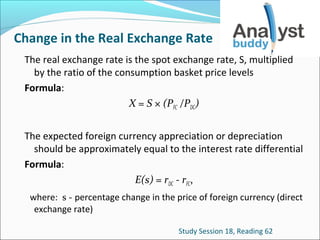

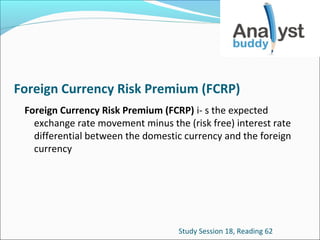

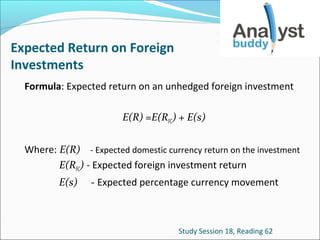

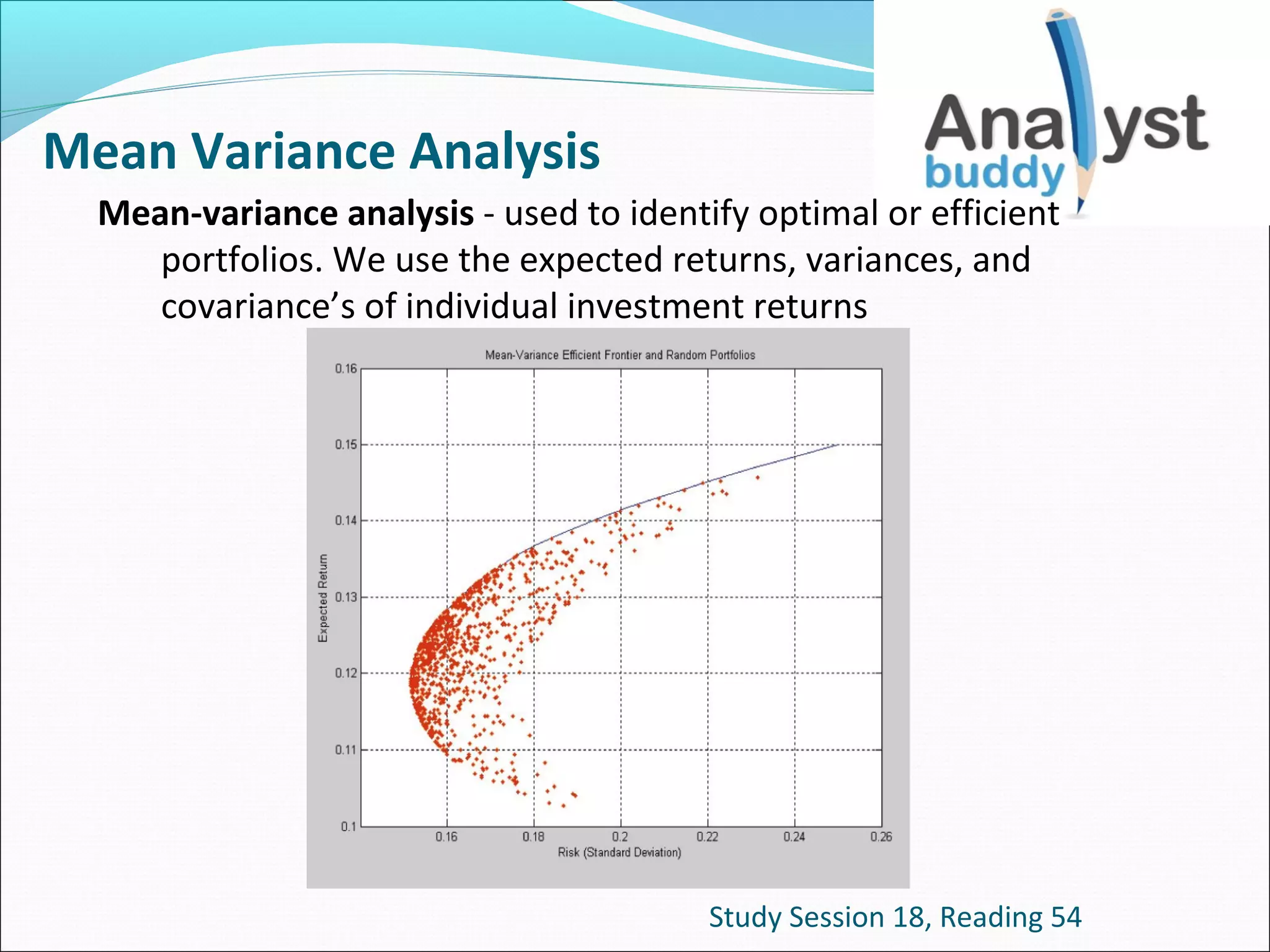

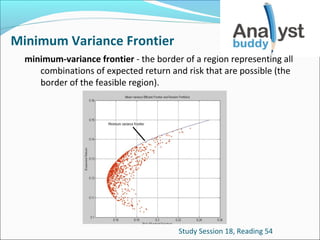

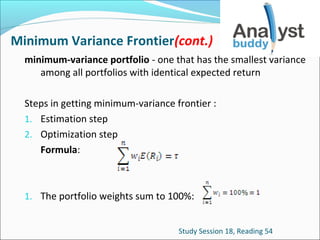

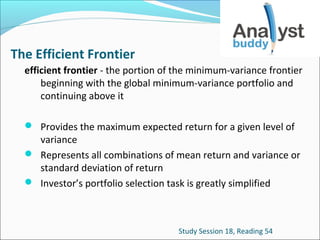

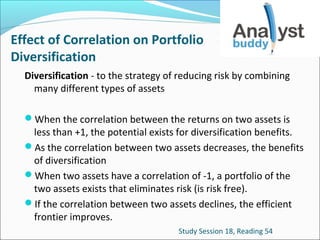

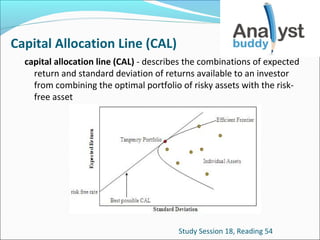

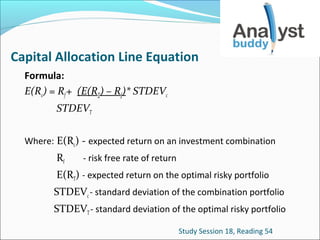

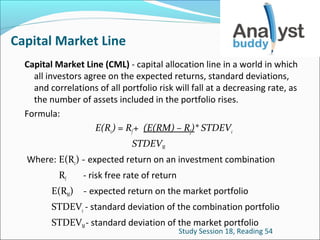

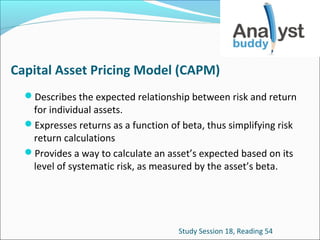

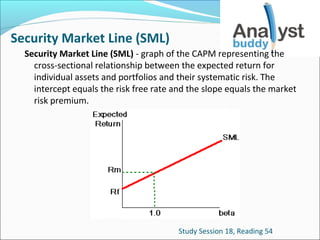

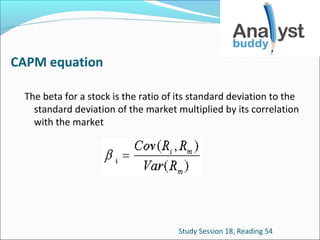

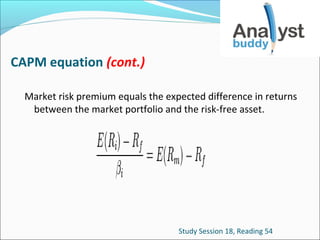

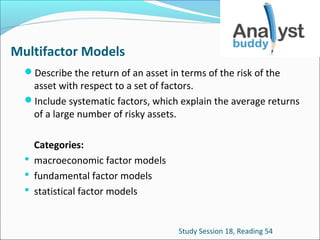

Mean-variance analysis is used to identify optimal portfolios based on expected returns, variances, and covariances of asset returns. The minimum-variance frontier shows the efficient combinations of expected return and risk. The efficient frontier begins with the global minimum-variance portfolio and provides the maximum expected return for a given level of variance. The capital market line describes combinations of the risk-free asset and market portfolio. The capital asset pricing model expresses expected returns as a linear function of systematic risk measured by beta.

