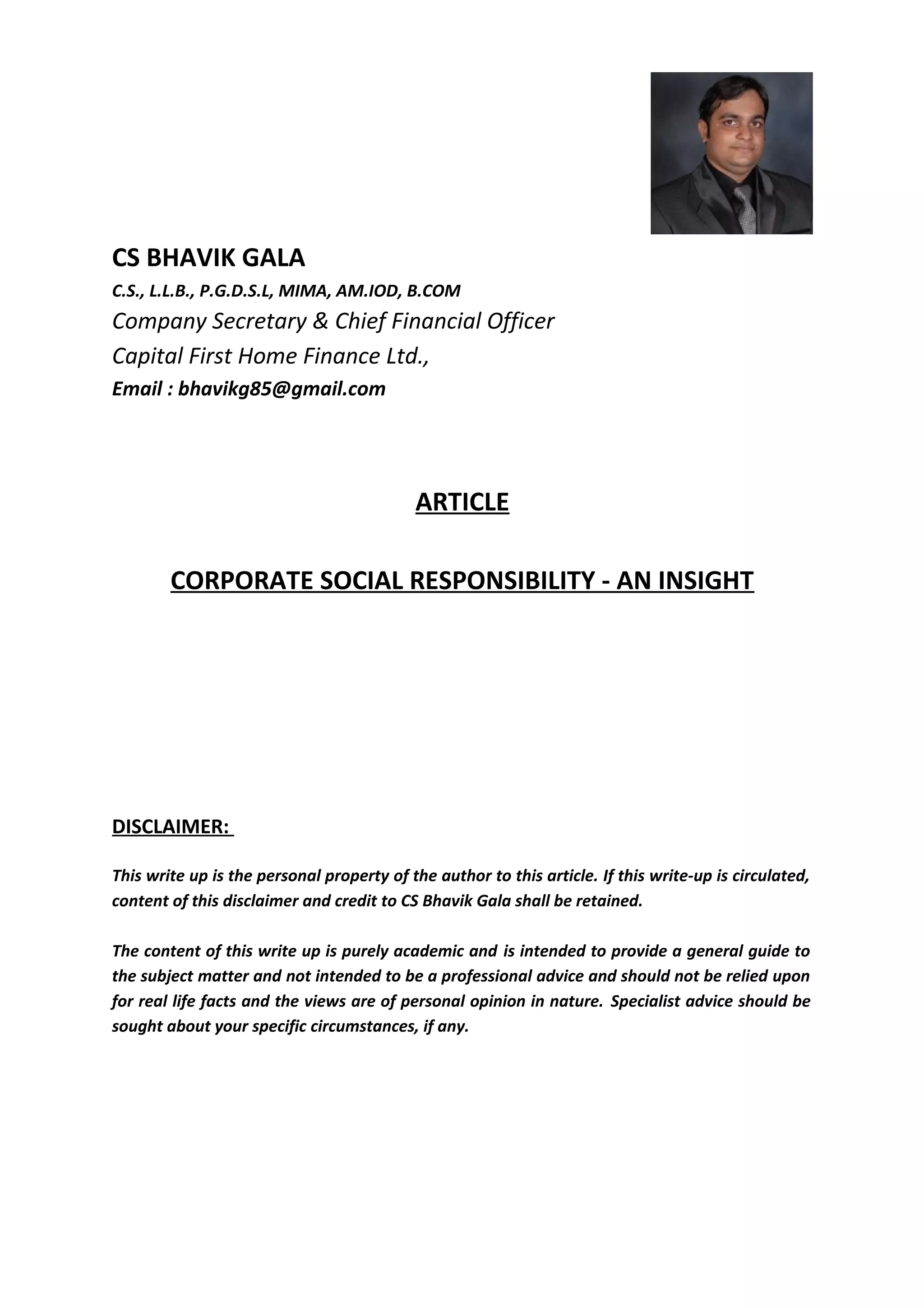

![APPLICABILITY & COMPLIANCE REQUIREMENTS

Every Company including its holding or subsidiary, and a foreign company (as defined under section

2(42) of the Act) having its branch office or project office in India, which fulfils the criteria specified

under section 135(1) of the Act shall comply with the provisions of section 135 and the Rules.

Criteria given under section 135(1) of the Act, which provides, during any financial year, a company

is either having:-

• Net worth of Rs. 500 Crores or more; or

• Turnover of Rs. 1,000 Crores or more; or

• Net profit of Rs. 5 Crores or more.

