Downloaded 28 times

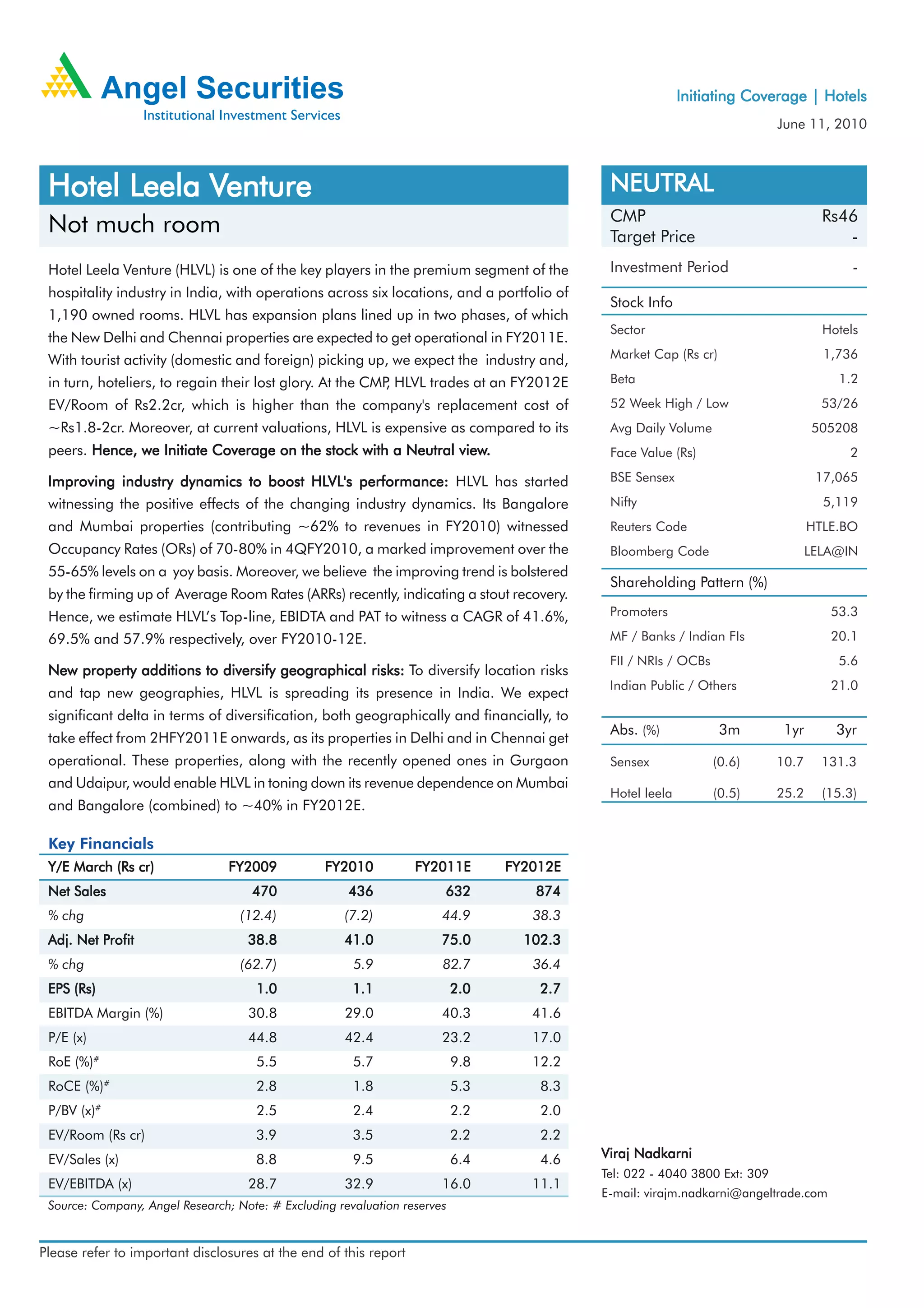

Hotel Leela Venture (HLVL) is a major player in India's premium hotel industry, operating six properties with 1,190 owned rooms. HLVL plans to expand in two phases, opening new properties in New Delhi and Chennai in fiscal year 2011. While the global recession and terrorism hurt the industry, tourism is recovering as foreign tourist arrivals and average room rates increase. HLVL's revenues, EBITDA, and profits are expected to grow rapidly over the next few years. The company is diversifying geographically through new properties to reduce reliance on Mumbai and Bangalore, which currently contribute about 62% of revenues. However, HLVL currently trades at a higher valuation than replacement cost and peers, leading to an