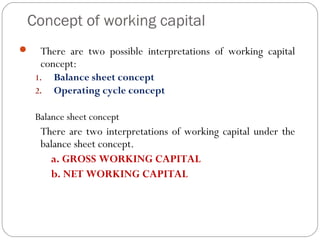

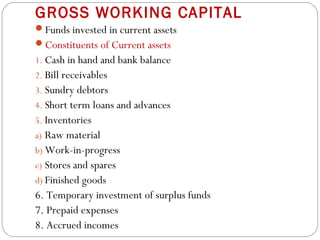

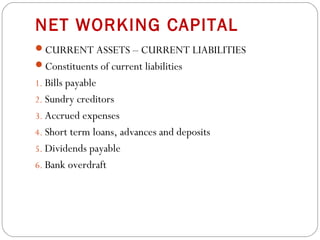

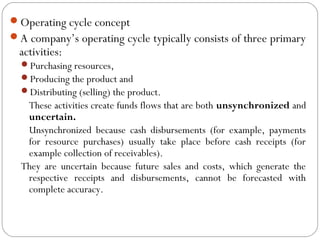

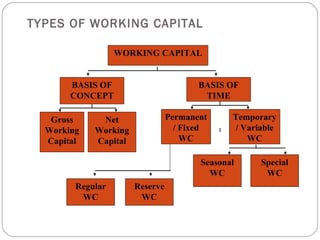

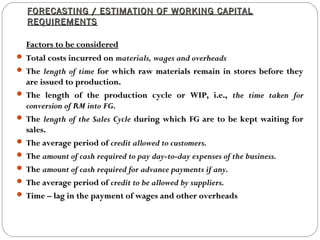

Working capital refers to the capital required to finance short-term assets like cash, inventory, and accounts receivable. It is needed to ensure a company has enough liquidity to operate day-to-day and take advantage of opportunities. There are two main concepts of working capital - the balance sheet approach looks at it as current assets minus current liabilities, while the operating cycle approach sees it revolving as assets are purchased, produced as inventory, and sold to generate receivables. Proper management of working capital is important, as too much can be unprofitable while too little can threaten solvency. Forecasting working capital needs considers factors like production costs, credit terms, and cash requirements.