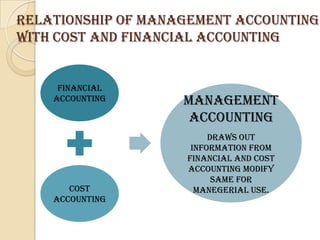

Management accounting provides information to internal managers to help them plan, direct operations, and control the organization. It involves tasks like modifying accounting data, analyzing and interpreting financial information, and facilitating management control through tools like standard costing and budgeting. Management accounting focuses on both financial and qualitative information to satisfy the needs of different management levels for decision making.