Every company which falls under the criteria mentioned under section 135(1) shall:-

• Constitute a Corporate Social Responsibility Committee of the Board (CSR Committee);

• Formulate Corporate Social Responsibility Policy (CSR Policy);

• Spend, in every financial year, at least two percent of the ‘Average Net Profits’ of the

company made during the three immediately preceding financial years, in pursuance of its

CSR Policy;

• Include in Board’s Report (pertaining to financial year commencing on or after 1st

April 2014)

an Annual Report on CSR, containing particulars specified under the Rules (In case of foreign

company, the balance sheet shall contain an annexure regarding report on CSR) .

• Display the contents of CSR Policy in Board’s Report and also place on company’s website, if

any.

The company shall give preference to the local area and areas around which it operates, for

spending the amount earmarked for the CSR Activities.

CSR Committee of Board shall consist of three or more directors, out of which at least one director

shall be an independent director. However, there are following exemptions:

• An unlisted company or private company [not required to appoint an independent director

pursuant to section 149(4)] shall have CSR Committee without such director.

• A private company having only two directors shall constitute CSR Committee with two such

directors.

• CSR Committee of a foreign company shall comprise of at least two persons of which one

shall be a person authorised to accept any notice or other documents from Registrar and

another person nominated by the foreign company.](https://image.slidesharecdn.com/article-corporatesocialresponsibility-aninsight-160807130238/85/Article-on-Corporate-Social-Responsibility-an-insight-3-320.jpg)

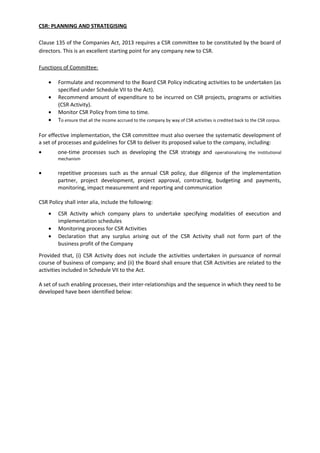

![institutions which are approved by the Central Government;

10. rural development projects.

The companies may pursue CSR Activity by taking into account the following:

a) the activities undertaken in pursuance of normal course of business shall not be treated as

CSR Activity.

b) the company may undertake CSR Activities through a registered trust or society or company,

established by the company or its holding or subsidiary or associate company. Provided that,

if trust, society or company is not established by company or its holding or subsidiary or

associate company, it shall have an established track record of three years in undertaking

similar programs or projects.

c) the company shall specify project or programs to be undertaken through said entities and

also the modalities of utilization of funds and have system of monitoring and reporting the

same.

d) collaborate with other companies for undertaking CSR Activities in such manner that the CSR

Committee of respective companies can report separately on CSR Activities.

e) the programs or activities undertaken in India only shall amount to CSR expenditure.

f) the projects, programs or activities that benefit only the employees of the company and

their families shall not be considered CSR Activity.

g) contribution of any amount directly or indirectly to any political party shall not be

considered as CSR Activity.

h) companies may build CSR capacities of their own personnel as well as those of their

implementing agencies through Institutions with established track records of at least three

financial years but such expenditure shall not exceed five percent of total CSR expenditure in

one financial year.

i) In case of foreign owned and controlled companies, CSR contribution can be made only to

those trust/NGO’s, etc. who hold FCRA license. It also pertinent to note that such restriction

has been proposed to be removed retrospectively in the Union Budget of 2016 but we need

to wait and watch till the same is being effectively notified and comply with the currently

effective provisions.

CERTAIN CLARIFICATIONS ON REGULATORY FRAMEWORK OF CSR

1. It is further clarified that CSR activities should be undertaken by the companies in project/

programme mode [as referred in Rule 4 (1) of Companies CSR Rules, 2014]. One-off events

such as marathons/ awards/ charitable contribution/ advertisement/ sponsorships of TV

programmes etc. would not be qualified as part of CSR expenditure.

2. Expenses incurred by companies for the fulfilment of any Act/ Statute of regulations (such as

Labour Laws, Land Acquisition Act etc.) would not count as CSR expenditure under the

Companies Act.](https://image.slidesharecdn.com/article-corporatesocialresponsibility-aninsight-160807130238/85/Article-on-Corporate-Social-Responsibility-an-insight-6-320.jpg)

This document provides an overview of Corporate Social Responsibility (CSR) in India. It discusses how CSR has evolved from traditional philanthropic activities to become more strategic and linked to business. The Companies Act of 2013 introduced mandatory CSR requirements for large companies in India. It outlines the activities considered eligible for CSR spending under Schedule VII of the Act, such as education, healthcare, environment, and more. The document also discusses the applicability of CSR requirements to companies, constitution of CSR committees, development of CSR policies and programs, and relevant tax benefits.