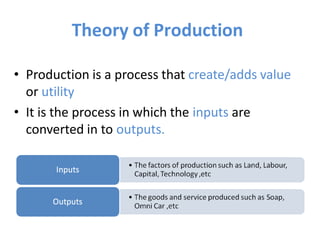

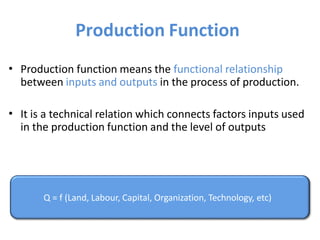

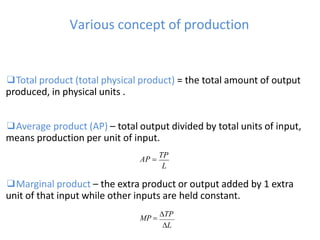

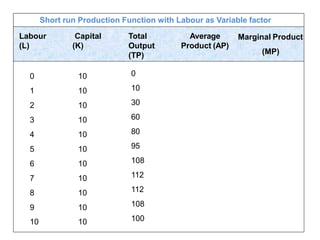

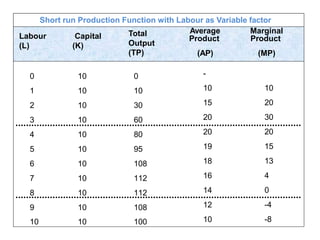

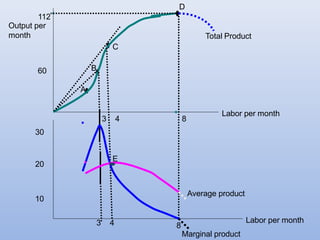

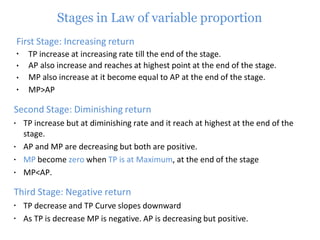

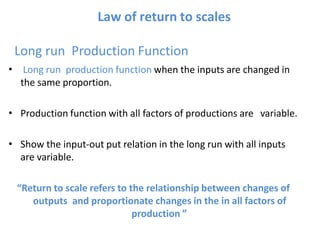

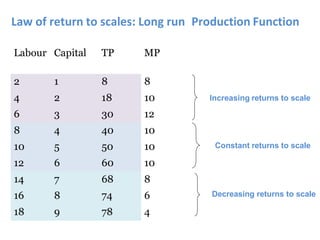

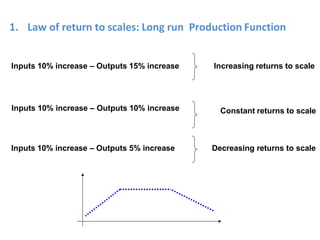

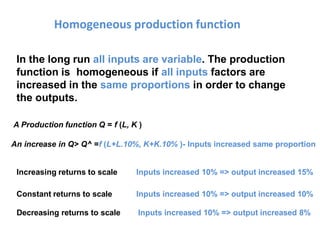

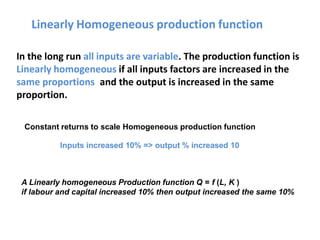

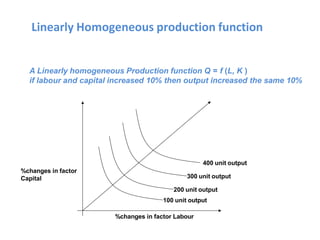

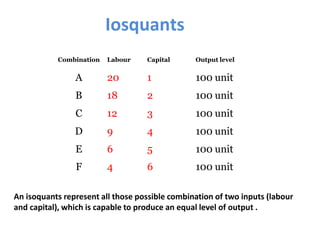

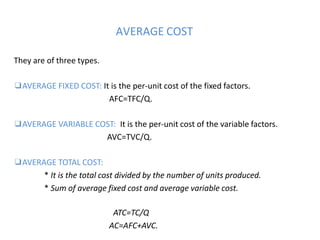

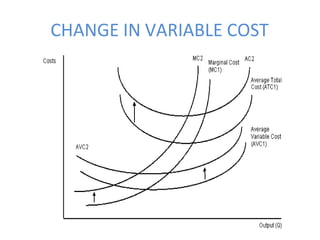

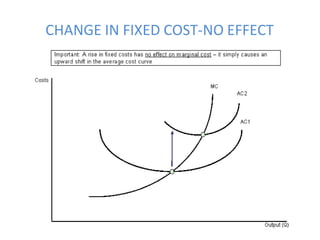

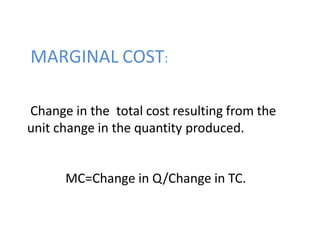

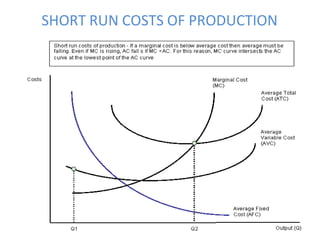

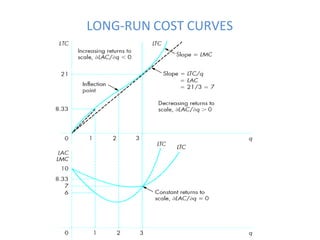

The document provides information on production theory and costs. It defines production as the process of converting inputs into outputs. The relationship between inputs and outputs is represented by the production function. There are laws of variable proportions that show how total product increases at different rates as variable inputs are added. Cost concepts like fixed, variable, total, average and marginal costs are introduced in the short run. Long run costs include economies of scale and different cost curves. Key economic principles like opportunity cost, sunk costs and accounting versus economic costs are also summarized.