and

present

A Summary of

Leveraged Buyout

(LBO) Models

2.

About JobSearchDigest.com

Every day our team researches all the online job

sources (including the specialty niche sites)

We capture every Hedge Fund, Private Equity,

Venture Capital and Investment Banking job

Daily email updates give you a competitive

advantage in your job search

www.JobSearchDigest.com

Copyright 2009

3.

About The InvestmentBanking Institute

Core financial, technical and modeling skills.

Similar to the top firms.

4 Weeks of training

– 28 hours of live, in-class instruction,

– Taught by current and former investment bankers.

Wide range of topics.

Classes monthly in major cities across the US,

Canada and Europe.

Visit www.ibtraining.com for additional details.

Copyright 2009

4.

Table of Contents

I. Uses for An LBO Model

II. Components of LBO Model

III. IRR Analysis

IV. Q&A

Copyright 2009

5.

Uses for anLBO Model

An LBO Model is an analysis used by private equity

firms (financial sponsors) to evaluate an acquisition

The goal of an LBO is to acquire a company by

financing the purchase with as much debt as cash flow

and debt markets will support

The more debt available, the smaller an equity

investment the financial sponsor has to make

The higher the leverage, the higher the expected IRR

for the financial sponsor or private equity firm

Copyright 2009

6.

Uses for anLBO Model (cont’d)

The goal of an LBO model is to establish expected

internal rates of return (“IRR”) for the acquisition

that reflects:

Purchase price assumptions and the cash needed

Capitalization assumptions: leverage, debt tranches, equity

investments

Base case financial projections for balance sheet, cash flow

and income statement

Model should include sensitivity functions for a

range of:

purchase prices,

capitalization structures,

operating assumptions

Copyright 2009

7.

Uses for anLBO Model (cont’d)

Private Equity Firms / Financial Sponsors usually have

a required rate of return hurdle

Expected transaction IRR must meet or exceed hurdle rate

PE firms required rates of return usually range from 15% to

30% (18% - 25% typical)

The IRR analysis is strongly driven by the amount of

leverage

With higher leverage, less equity, and higher IRR

Often the goal is to leverage up the Company based on cash

flow and the debt markets

More leverage increases risk, as cash flows will pay interest

and debt service

Copyright 2009

8.

Uses for anLBO Model (cont’d)

Leverage is largely determined by the debt markets

Until mid-2007, the debt markets were experiencing

excess liquidity

Lenders were allowing higher leverage

In 2005-2007 leveraged at 4.0–6.0x recent EBITDA

Higher levels allowed higher prices yet still attain

the required IRR

Copyright 2009

9.

Uses for anLBO Model (cont’d)

Leverage is comprised of some combination

of:

Senior secured loans

Junior loans/bonds

Mezzanine debt, or “hybrid” securities

Lenders may require the financial sponsor to

have a minimum equity investment

Minimum equity contribution is typically around

20% - 25% of total capitalization

Copyright 2009

10.

Uses for anLBO Model (cont’d)

Not Just for Buyers

The LBO Model is also used by lenders

Lenders like to see expected leverage and debt

service coverage ratios based upon Company’s

projected:

– income statement,

– balance sheet,

– cash flow

Copyright 2009

11.

Pop Quiz

Thegoal of an LBO model is to establish

expected internal rates of return (“IRR”)

using a financial model that reflects:

a. Purchase price assumptions and uses of cash

b. Capitalization assumptions and sources of cash

c. Base case financial projections with

assumptions

d. All the above.

Copyright 2009

12.

Pop Quiz

Thegoal of an LBO model is to establish

expected internal rates of return (“IRR”)

using a financial model that reflects:

a. Purchase price assumptions and uses of cash

b. Capitalization assumptions and sources of cash

c. Base case financial projections with

assumptions

d. All the above.

Copyright 2009

13.

