Downloaded 20 times

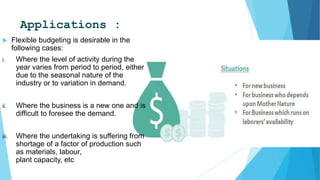

This document discusses flexible budgets. It defines a flexible budget as a budget that changes based on different output levels to recognize varying cost behavior patterns. Flexible budgets are prepared for a range of activity levels rather than a single level. They provide a dynamic basis for comparison and a tailored budget for each output volume. Some key advantages are determining costs, sales, and profits at different operating capacities and identifying profit areas.