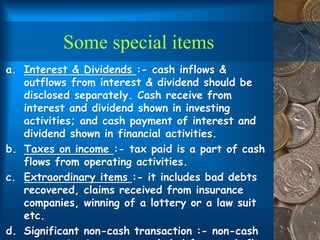

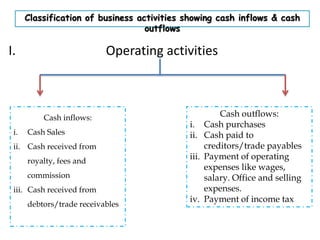

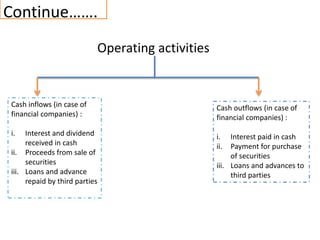

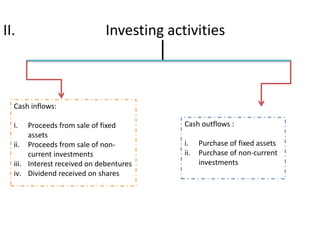

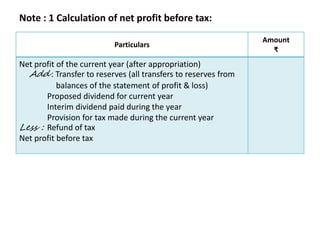

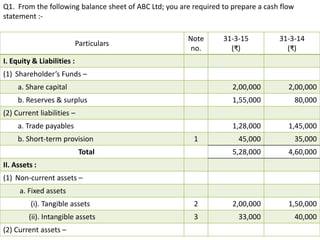

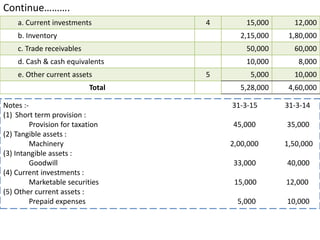

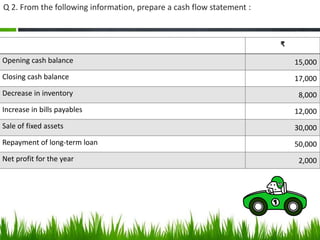

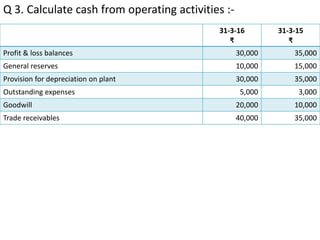

The document is a detailed project on cash flow statements, outlining their meaning, objectives, uses, limitations, and how to prepare them. It explains the difference between cash flow statements and cash budgets, as well as the classification of cash flows into operating, investing, and financial activities. Examples, illustrations, and cash flow statement formats for various companies are also provided, along with specific cases and calculations.