Downloaded 21 times

![228822

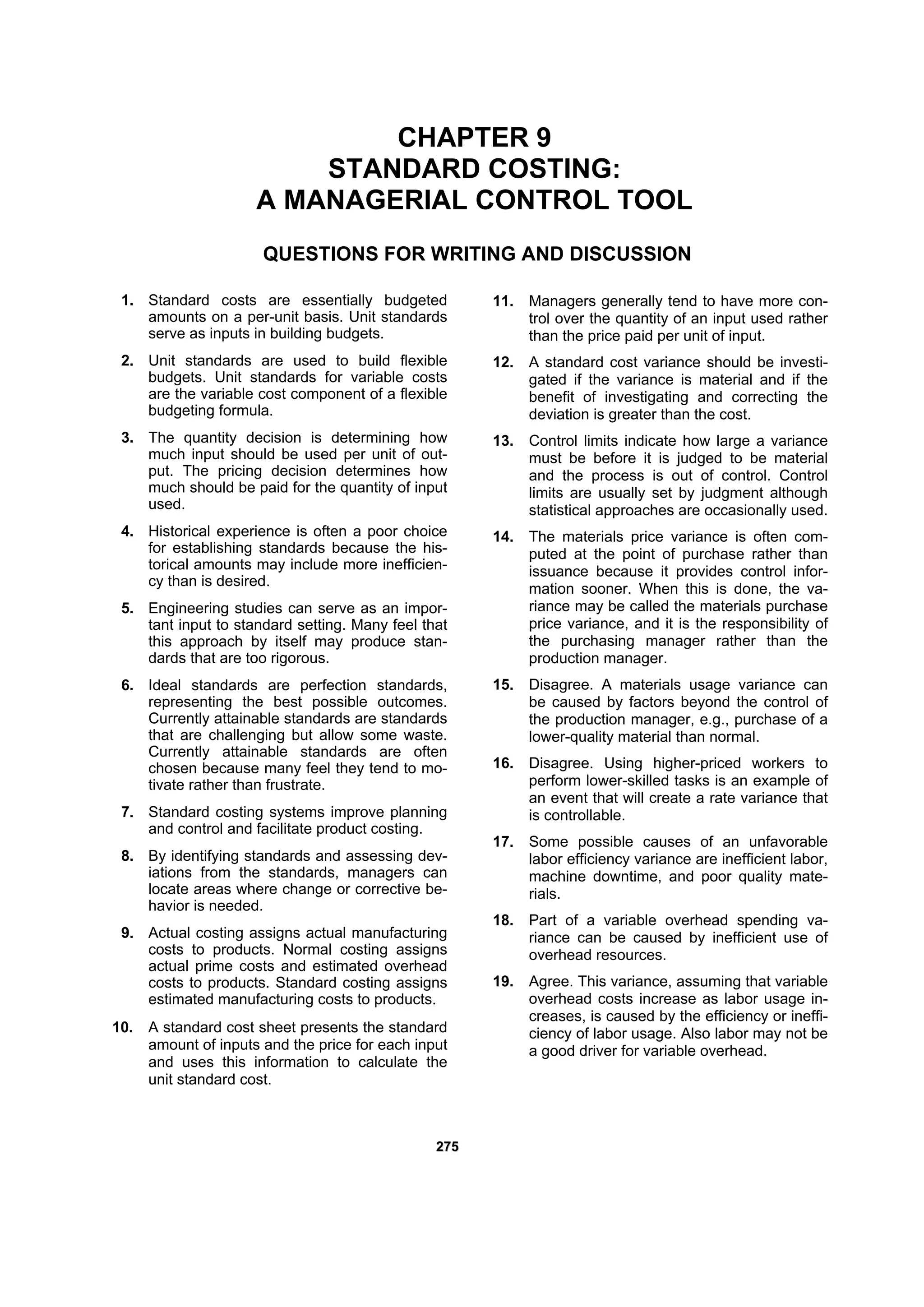

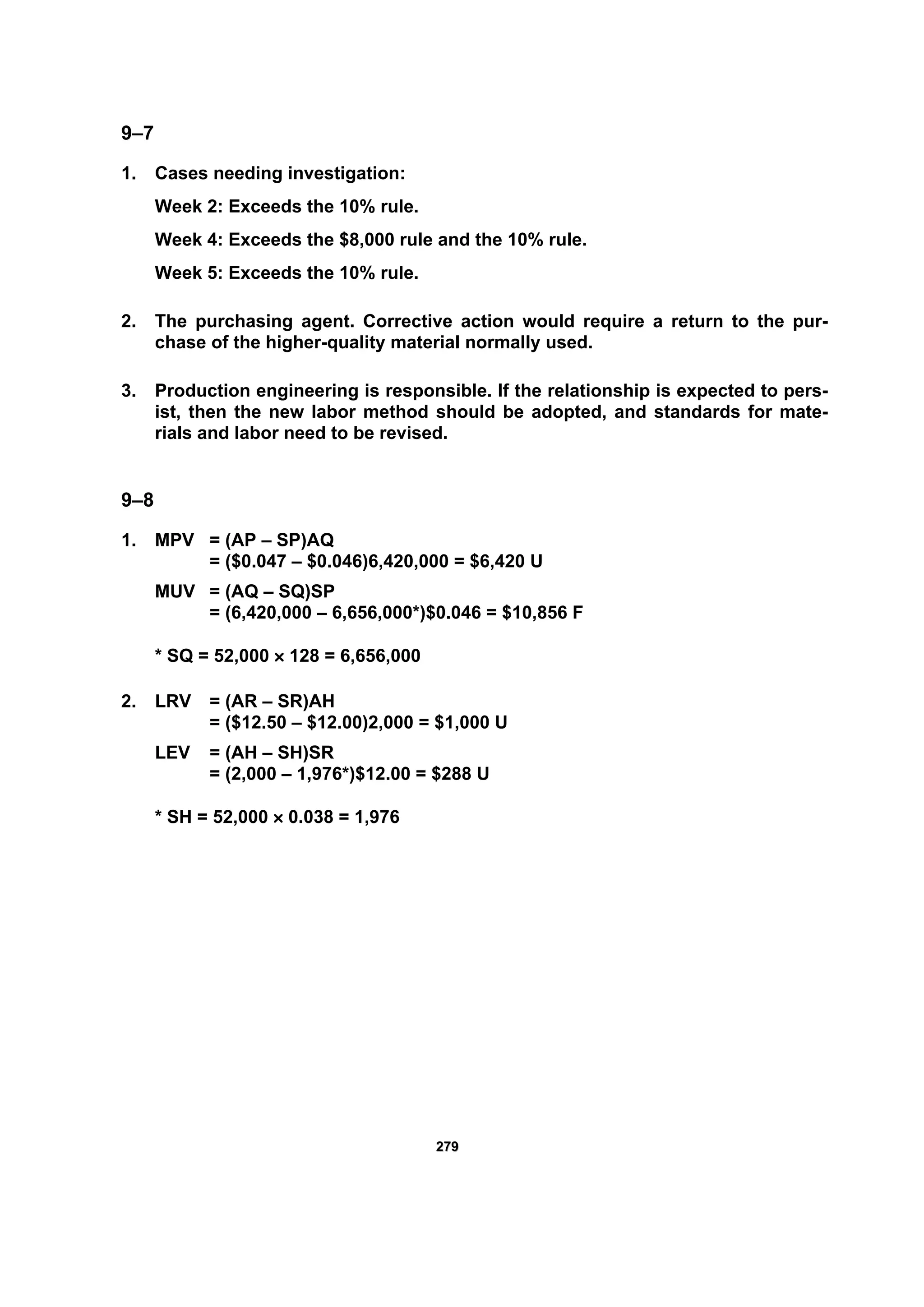

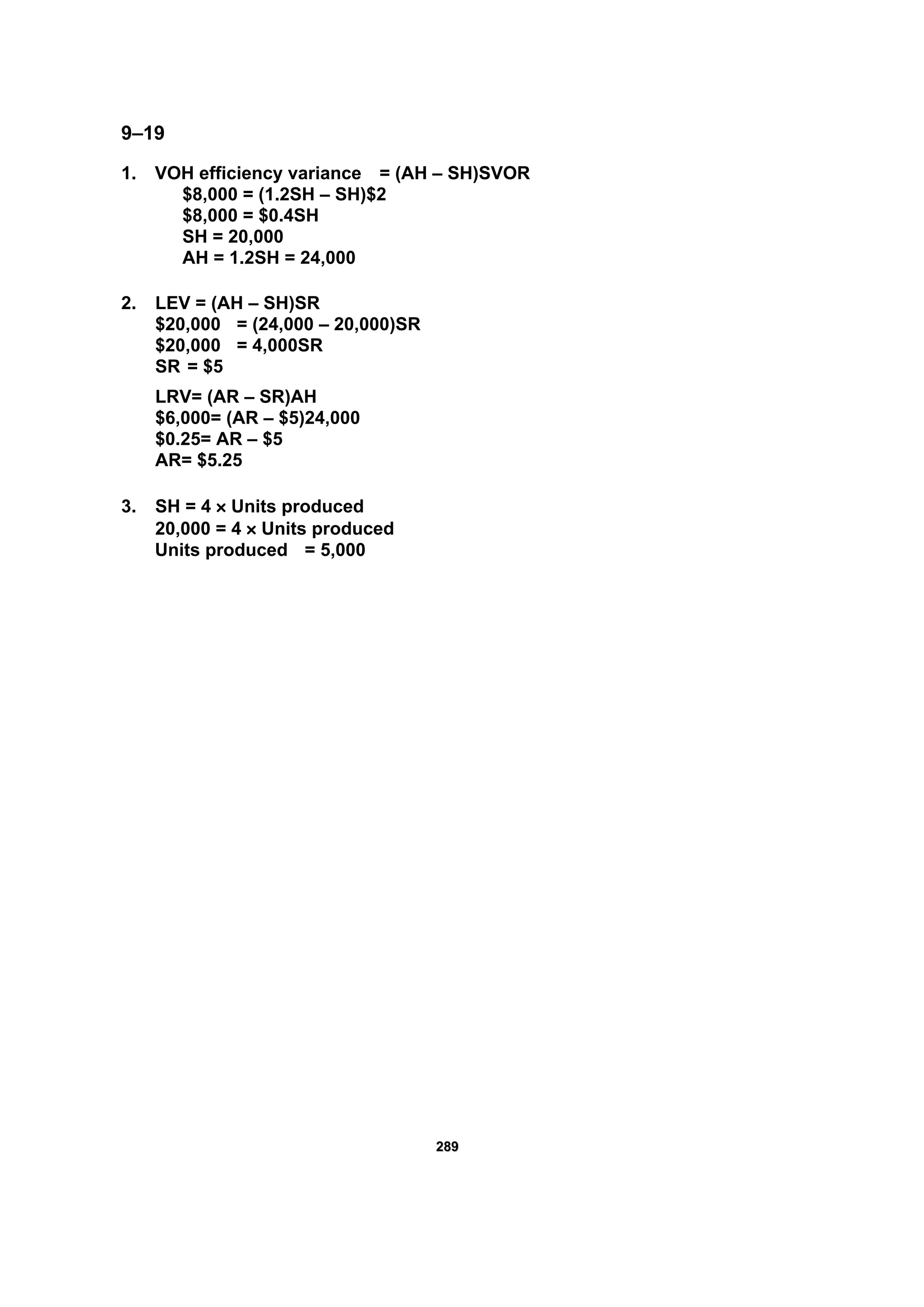