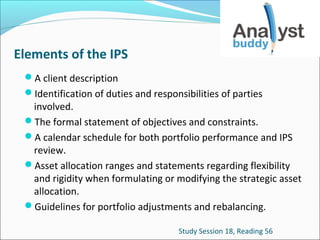

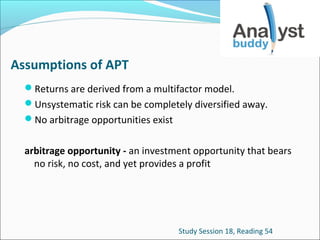

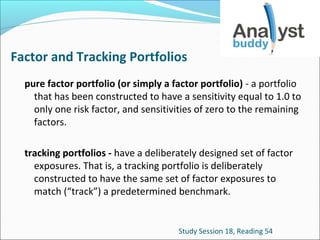

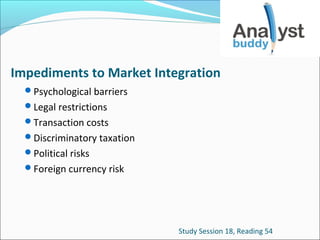

![Security Market Line (SML) (cont.)

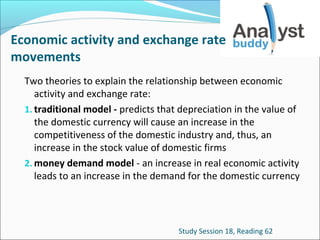

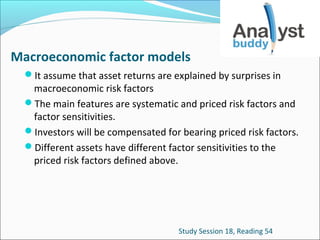

Security Market Line (SML) Equation:

E(Ri) = RF + βi[E(RM – RF)]

Where: E(Ri) - expected return on the asset

RF

- risk free rate of return

βi

- beta of the asset

E(RM – RF)]- expected risk premium

Study Session 18, Reading 54](https://image.slidesharecdn.com/l2flashcardsportfoliomanagement-ss18-131222035812-phpapp02/85/L2-flash-cards-portfolio-management-SS-18-19-320.jpg)

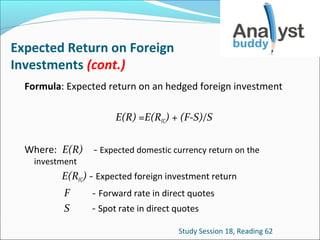

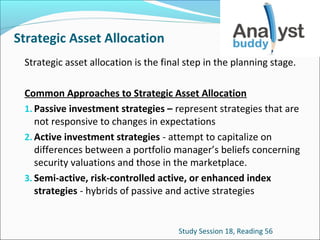

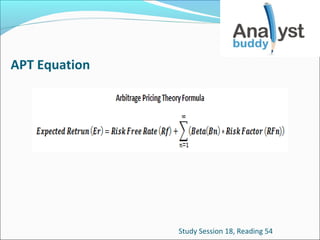

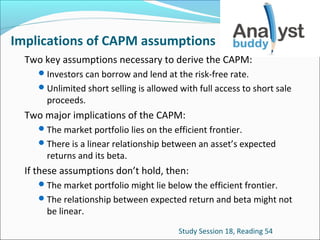

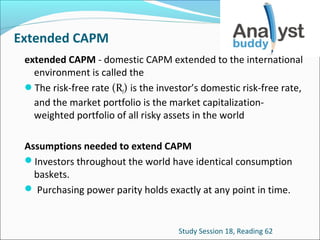

![ICAPM Equation

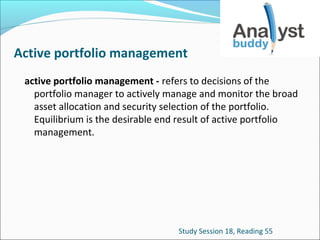

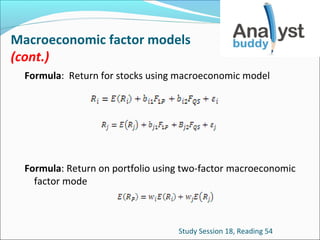

E(r)= Rf +(βg×MrPg )+(g1×FcrP1)+(g2×FcrP2 )+...........+(gk ×FcrPk )

Where: E(r) - asset’s expected return

Rrf - domestic currency risk-free rate

βg - sensitivity of the asset’s domestic currency returns to

changes in the global market portfolio

MrPg - world market risk premium [E(rm ) - r ]

E(r m) - expected return on world market portfolio

g1 to gk - sensitivities of asset’s domestic currency returns to

changes in the values of currencies 1 through k

FcrP1 to FcrPk - foreign currency risk premiums on

currencies 1 through k

Study Session 18, Reading 62](https://image.slidesharecdn.com/l2flashcardsportfoliomanagement-ss18-131222035812-phpapp02/85/L2-flash-cards-portfolio-management-SS-18-43-320.jpg)