Downloaded 161 times

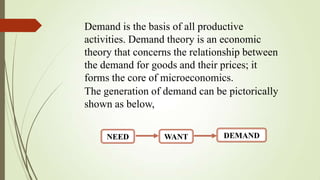

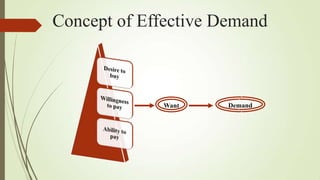

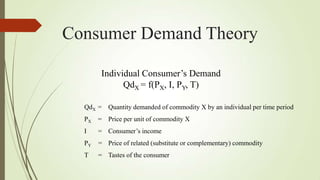

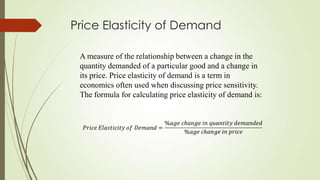

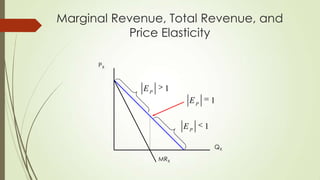

This document discusses demand theory and its implications in managerial economics. It defines demand as the basis of all productive activities and explains that demand theory forms the core of microeconomics and concerns the relationship between demand for goods and their prices. The document then covers various aspects of demand theory including individual consumer demand, the law of demand, market demand curves, demand faced by different market structures like monopoly and perfect competition, price elasticity of demand, and determinants of price elasticity.