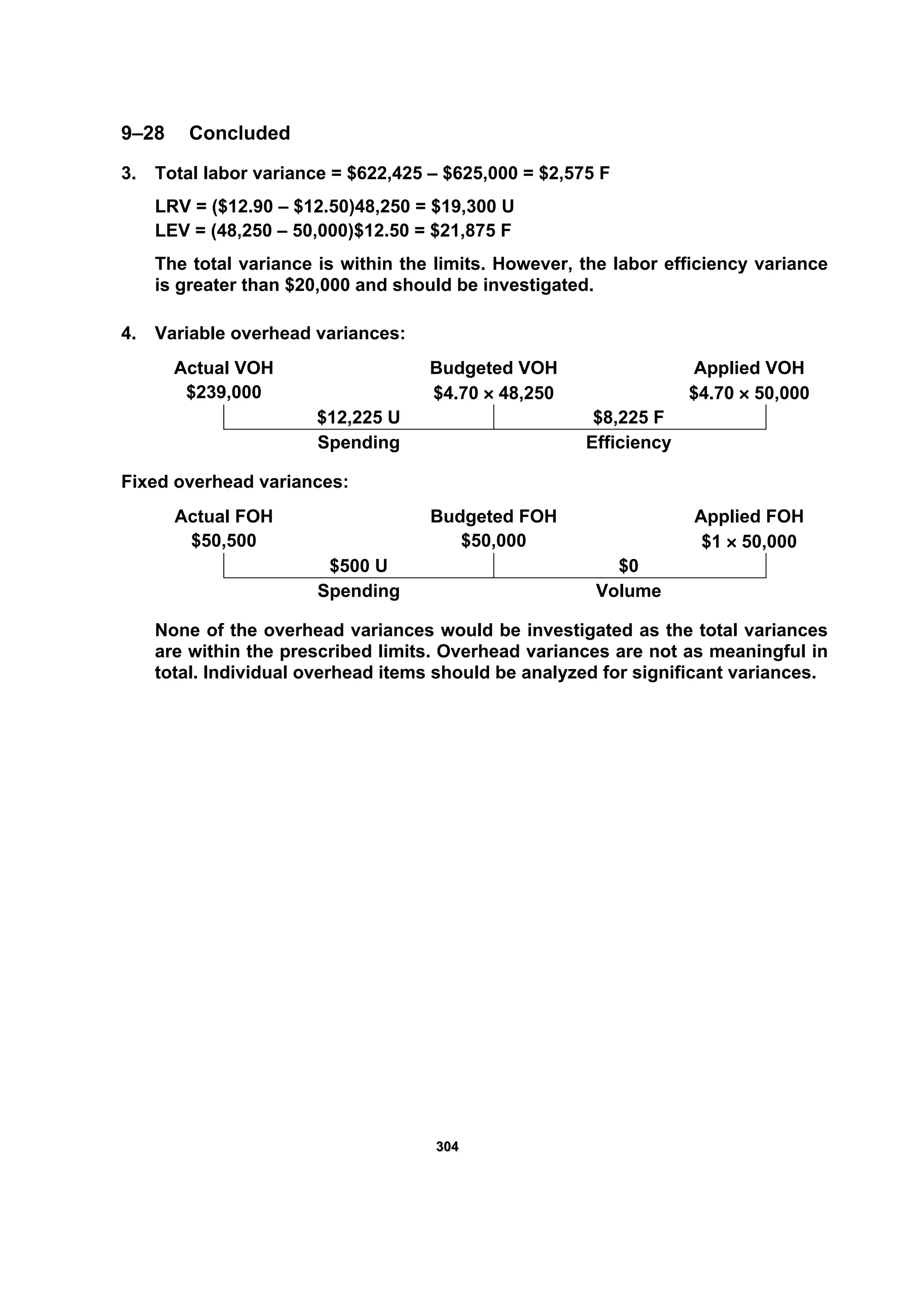

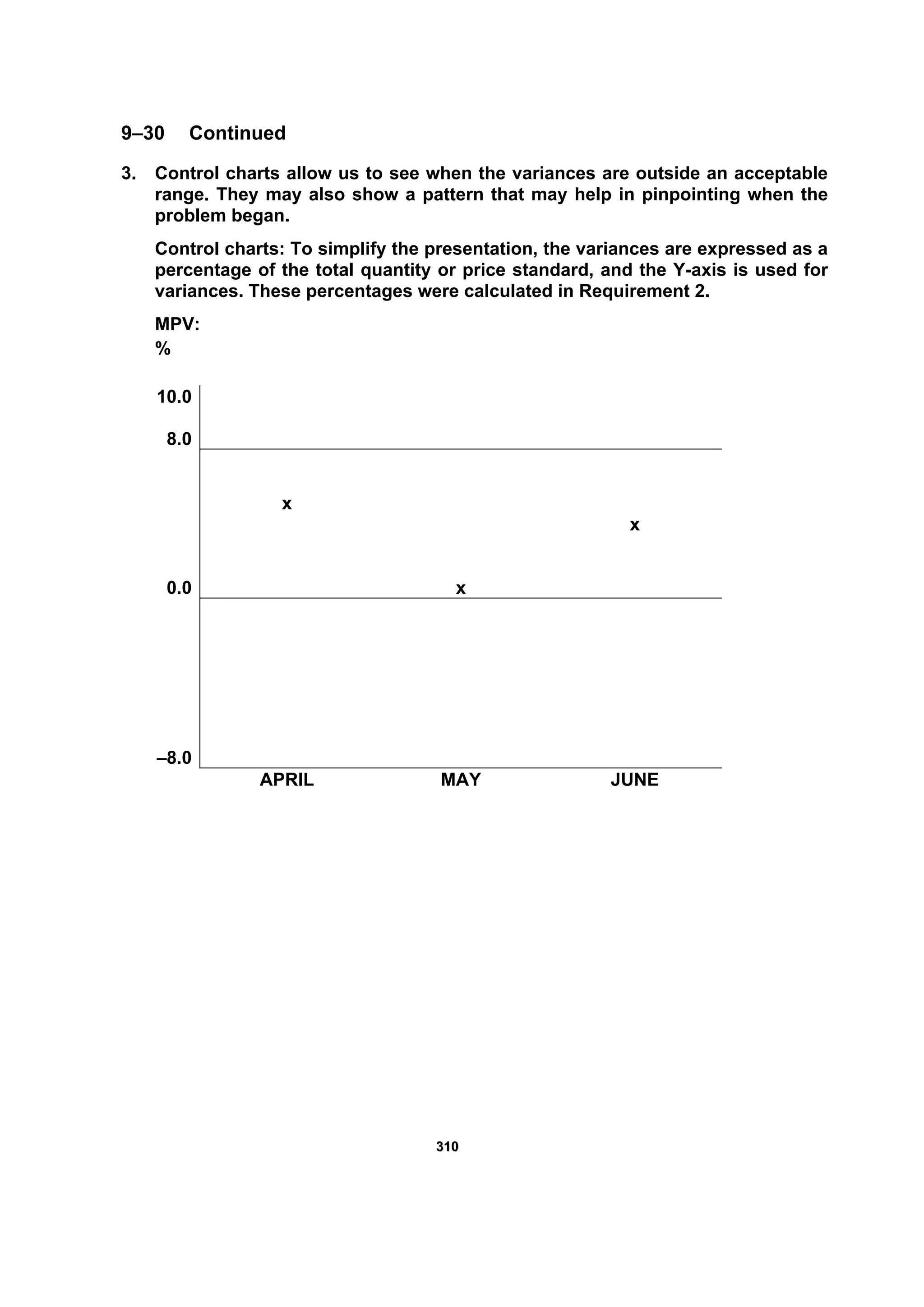

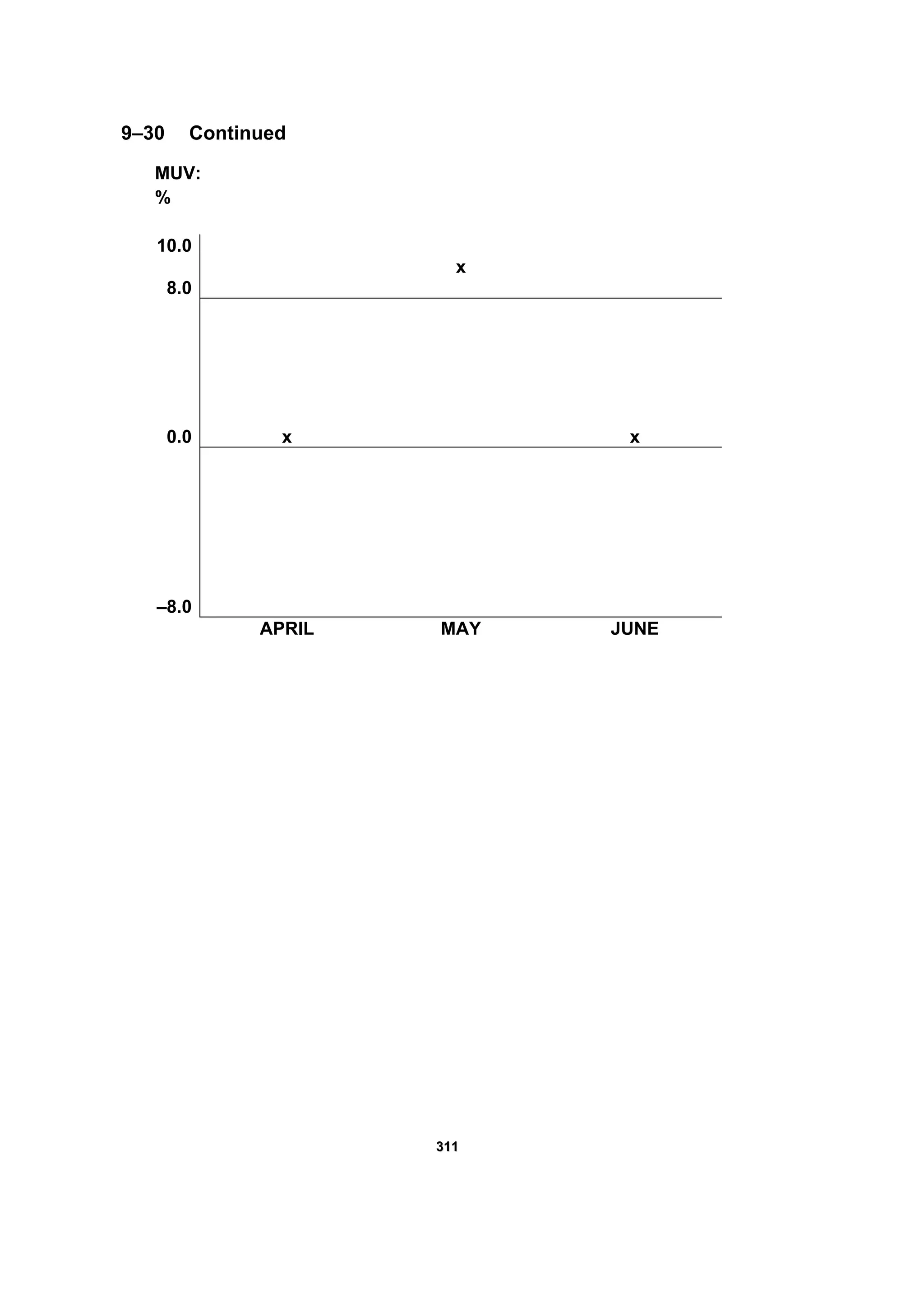

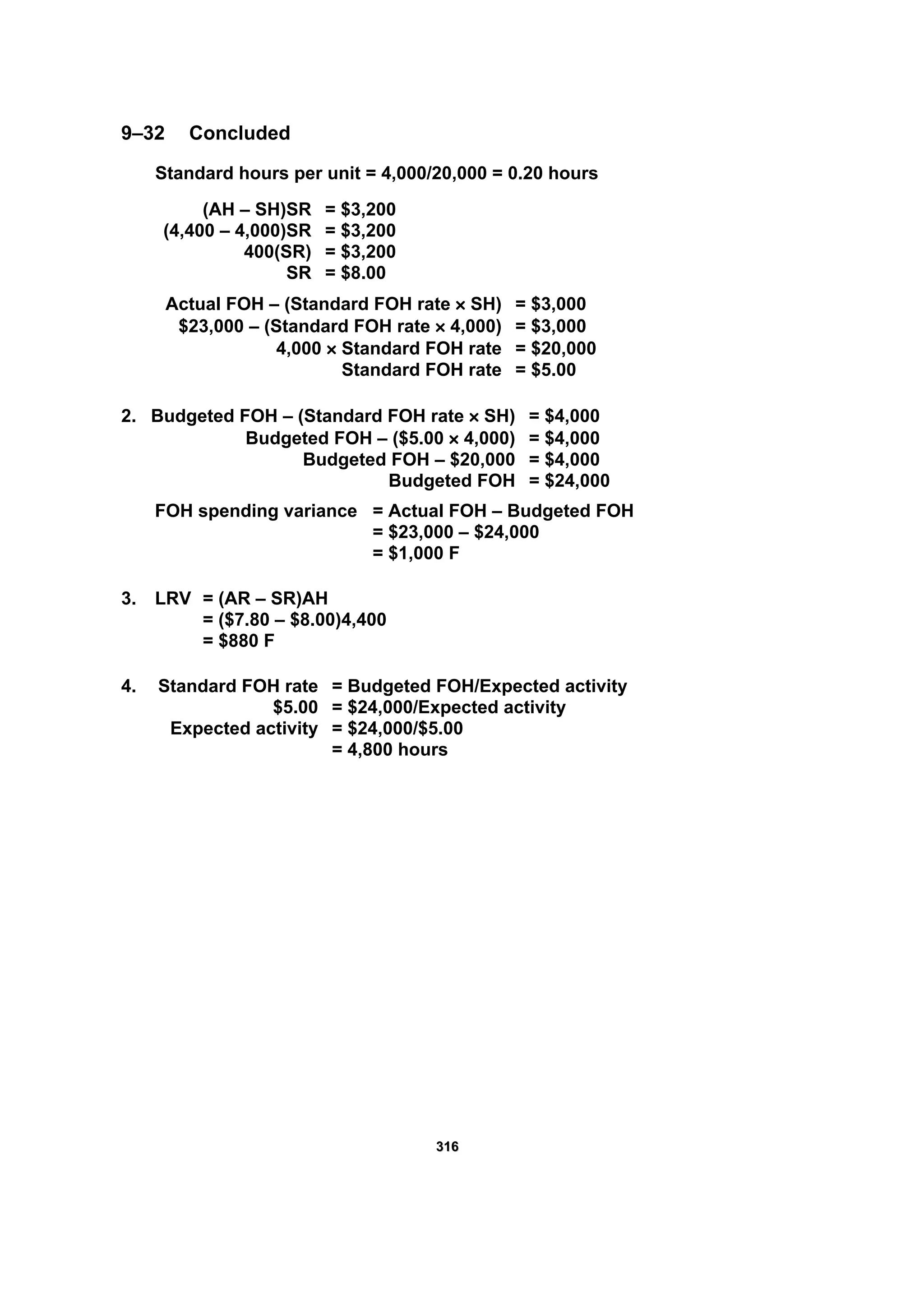

9–11

