Downloaded 224 times

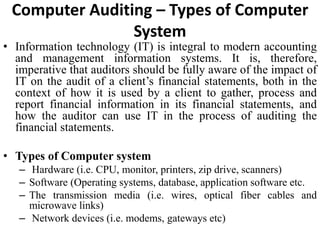

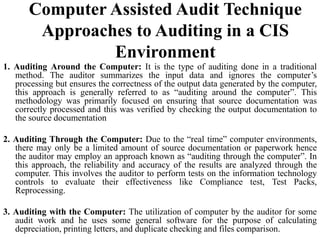

This document discusses auditing in a computerized environment. It describes the different types of computer systems including hardware, software, and transmission media. It outlines three approaches to auditing in a computer information system (CIS) environment: auditing around, through, and with the computer. The document also discusses characteristics of a CIS environment, internal controls including general and application controls, input, processing, and output controls, special considerations for auditing e-commerce transactions, and computer-assisted audit tools and techniques (CAATs).