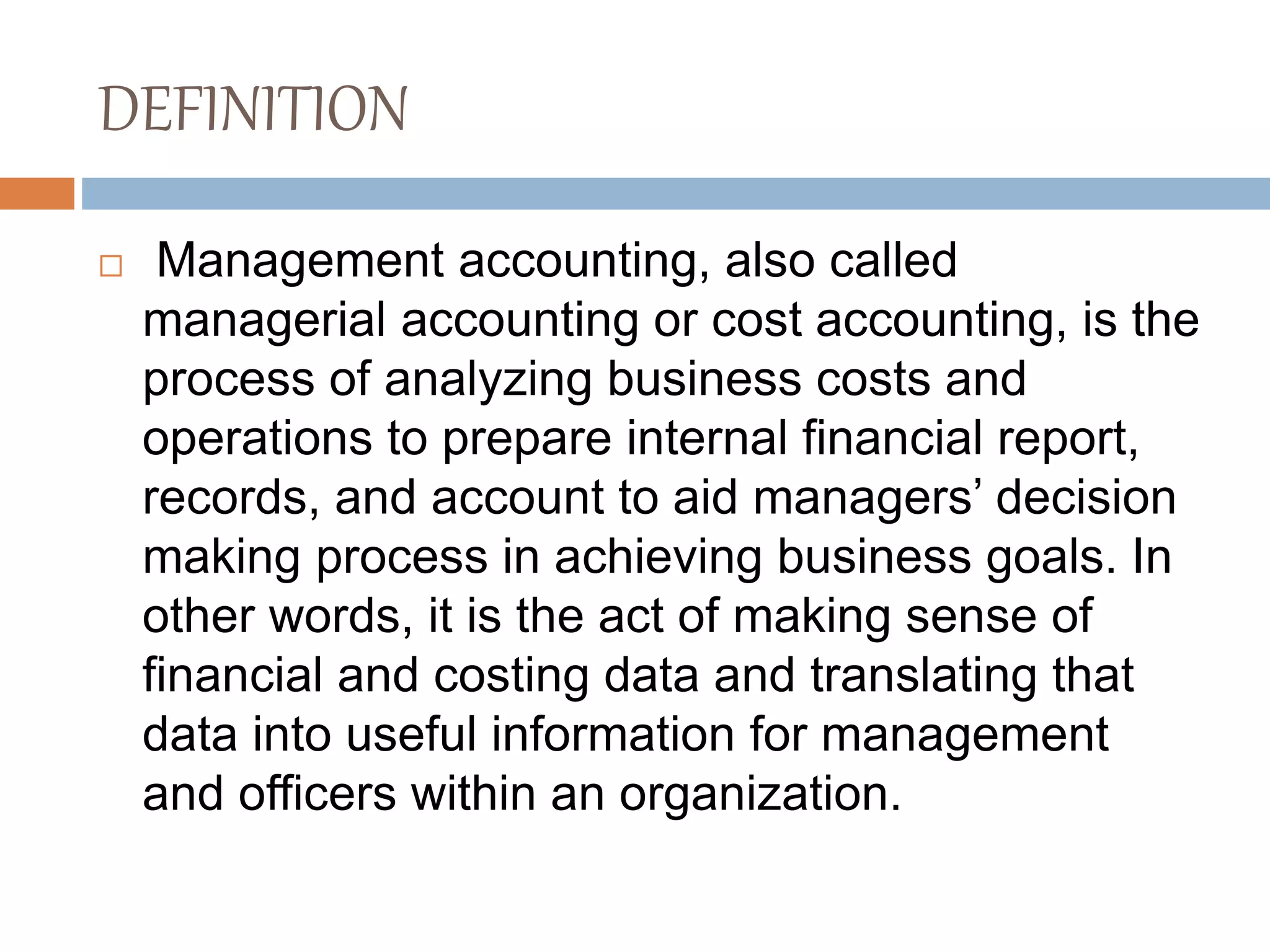

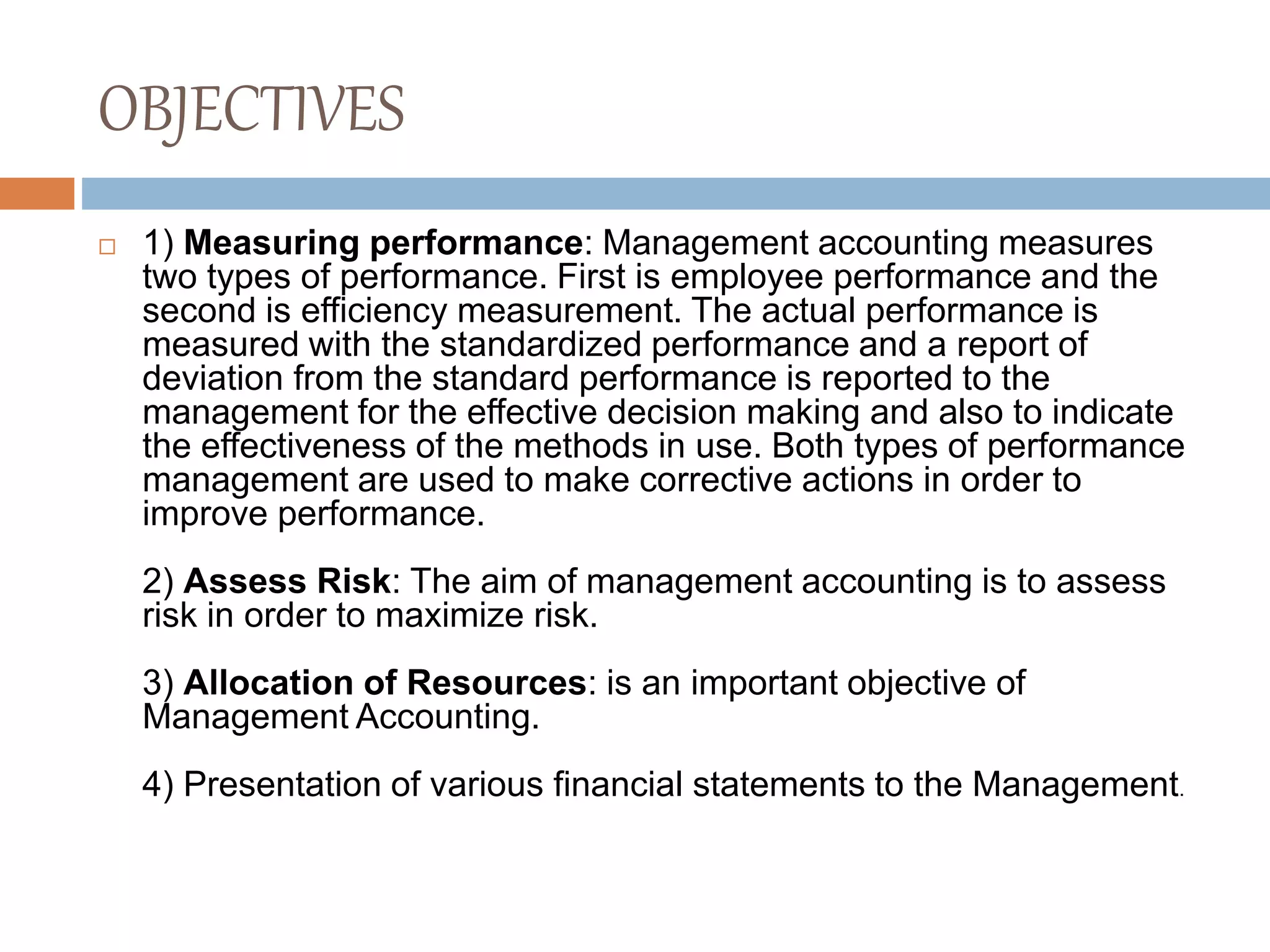

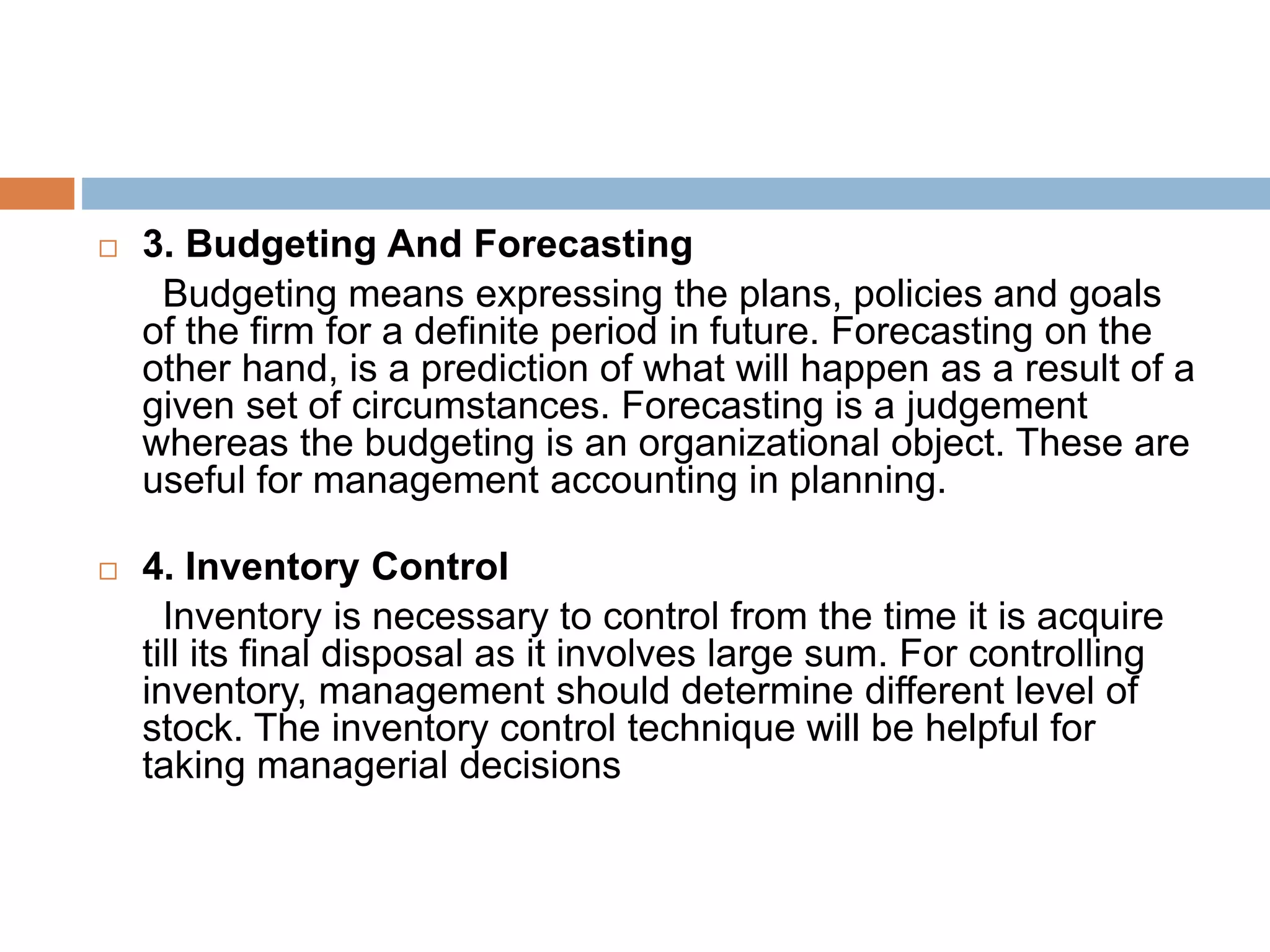

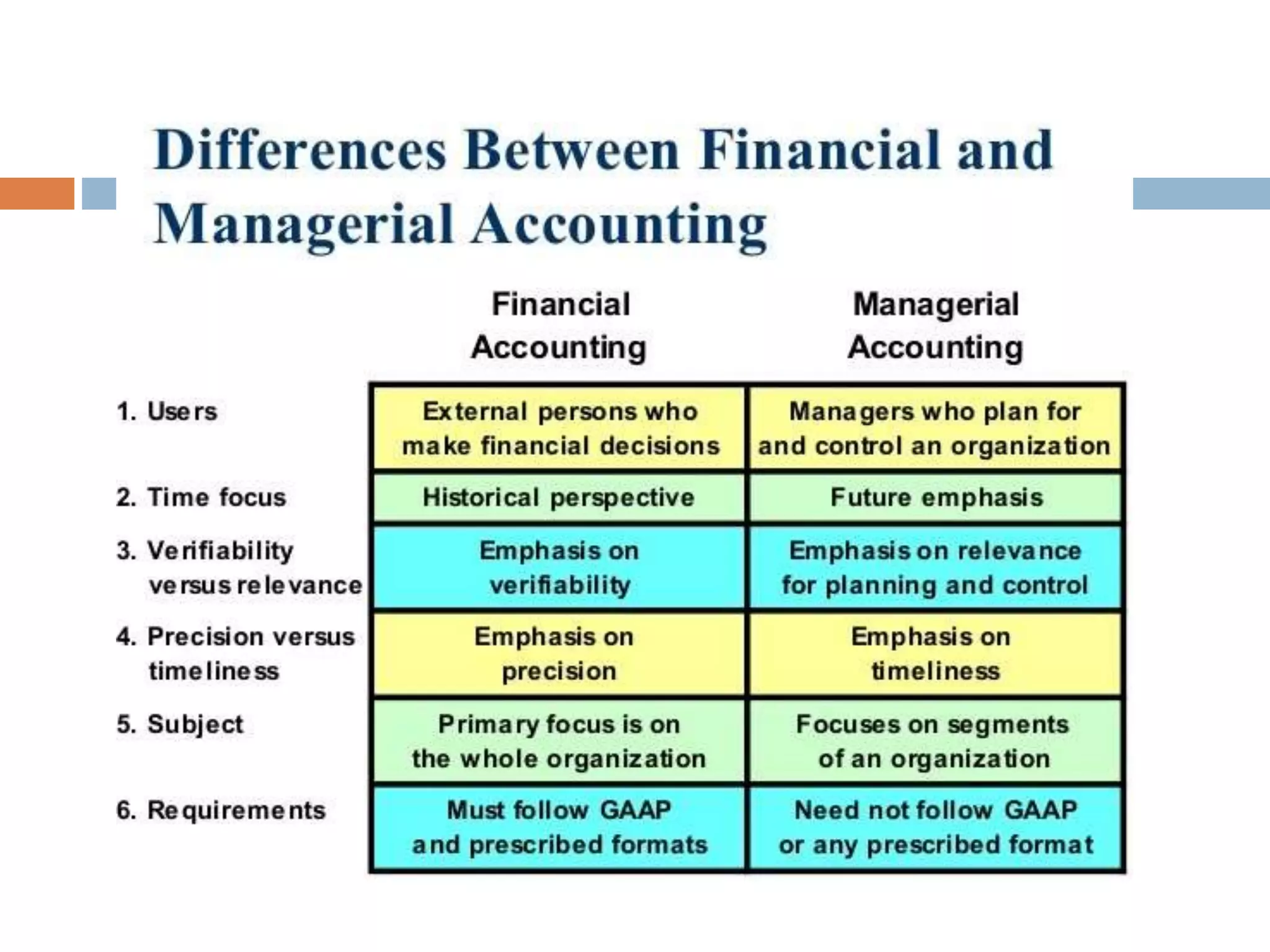

Management accounting is the process of analyzing business costs and operations to prepare internal reports and records to aid managers' decision-making. It involves collecting accounting information using financial and cost accounting and translating it into useful information for management. The objectives of management accounting include measuring performance, assessing risk, allocating resources, and presenting financial statements. It uses tools like budgeting, variance analysis, and cash flow analysis to help managers with planning, decision-making, and control.