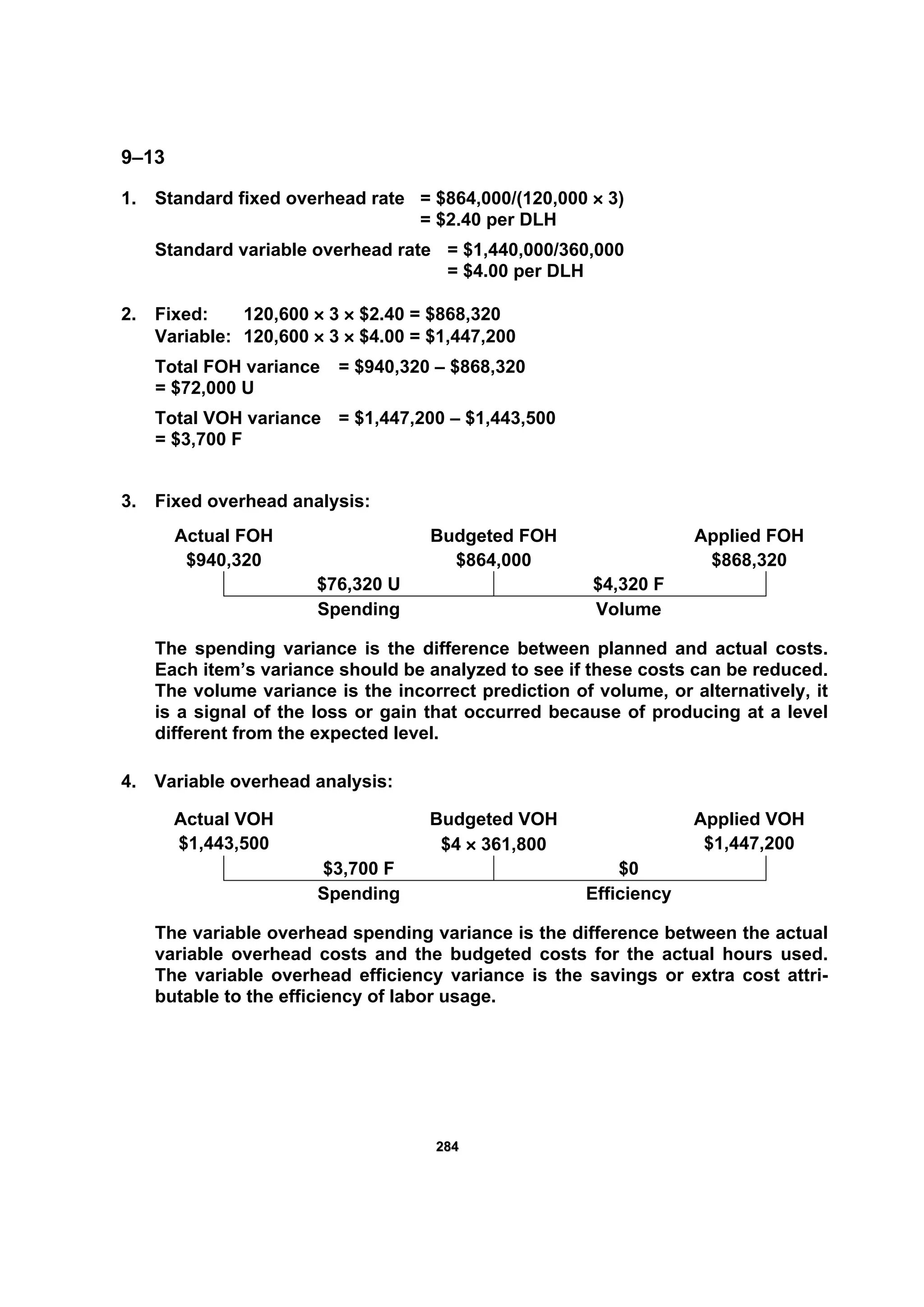

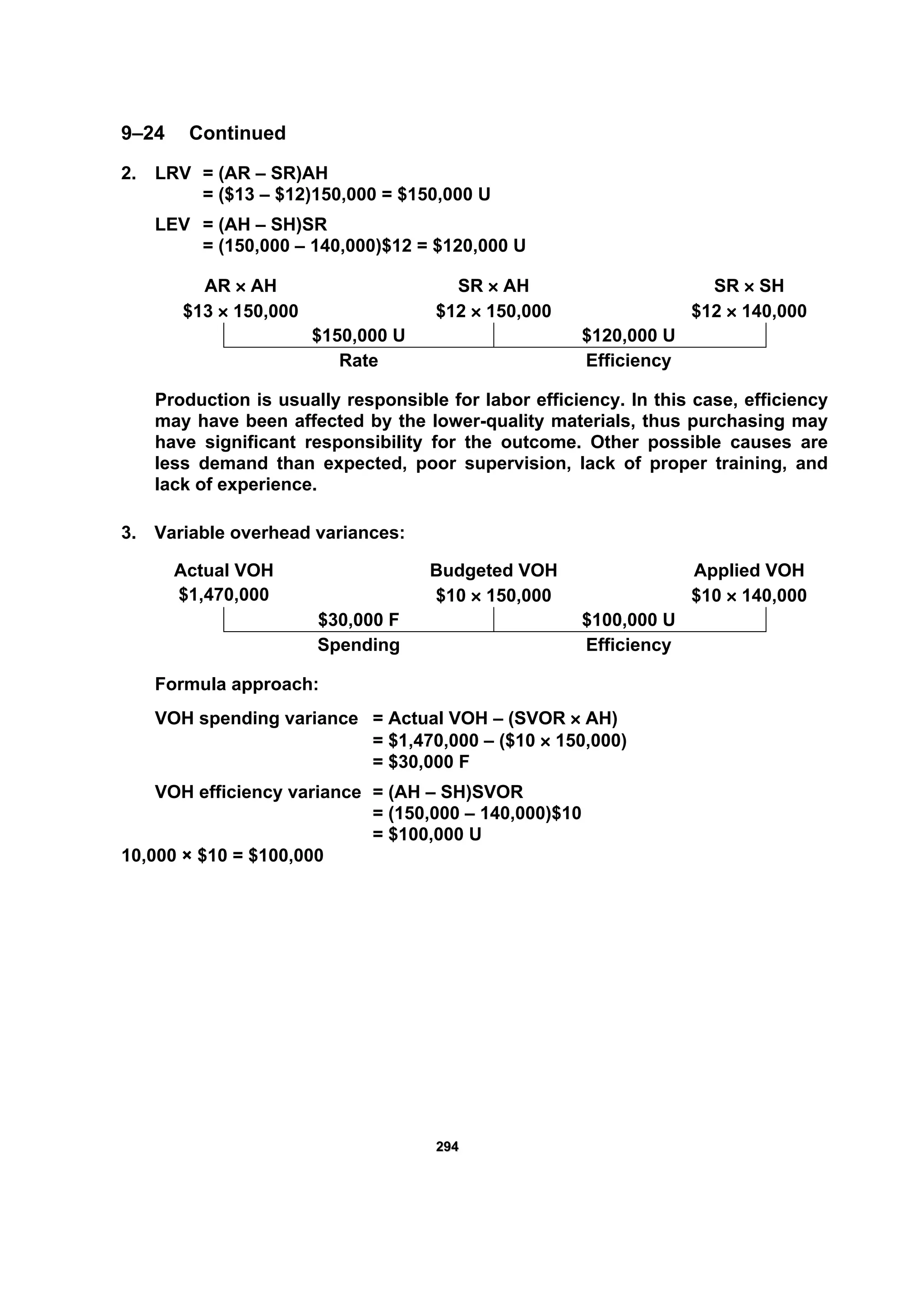

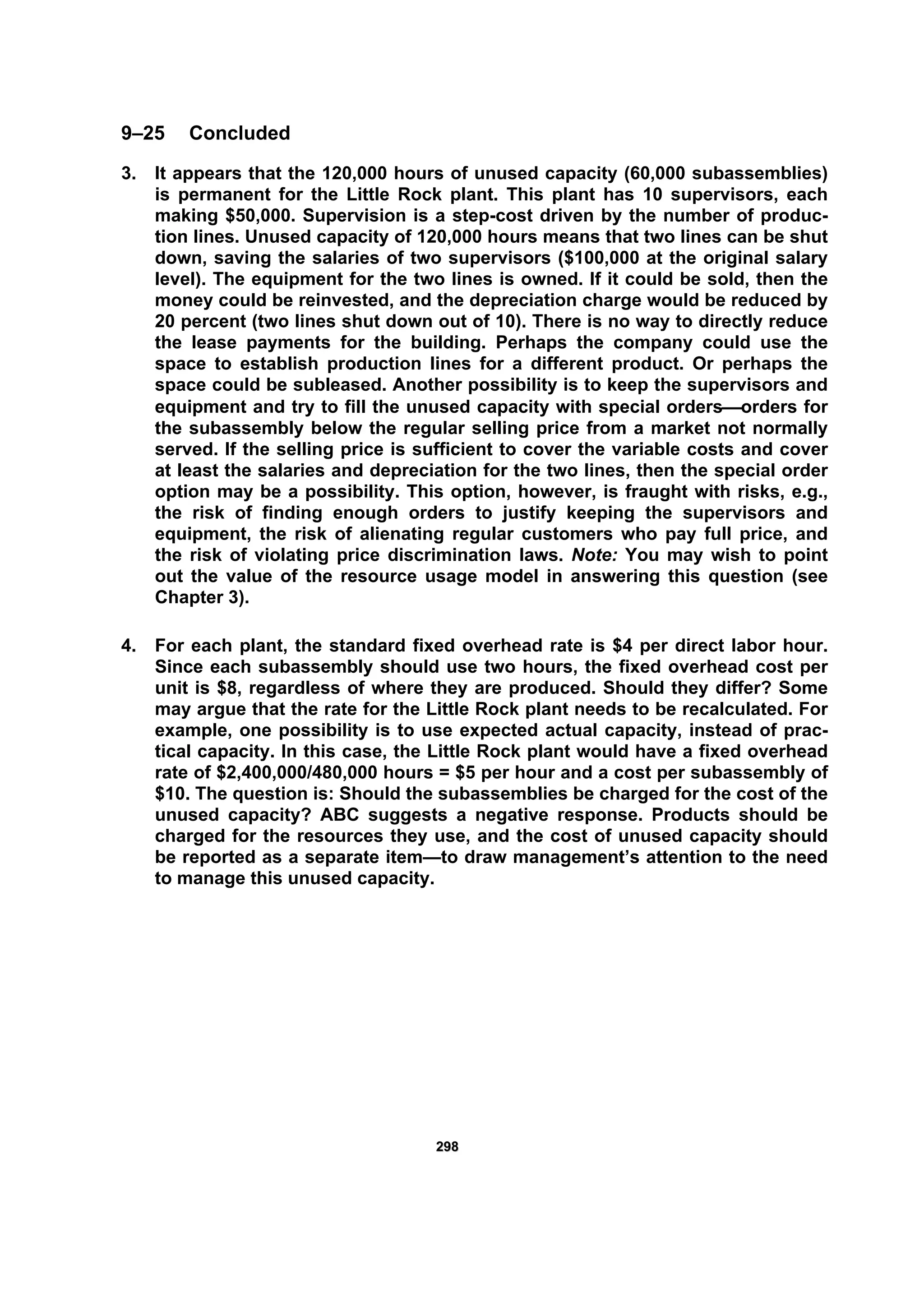

1. MPV = (AP – SP)AQ

= ($8.05 – $7.95)222,500 = $22,250 U

MUV = (AQ – SQ)SP

= [220,400 – (20,100 × 11)]$7.95 = $5,565 F

(A three-pronged variance diagram is not shown because MPV is for materials

purchased and not materials used.)

