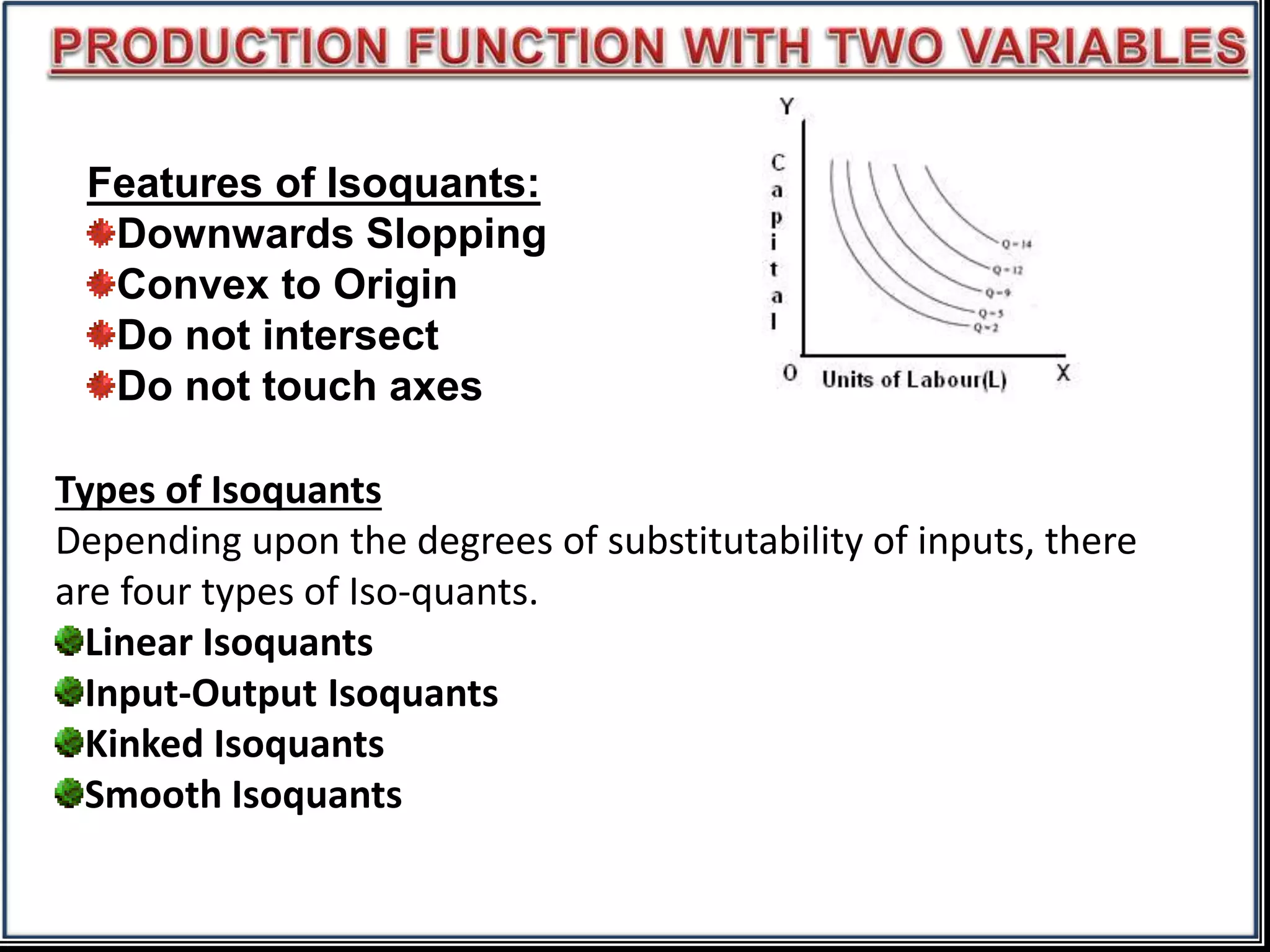

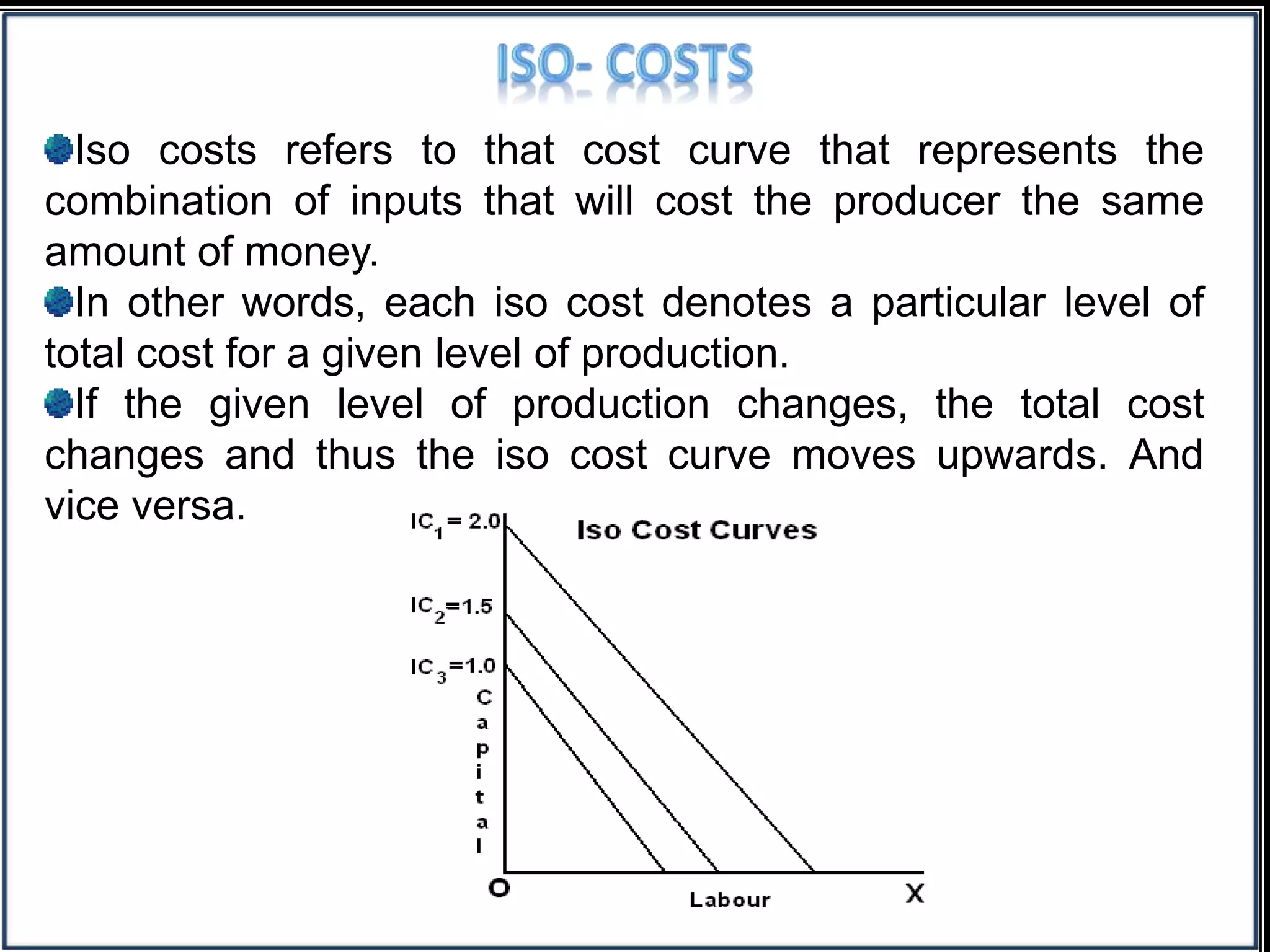

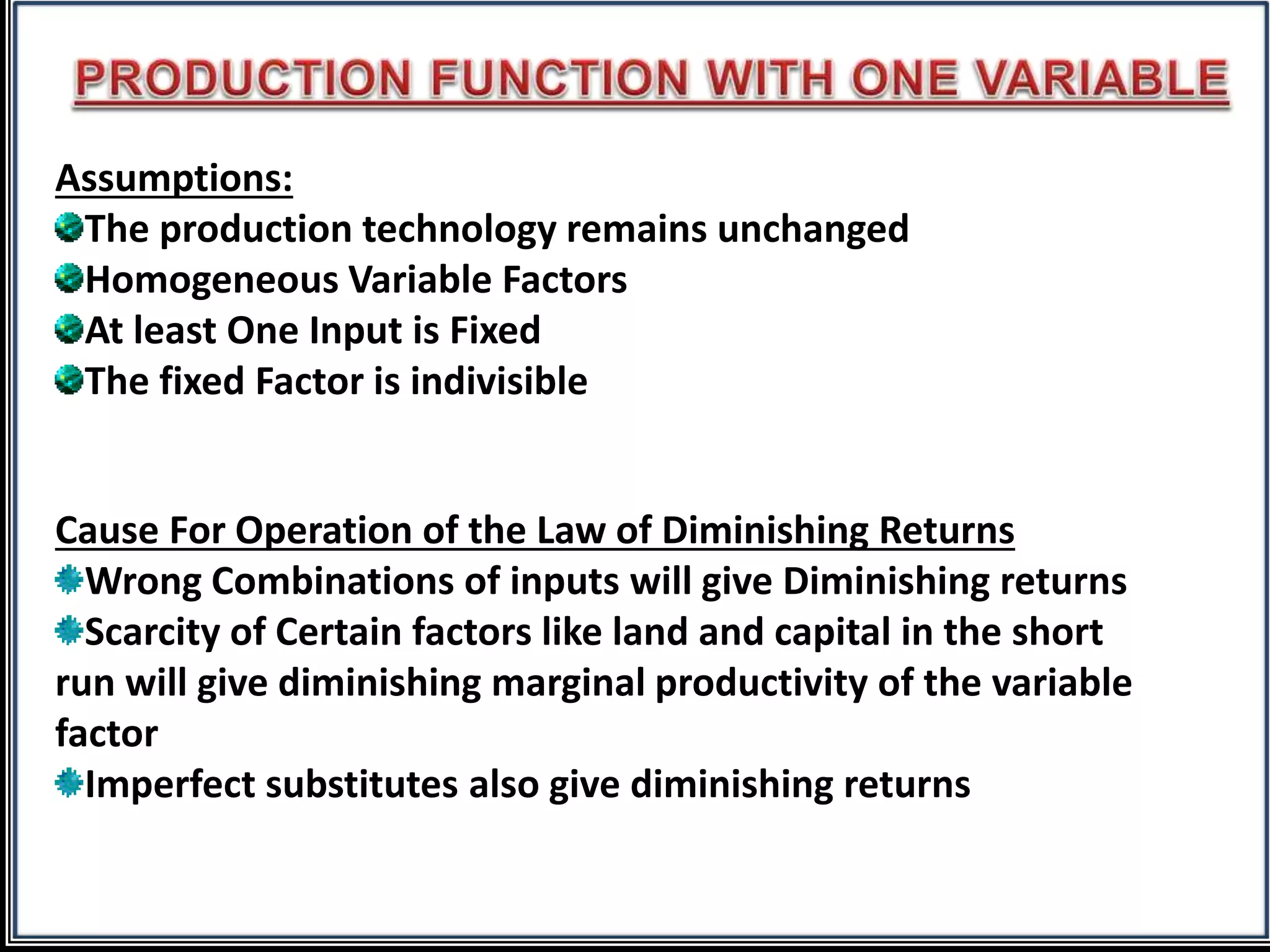

The document discusses production functions and the law of variable proportions. It defines production functions as relationships between inputs and outputs. Specifically, it discusses Cobb-Douglas production functions, which take the form of a power equation relating capital and labor to output. Isoquants and isocosts are also introduced as showing equal levels of output and cost from different input combinations. The law of variable proportions is summarized as explaining how adding more of a variable input initially increases then decreases marginal returns in the short run when one input is fixed.