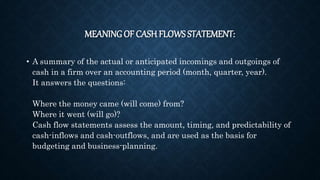

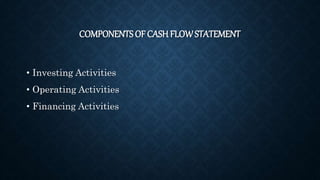

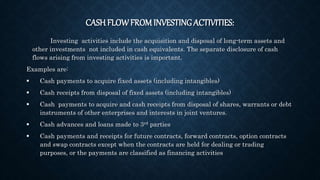

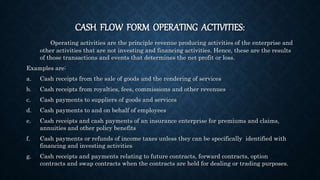

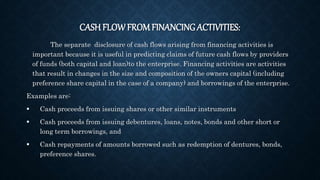

The document discusses the components of a cash flow statement, which includes cash flows from operating activities, investing activities, and financing activities. It provides examples of cash inflows and outflows for each category. Operating activities include cash from sales and payments to suppliers and employees. Investing activities consist of cash flows for purchasing/selling long-term assets. Financing activities contain cash from issuing shares/bonds and repaying amounts borrowed. The cash flow statement assesses cash inflows and outflows over a period to evaluate financial performance and assist with budget planning.