I. Uses forAn LBO Model

II. Components of LBO Model

III. IRR Analysis

IV. Q&A

Copyright 2009

14.

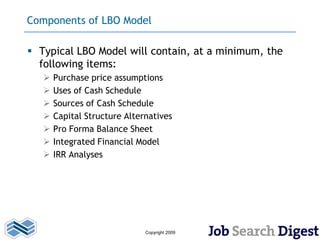

Components of LBOModel

Typical LBO Model will contain, at a minimum, the

following items:

Purchase price assumptions

Uses of Cash Schedule

Sources of Cash Schedule

Capital Structure Alternatives

Pro Forma Balance Sheet

Integrated Financial Model

IRR Analyses

Copyright 2009

15.

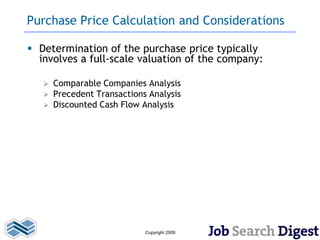

Purchase Price Calculationand Considerations

Determination of the purchase price typically

involves a full-scale valuation of the company:

Comparable Companies Analysis

Precedent Transactions Analysis

Discounted Cash Flow Analysis

Copyright 2009

16.

Sources and Usesof Cash

Total Uses is the amount of cash necessary to

complete the transaction

Total Sources is capital required to complete the

transaction

Copyright 2009

17.

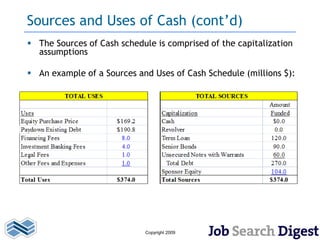

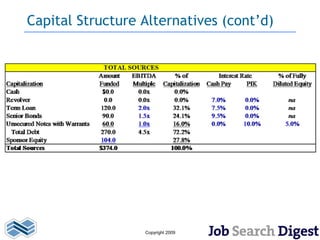

Sources and Usesof Cash (cont’d)

The Sources of Cash schedule is comprised of the capitalization

assumptions

An example of a Sources and Uses of Cash Schedule (millions $):

Copyright 2009

18.

Capital Structure Alternatives

Debt may be comprised of different securities

usually provided by different lenders

Revolver / Term loan (senior secured loans)

– Usually provided by typical commercial banks

– Have lower interest rates

Junior loans can be provided by public markets

(high yield issue) and private placements

Often, the most junior piece on debt will have

equity warrants attached

Copyright 2009

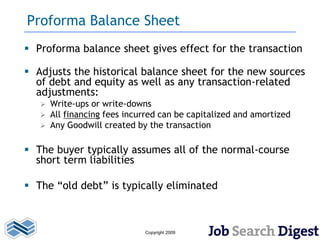

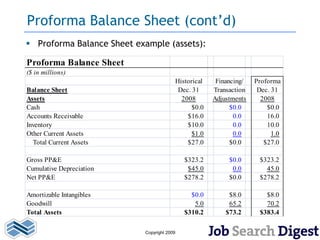

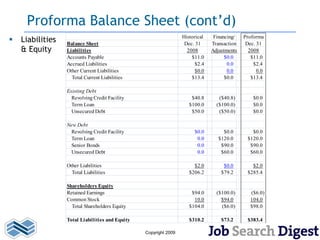

Proforma Balance Sheet

Proforma balance sheet gives effect for the transaction

Adjusts the historical balance sheet for the new sources

of debt and equity as well as any transaction-related

adjustments:

Write-ups or write-downs

All financing fees incurred can be capitalized and amortized

Any Goodwill created by the transaction

The buyer typically assumes all of the normal-course

short term liabilities

The “old debt” is typically eliminated

Copyright 2009

Proforma Balance Sheet(cont’d)

