Downloaded 30 times

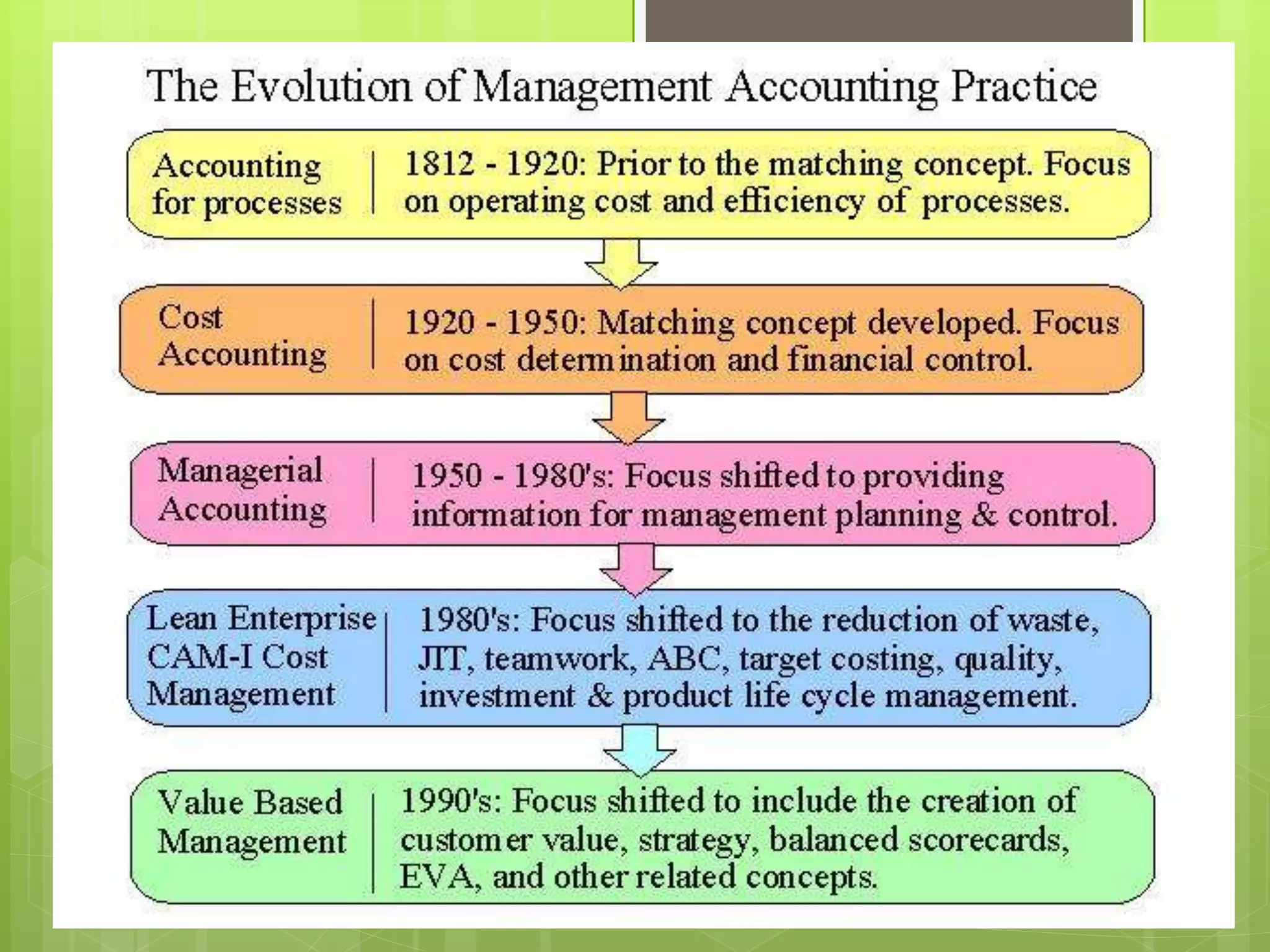

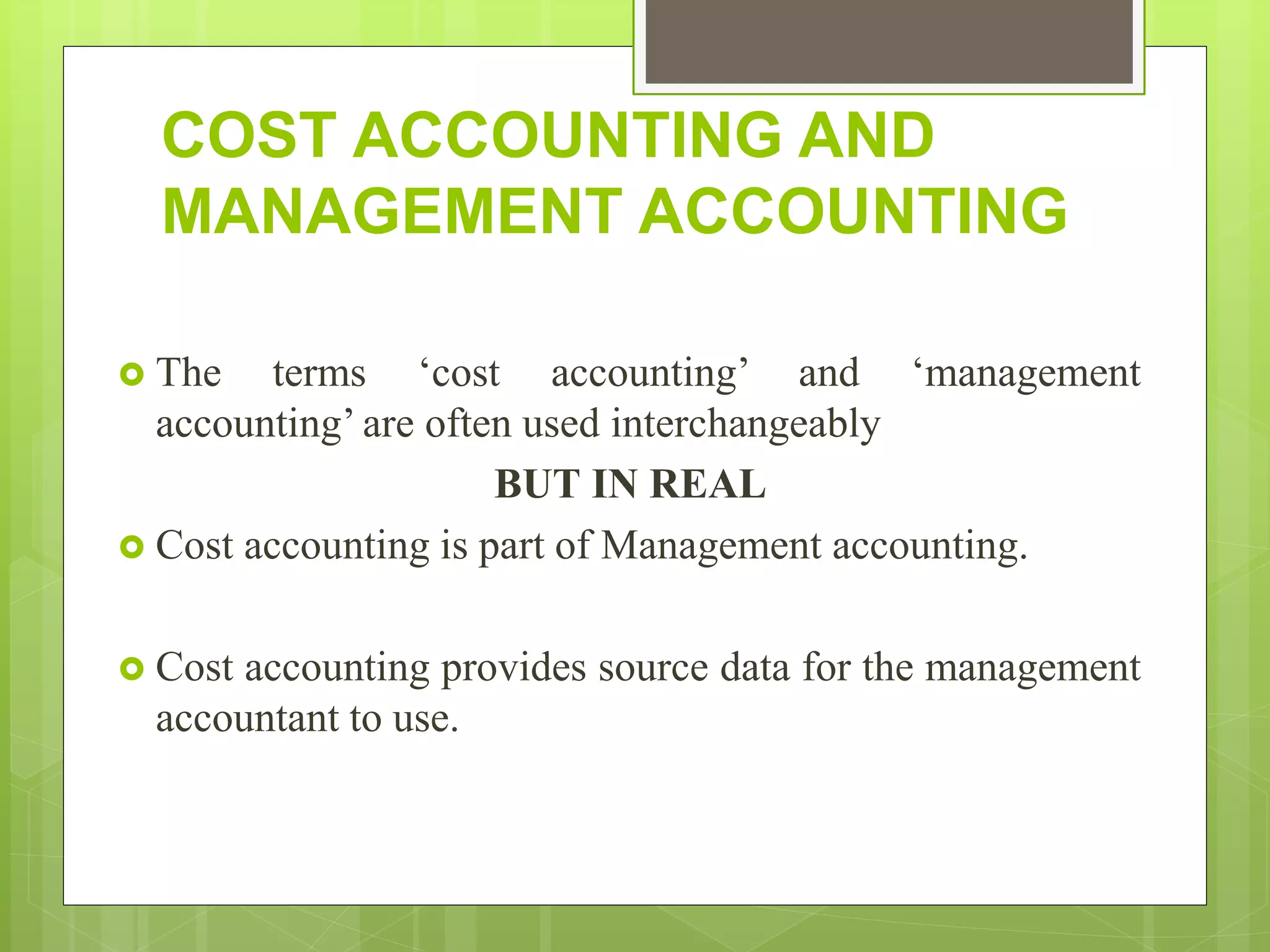

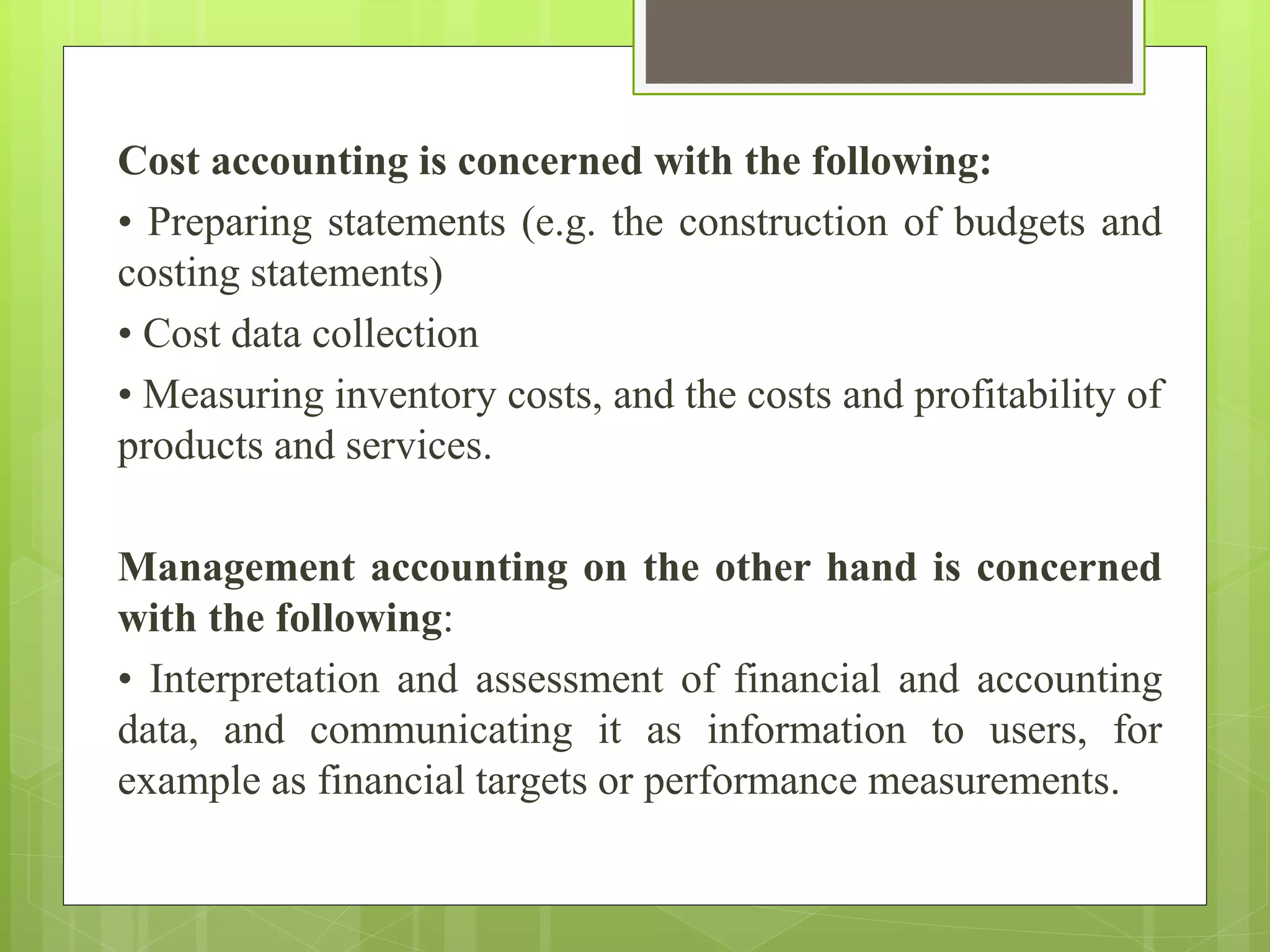

This document provides an introduction to management accounting. It defines management accounting as measuring, analyzing, and reporting financial and non-financial information to help managers make decisions to achieve organizational goals. The objectives of management accounting are to assist management in planning, organizing, directing and controlling, and to provide relevant information for decision-making. Management accounting provides data, modifies accounting data for planning and decisions, analyzes and interprets data, facilitates control, and uses qualitative information. It is distinguished from financial accounting in its objectives, analytical focus, data used, treatment of non-monetary factors, and periodicity of reporting. Cost accounting is a part of management accounting that provides source data.