Download to read offline

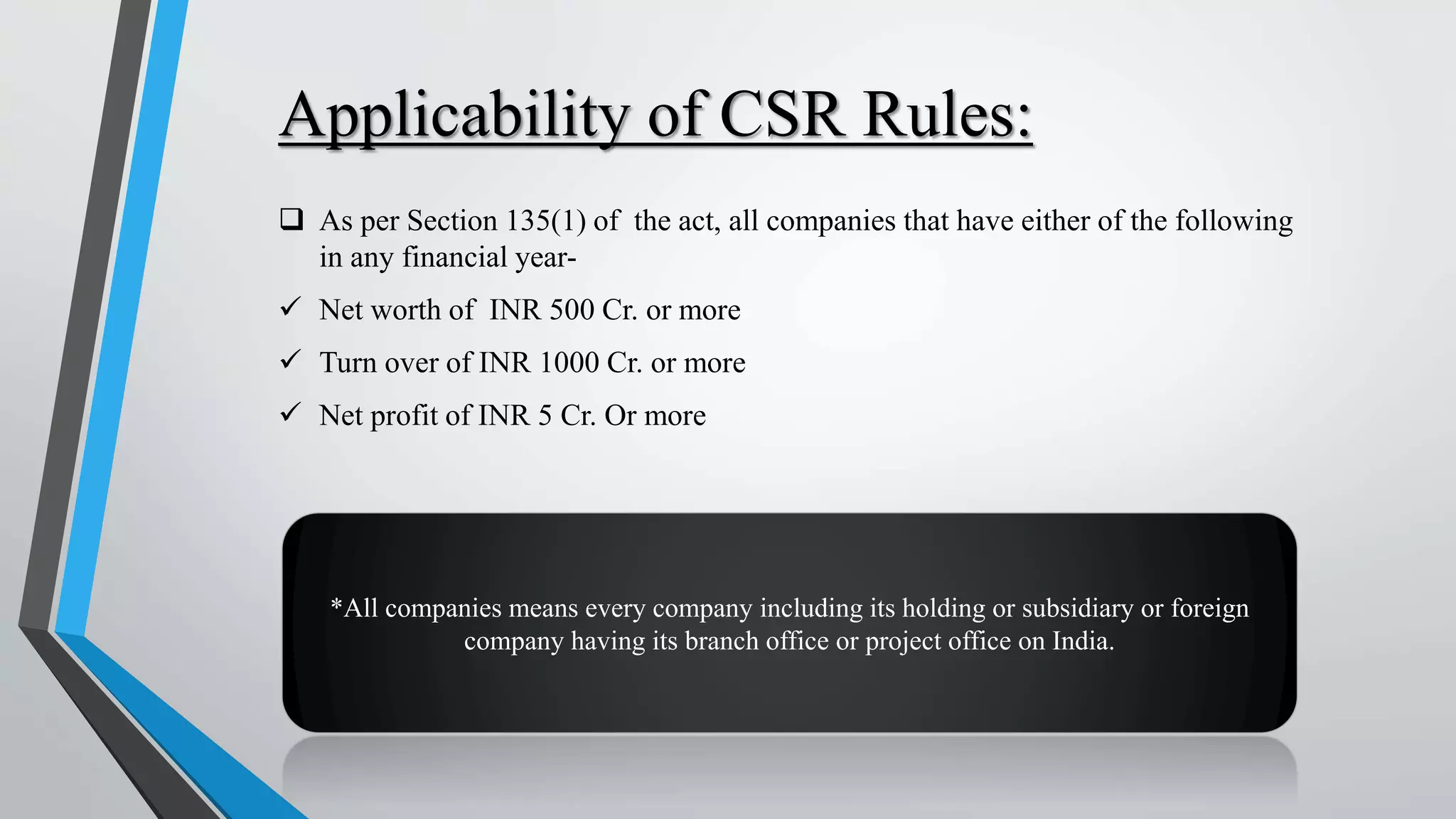

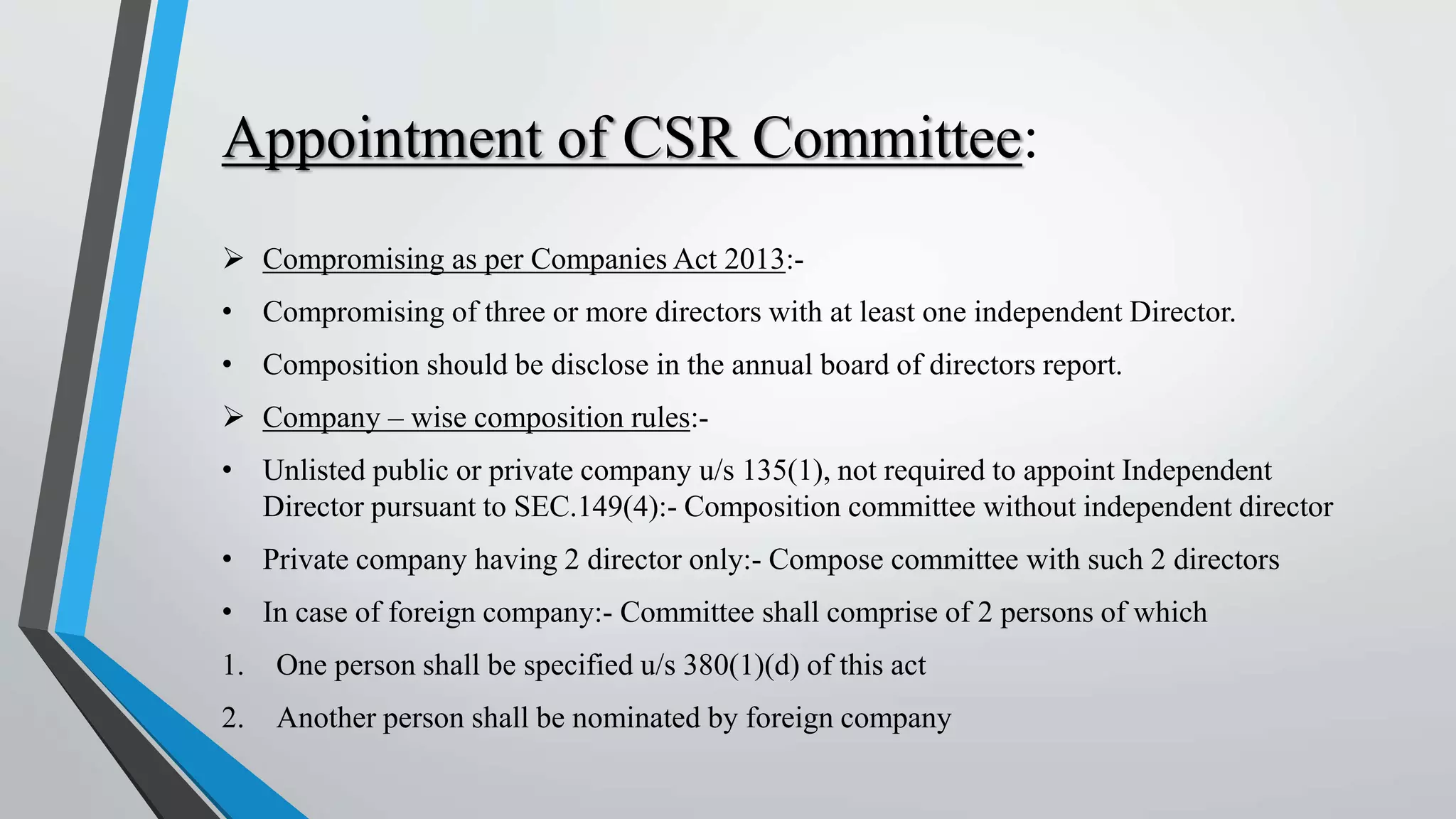

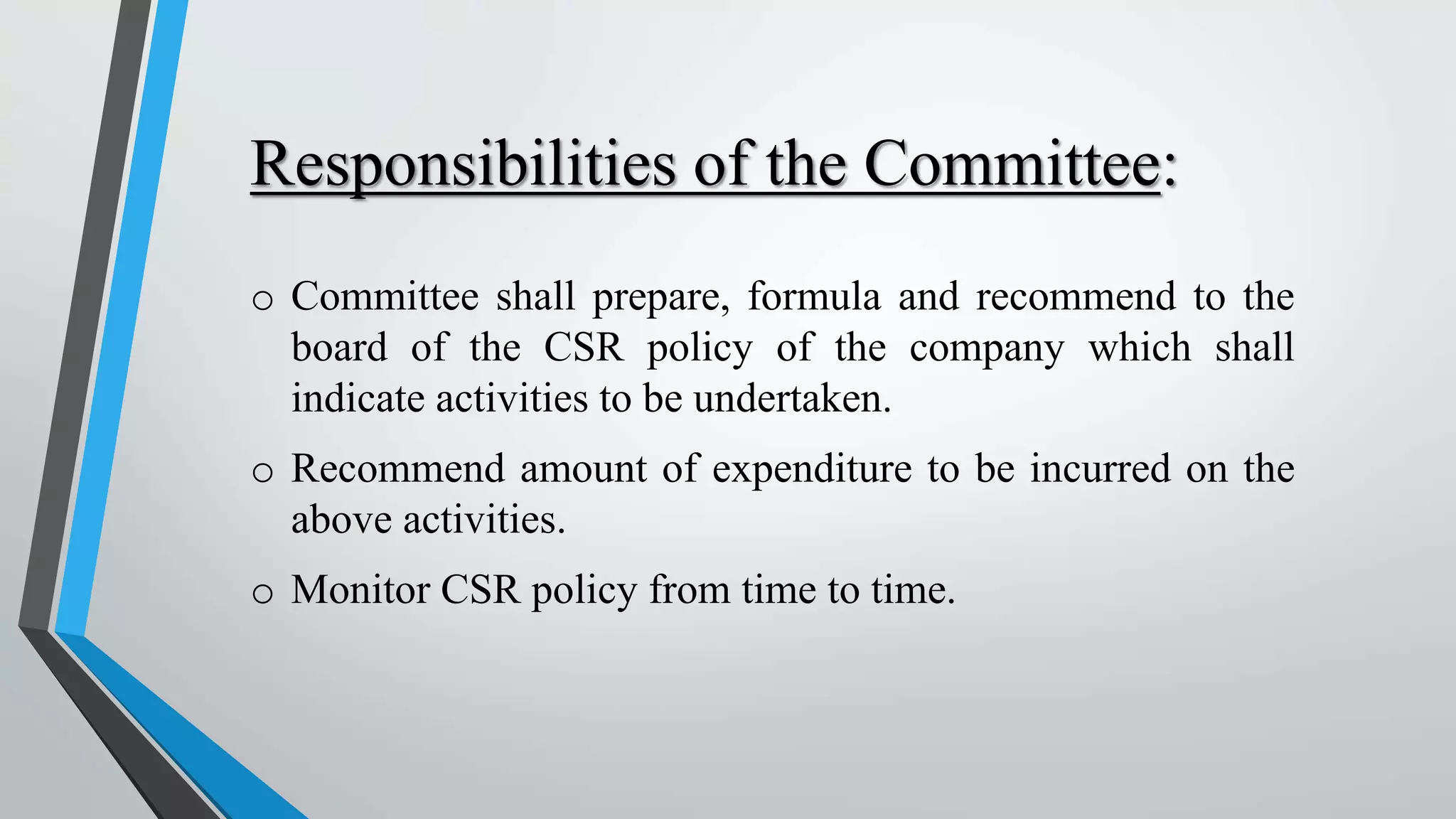

Corporate Social Responsibility (CSR) is an organizational process focused on stakeholder relationships and the common good, aiming to integrate social, environmental, and economic objectives into business operations. The Companies Act 2013 mandates certain companies to establish CSR committees, approve CSR policies, and allocate a minimum of 2% of their average net profits for CSR activities. Key CSR activities include education promotion, eradicating hunger, enhancing vocational skills, and supporting socio-economic development initiatives.