2. LRV = (AR – SR)AH

= ($9.50 – $9.40)79,900 = $7,990 U

Note: AR = $759,050/79,900 = $9.50

LEV = (AH – SH)SR

= [79,900 – (20,100 × 4)]$9.40 = $4,700 F

AR × AH SR × AH SR × SH

$9.50 × 79,900 $9.40 × 79,900 $9.40 × 80,400

$7,990 U $4,700 F

Rate Efficiency

3. Materials Inventorya

.................................. 1,768,875

MPV ............................................................ 22,250

Accounts Payableb

.............................. 1,791,125

Work in Processc

....................................... 1,757,745

MUV....................................................... 5,565

Materials Inventoryd

............................ 1,752,180

Work in Processe

....................................... 755,760

LRV ............................................................. 7,990

LEV........................................................ 4,700

Accrued Payrollf

.................................. 759,050

a

$7.95 × 222,500 =1,768,875

b

$8.05 × 222,500 =1,791,125

c

$7.95 × 221,100 =1,757,745

d

$7.95 × 222,500 = 1,768,875

e

$9.40 × 80,400 = 755,760

f

$9.50 × 79,900 = 759,050](https://image.slidesharecdn.com/ch9-171016134546/75/Chapter-9-Standard-Costing-A-Managerial-Control-Tool-8-2048.jpg)