Liabilities Balance Sheet

Historical

Dec. 31

Financing/

Transaction

Proforma

Dec. 31

& Equity Liabilities 2008 Adjustments 2008

Accounts Payable $11.0 $0.0 $11.0

Accrued Liabilities $2.4 0.0 $2.4

Other Current Liabilities $0.0 0.0 0.0

Total Current Liabilities $13.4 $0.0 $13.4

Existing Debt

Revolving Credit Facility $40.8 ($40.8) $0.0

Term Loan $100.0 ($100.0) $0.0

Unsecured Debt $50.0 ($50.0) $0.0

New Debt

Revolving Credit Facility $0.0 $0.0 $0.0

Term Loan 0.0 $120.0 $120.0

Senior Bonds 0.0 $90.0 $90.0

Unsecured Debt 0.0 $60.0 $60.0

Other Liabilities $2.0 $0.0 $2.0

Total Liabilities $206.2 $79.2 $285.4

Shareholders Equity

Retained Earnings $94.0 ($100.0) ($6.0)

Common Stock 10.0 $94.0 104.0

Total Shareholders Equity $104.0 ($6.0) $98.0

Total Liabilities and Equity $310.2 $73.2 $383.4

Copyright 2009

23.

Financial Statement Projections

An LBO model must also include forecasted income

statement, balance sheet, cash flow and debt

schedule

This allows us to forecast performance of the

company on a post-LBO basis to see:

How well the company is able to service the increased debt;

How profitable the company can be following the LBO; and

How the company might be valued at the end of the

anticipated holding period

Copyright 2009

24.

Pop Quiz

Whichof the following is not included in total

uses of cash?

a. purchase price

b. transaction fees

c. debt service

d. other required cash payments in the transaction

e. none

Copyright 2009

25.

Pop Quiz

Whichof the following is not included in total

uses of cash?

a. purchase price

b. transaction fees

c. debt service

d. other required cash payments in the transaction

e. none

Copyright 2009

26.

I. Uses forAn LBO Model

II. Components of LBO Model

III. IRR Analysis

IV. Q&A

Copyright 2009

27.

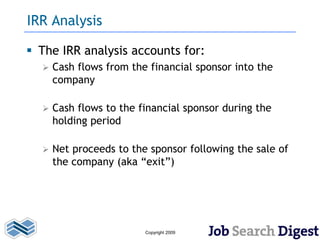

IRR Analysis

TheIRR analysis accounts for:

Cash flows from the financial sponsor into the

company

Cash flows to the financial sponsor during the

holding period

Net proceeds to the sponsor following the sale of

the company (aka “exit”)

Copyright 2009

28.

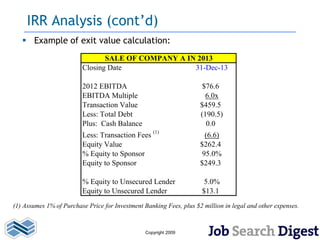

IRR Analysis (cont’d)

Example of exit value calculation:

SALE OF COMPANY A IN 2013

Closing Date 31-Dec-13

2012 EBITDA $76.6

EBITDA Multiple 6.0x

Transaction Value $459.5

Less: Total Debt (190.5)

Plus: Cash Balance 0.0

Less: Transaction Fees (1) (6.6)

Equity Value $262.4

% Equity to Sponsor 95.0%

Equity to Sponsor $249.3

% Equity to Unsecured Lender 5.0%

Equity to Unsecured Lender $13.1

(1) Assumes 1% of Purchase Price for Investment Banking Fees, plus $2 million in legal and other expenses.

Copyright 2009

29.

