Download to read offline

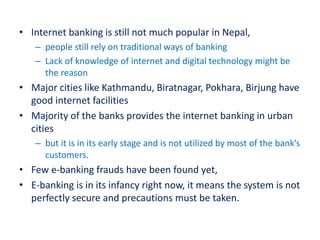

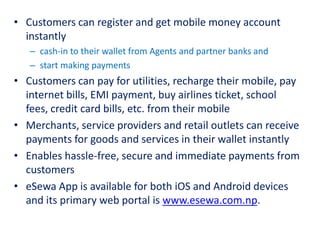

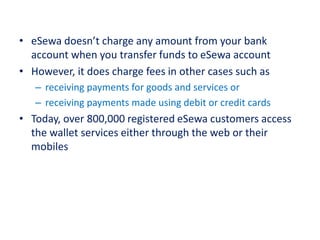

Electronic banking in Nepal allows customers to conduct transactions online without visiting banks, using the internet for services like fund transfers and bill payments. Although e-banking is still in its infancy in Nepal, with low internet banking usage and significant reliance on traditional banking methods, services like eSewa have improved payment convenience since its launch in 2009. Many banks offer internet banking mainly in urban areas, but security concerns and limited knowledge hinder wider adoption among the population.