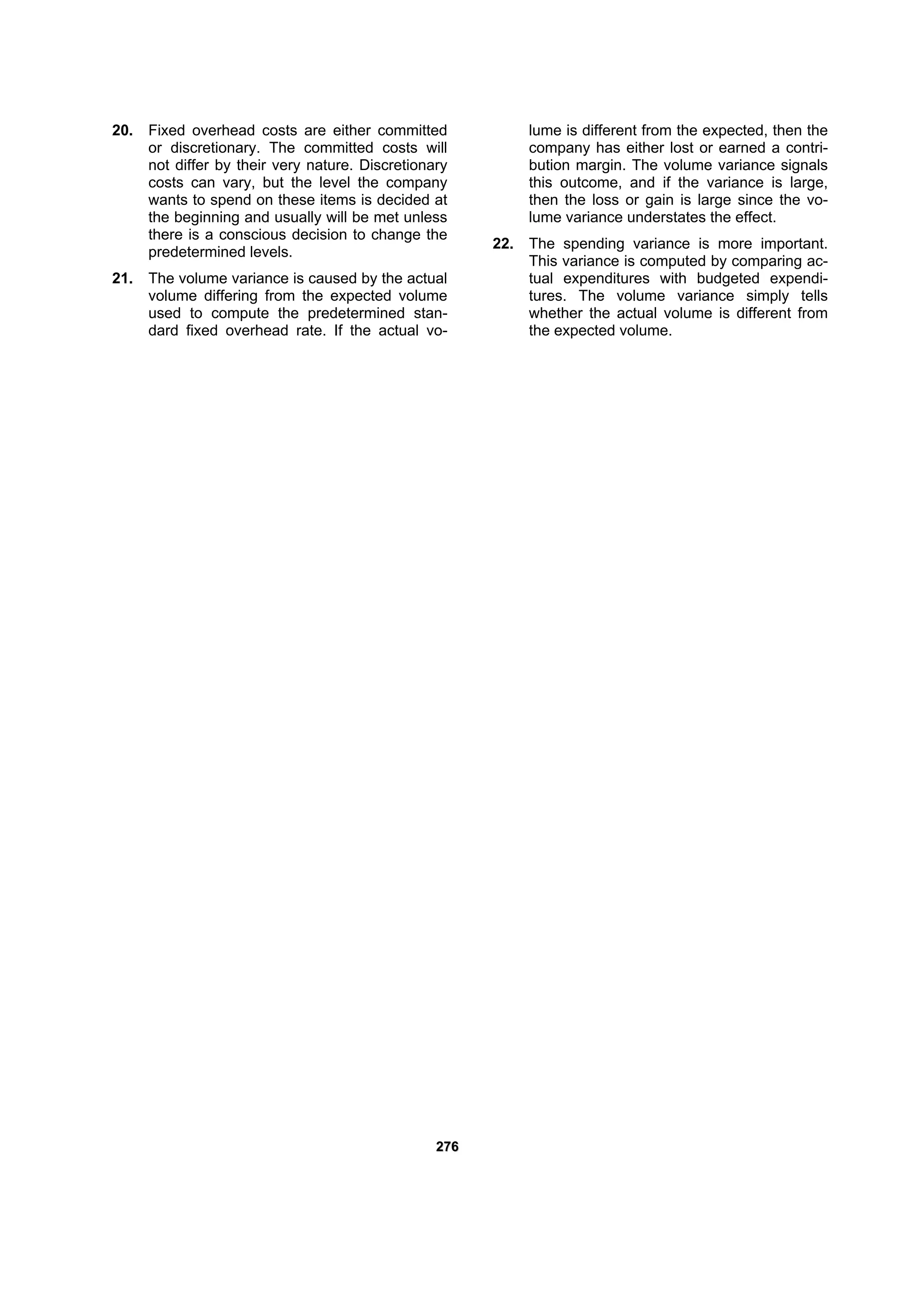

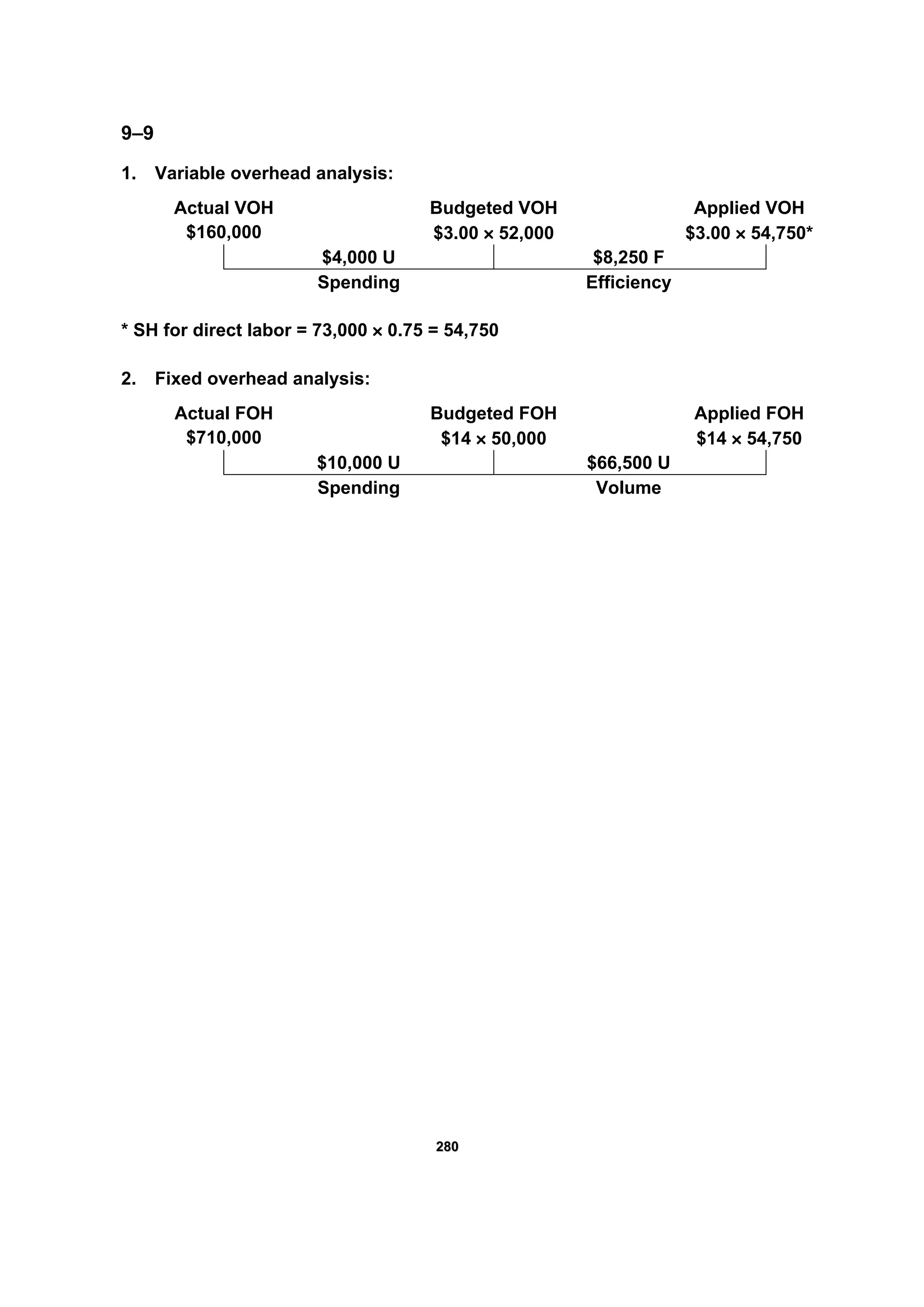

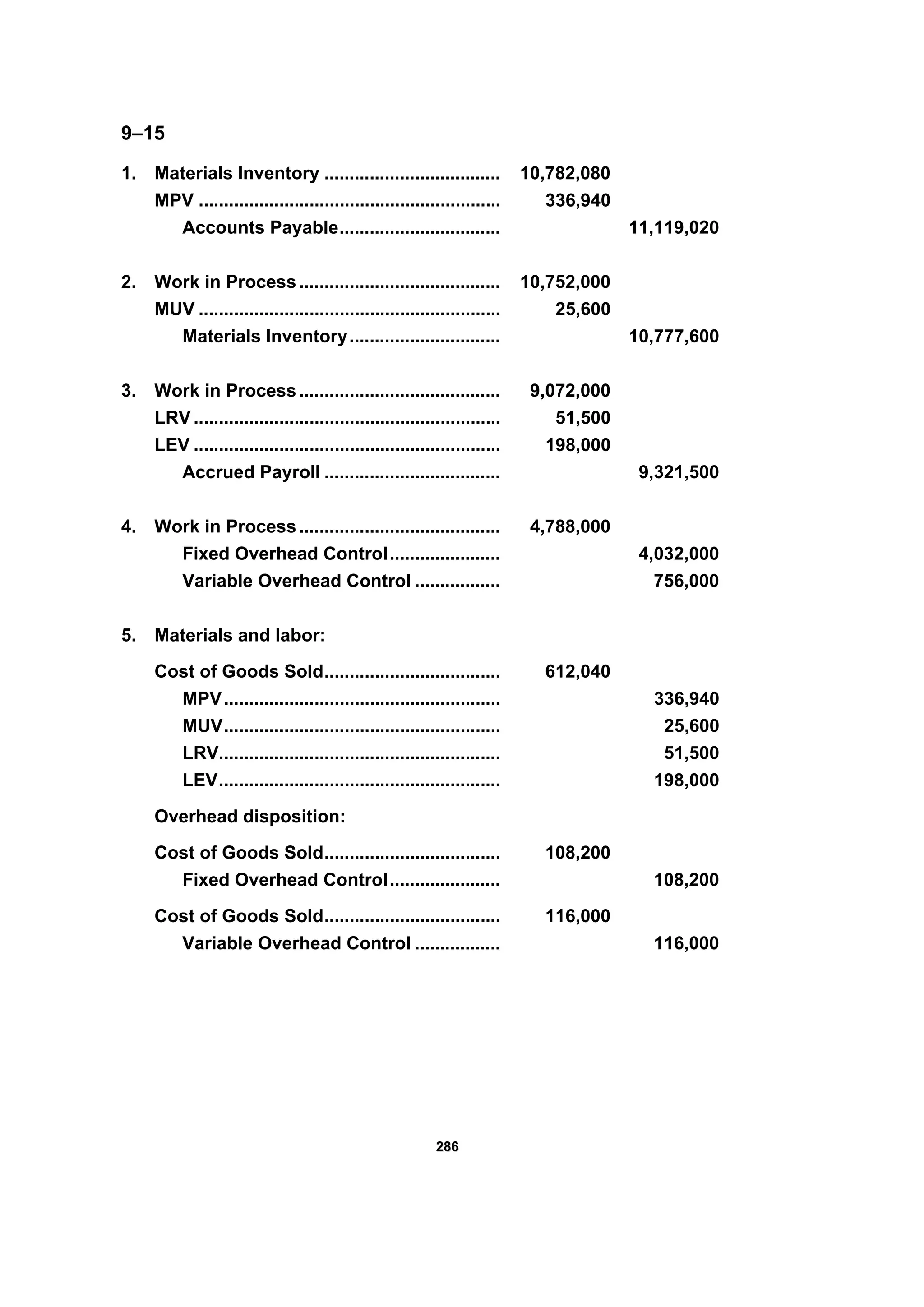

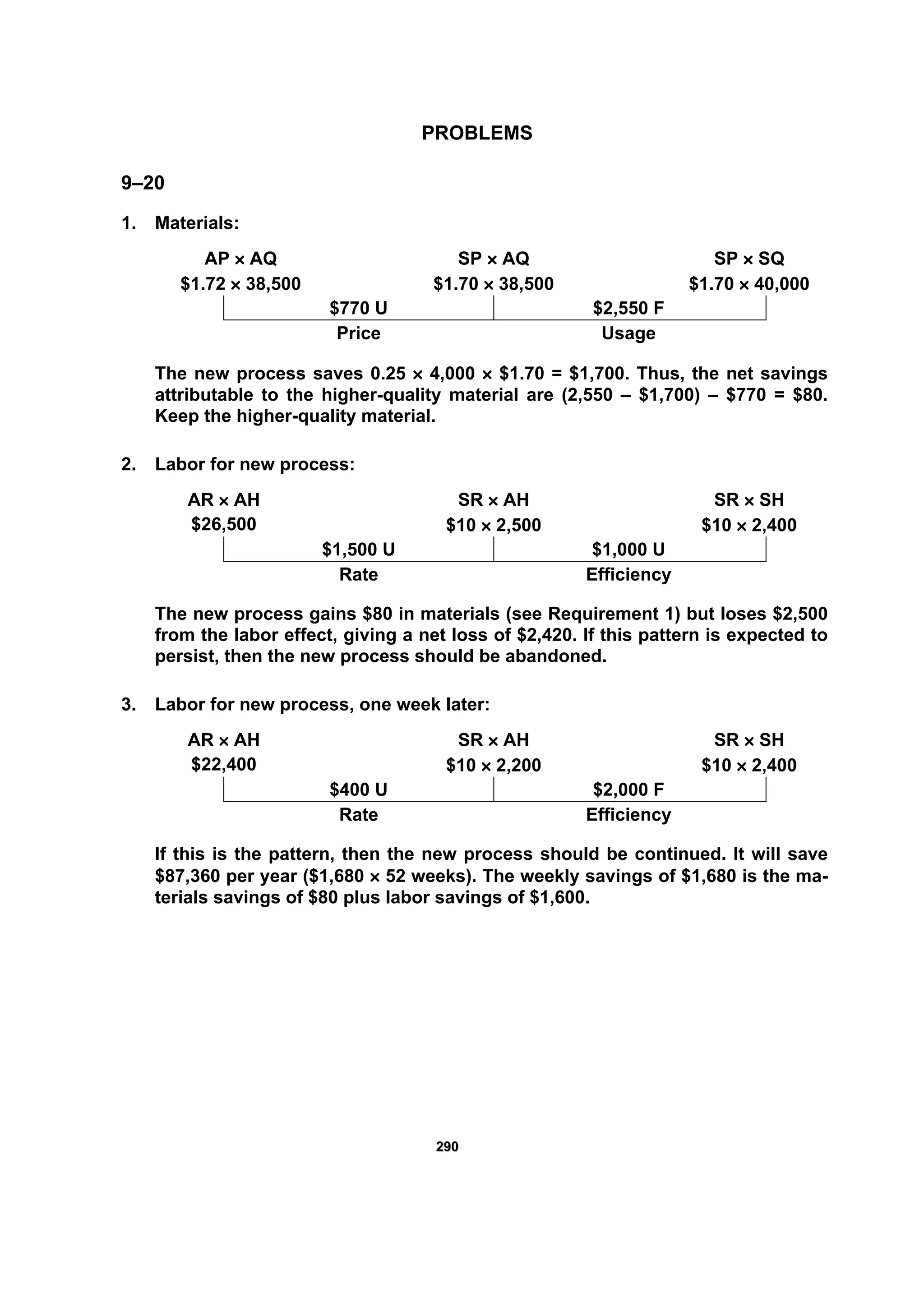

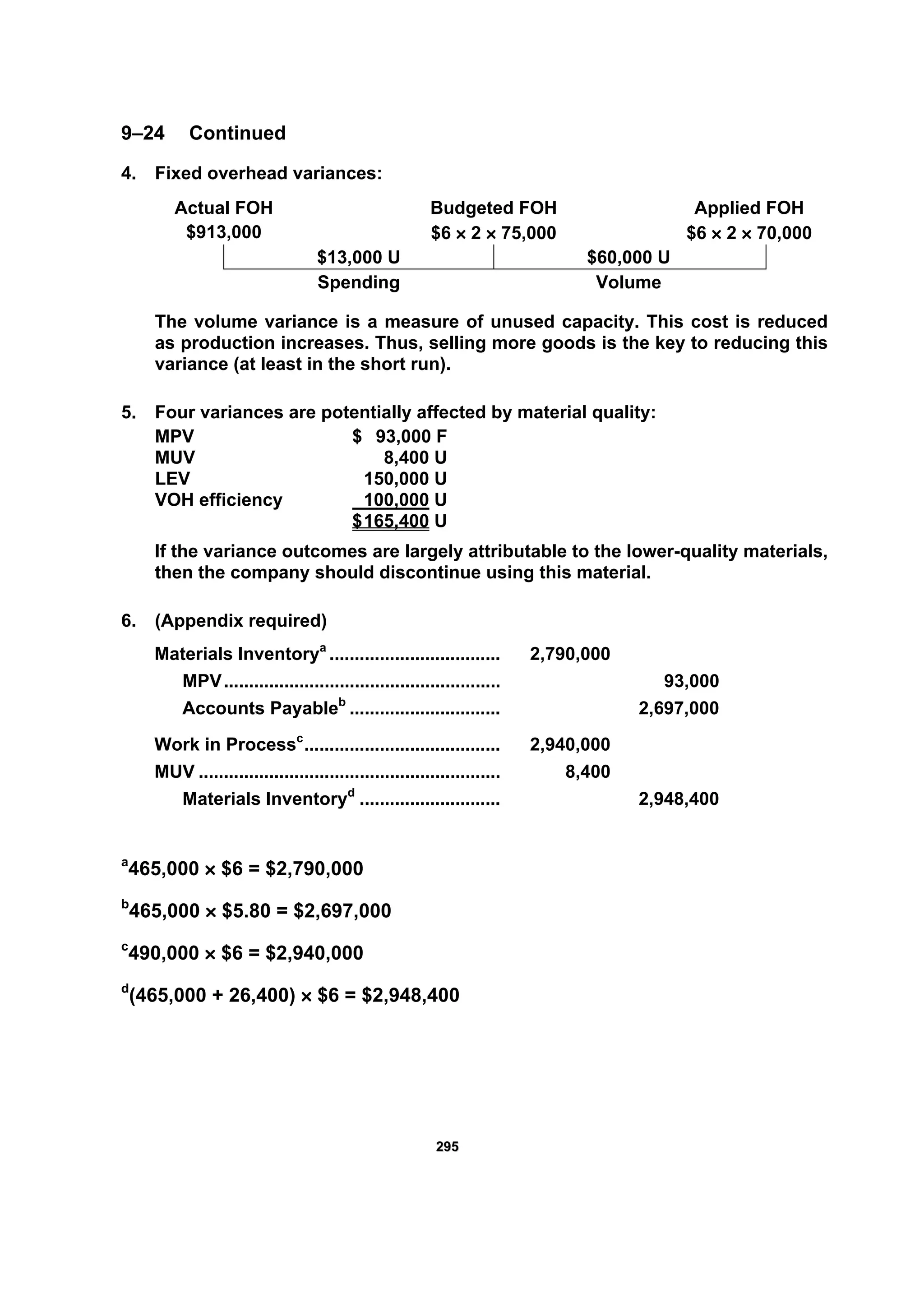

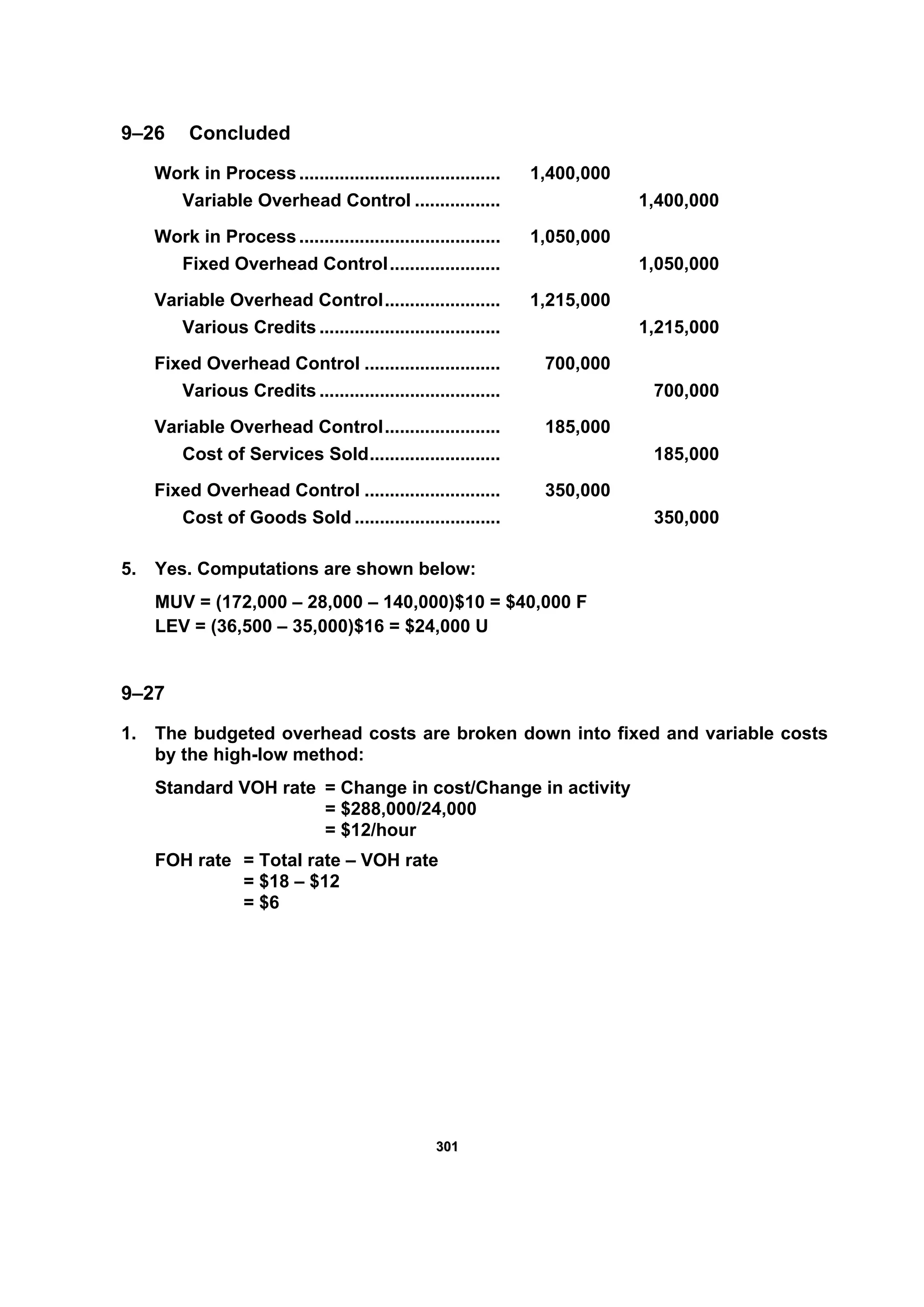

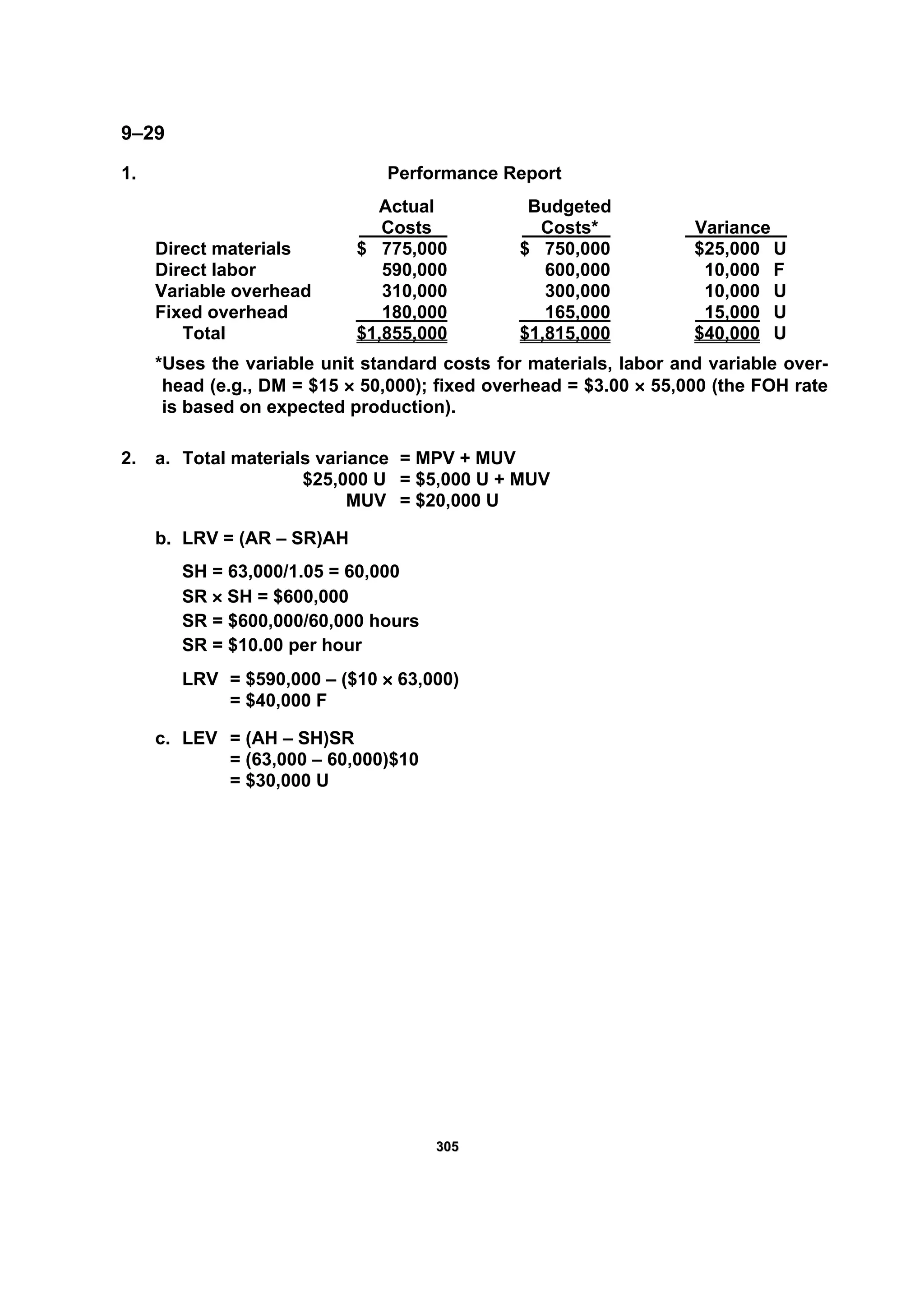

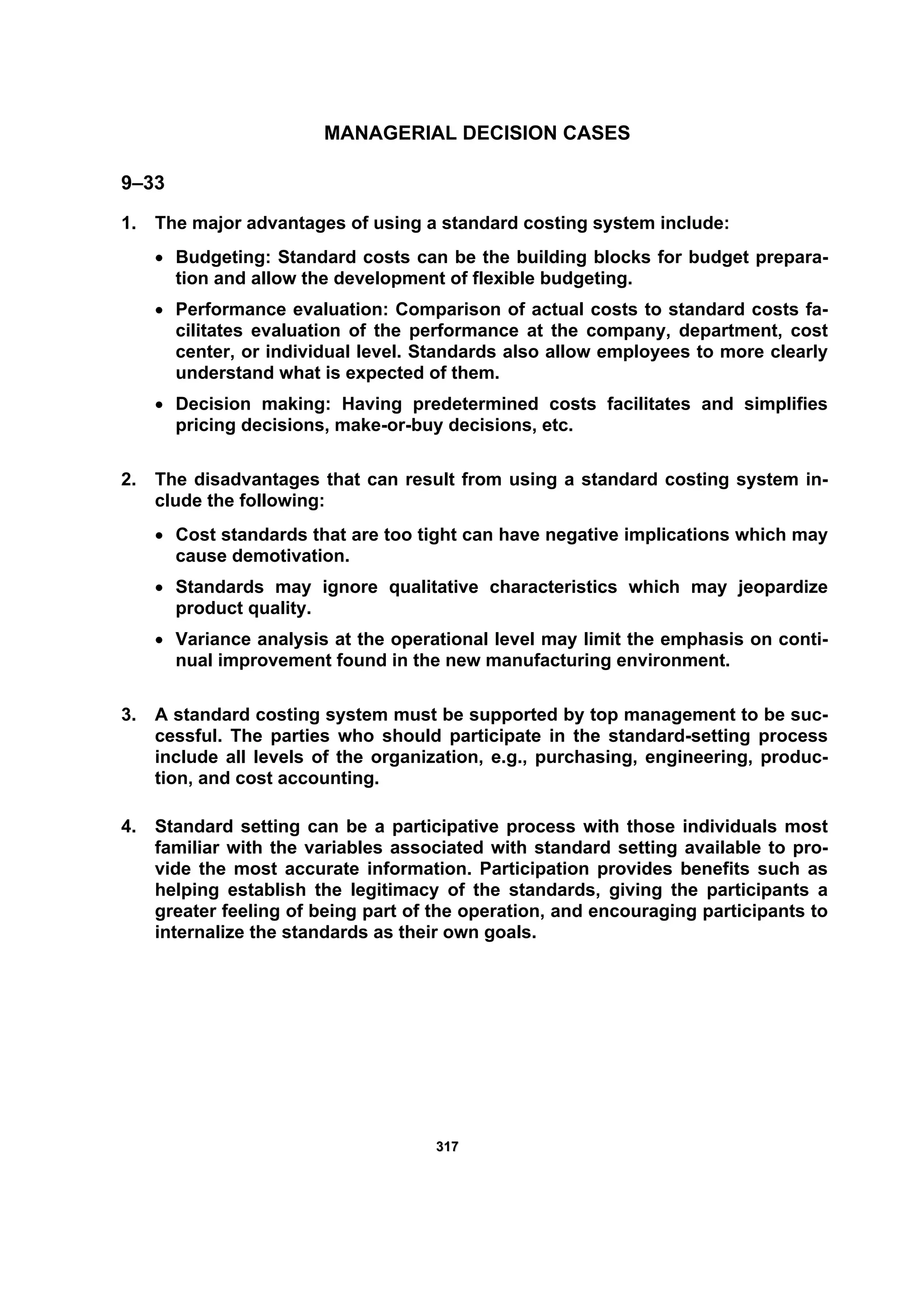

![228855

9–14

1. MPV = (AP – SP)AQ

= ($6.60 – $6.40)1,684,700

= $336,940 U

MUV = (AQ – SQ)SP

= (1,684,000 – 1,680,000)$6.40

= $25,600 U