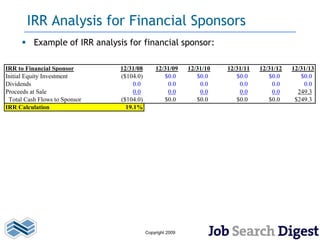

IRR Analysis forFinancial Sponsors

Example of IRR analysis for financial sponsor:

IRR to Financial Sponsor 12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13

Initial Equity Investment ($104.0) $0.0 $0.0 $0.0 $0.0 $0.0

Dividends 0.0 0.0 0.0 0.0 0.0 0.0

Proceeds at Sale 0.0 0.0 0.0 0.0 0.0 249.3

Total Cash Flows to Sponsor ($104.0) $0.0 $0.0 $0.0 $0.0 $249.3

IRR Calculation 19.1%

Copyright 2009

30.

Pop Quiz

TheIRR analysis accounts for:

a. Cash flows from the financial sponsor into

the company

b. Cash flows to the financial sponsor during

the holding period

c. Net proceeds to the sponsor following the

sale of the company

d. All of the above

Copyright 2009

31.

Pop Quiz

TheIRR analysis accounts for:

a. Cash flows from the financial sponsor into

the company

b. Cash flows to the financial sponsor during

the holding period

c. Net proceeds to the sponsor following the

sale of the company

d. All of the above

Copyright 2009

32.

I. Uses forAn LBO Model

II. Construction of LBO Model

III. IRR Analysis

IV. Q&A

Copyright 2009

33.

Q&A

Q: When isthe LBO considered an

appropriate method over other

financing options?

Copyright 2009

34.

Q&A

Q: How havecurrent market

conditions affected the LBO

model?

Copyright 2009

About Investment BankingInstitute

The Investment Banking Institute (IBI), with offices in 14 cities

throughout North America and Europe, conducts corporate as

well as individual training for candidates ranging from

Managing Directors to MBAs to College Undergrads and other

professionals seeking to enter the industry. Since our inception

in 2002, IBI has offered the most comprehensive course

syllabus and longest running program available

IBI conducts more individual based programs in more cities

than any other firm. Last year alone (2008) we held over 700

sessions worldwide for more than 2000 live training hours;

moreover, our bankers/instructors possess a combined 129

years of I-banking and/or PE experience

Copyright 2009

40.

About Investment BankingInstitute

IBI is affiliated with the CFA Institute, NASBA (the national

association of the state boards of accountancy –overseeing

CPAs), and the CFP Board

IBI has trained analysts and associates for hundreds of

organizations (a partial list can be viewed on our website), the

in-class training we provide our individual students is the same

exact training provided to corporate clients

Interview preparation, resume revision, and job contacts are

available through our Human Resources division on a one-on-

one basis with no set expiration date

The training program can be repeated free of charge at any

future date to ensure your skills are sharp when you need them

to be

Seasoned Investment Bankers are available for help outside of

class whenever needed

Copyright 2009

41.

Investment Banking Institute Student Testimonial

I am so thankful for the class I took at the Investment Banking Institute. It was both

an enriching knowledge vault and a confidence booster!

Your walkthrough of the DCF calculations was an excellent refresher. While I still

remember bits and pieces of how DCF works from my on-campus interviews back in

college and work at JP Morgan, your presentation helped to consolidate everything

in my mind. I also appreciate how you tied things back to an estimate of the

company's stock price at the end -- I actually once got an interview question on that

exact topic! The details and examples of the LBO modeling were extremely helpful,

and the encouragement you gave students throughout the class was equally

invaluable.

A huge thank-you for your insight into current market conditions, and on how the

subprime crisis actually unfolded. Although I manage to gain exposure to

macroeconomic and market valuation issues at work every day at JP Morgan, it was

your engaging, concise teaching method and holistic approach to the course that

put everything in perspective for me.

I will definitely recommend your course to my future classmates at Harvard Business

School as I am sure they will benefit tremendously from it.

Thank you very much.

Anthony, Boston

Copyright 2009

42.

Investment Banking Institute

Please visit us at

www.ibtraining.com

For company information, banker’s bios, and contact

information for any of our local offices

Headquarters:

The Helmsley Building

230 Park Avenue, 10th Floor

New York, NY 10169

212-380-7027

Copyright 2009