Note: There is no three-pronged analysis for materials because materials pur-

chased is different from the materials used. (MPV uses materials purchased

and MUV uses materials used.)

2. LRV = (AR – SR)AH

= ($18.10 – $18.00)515,000

= $51,500 U

LEV = (AH – SH)SR

= [515,000 – (1.8 × 280,000 units)]$18.00

= $198,000 U

AR × AH SR × AH SR × SH

$18.10 × 515,000 $18 × 515,000 $18 × 504,000

$51,500 U $198,000 U

Rate Efficiency

3. Fixed overhead analysis:

Actual FOH Budgeted FOH Applied FOH

$4,140,200 $8 × 518,400 $8 × 504,000

$7,000 F $115,200 U

Spending Volume

Note: Practical volume in hours = 1.8 × 288,000 = 518,400 hours

4. Variable overhead analysis:

Actual VOH Budgeted VOH Applied VOH

$872,000 $1.50 × 515,000 $1.50 × 504,000

$99,500 U $16,500 U

Spending Efficiency](https://image.slidesharecdn.com/ch9-171016134546/75/Chapter-9-Standard-Costing-A-Managerial-Control-Tool-11-2048.jpg)

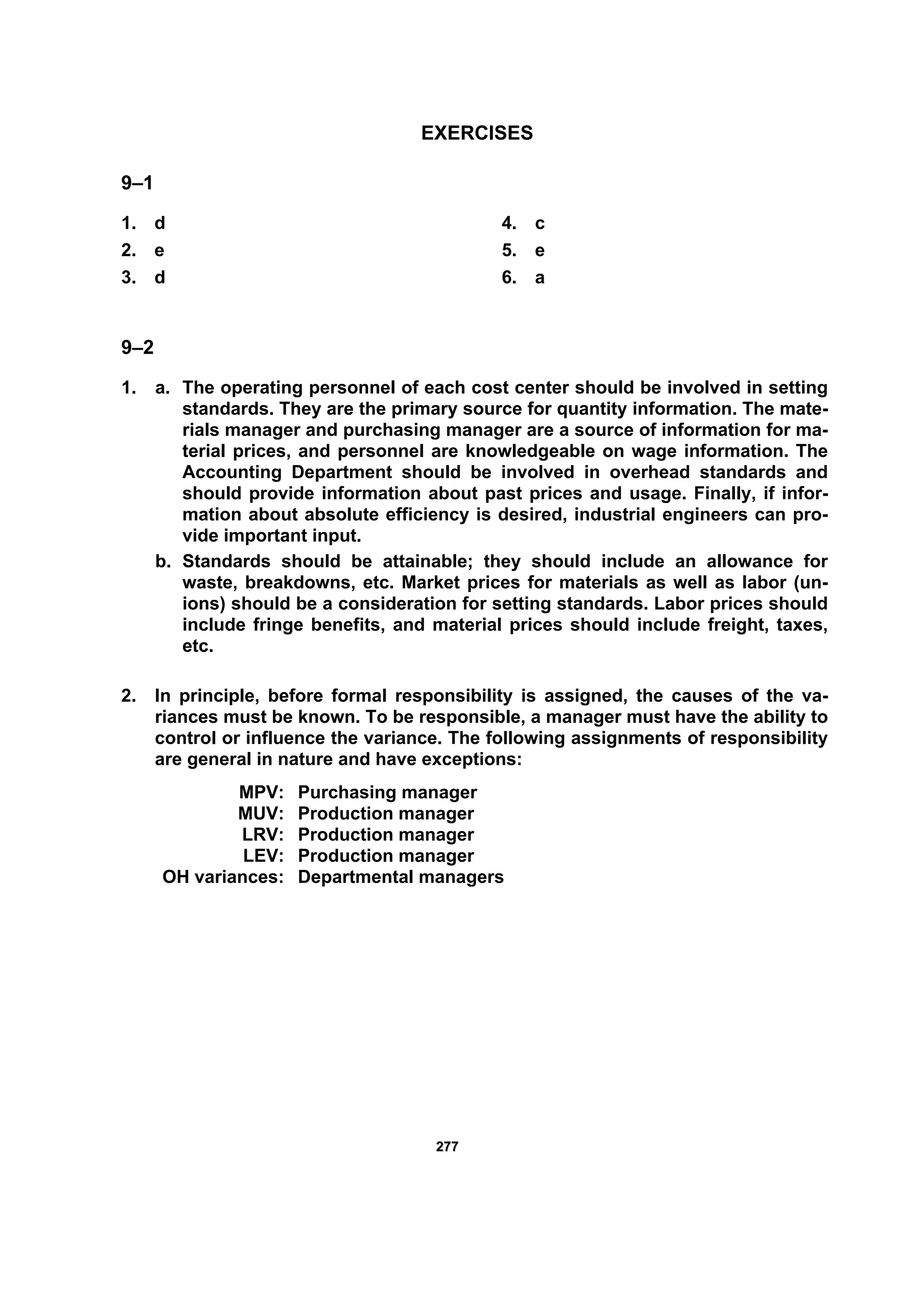

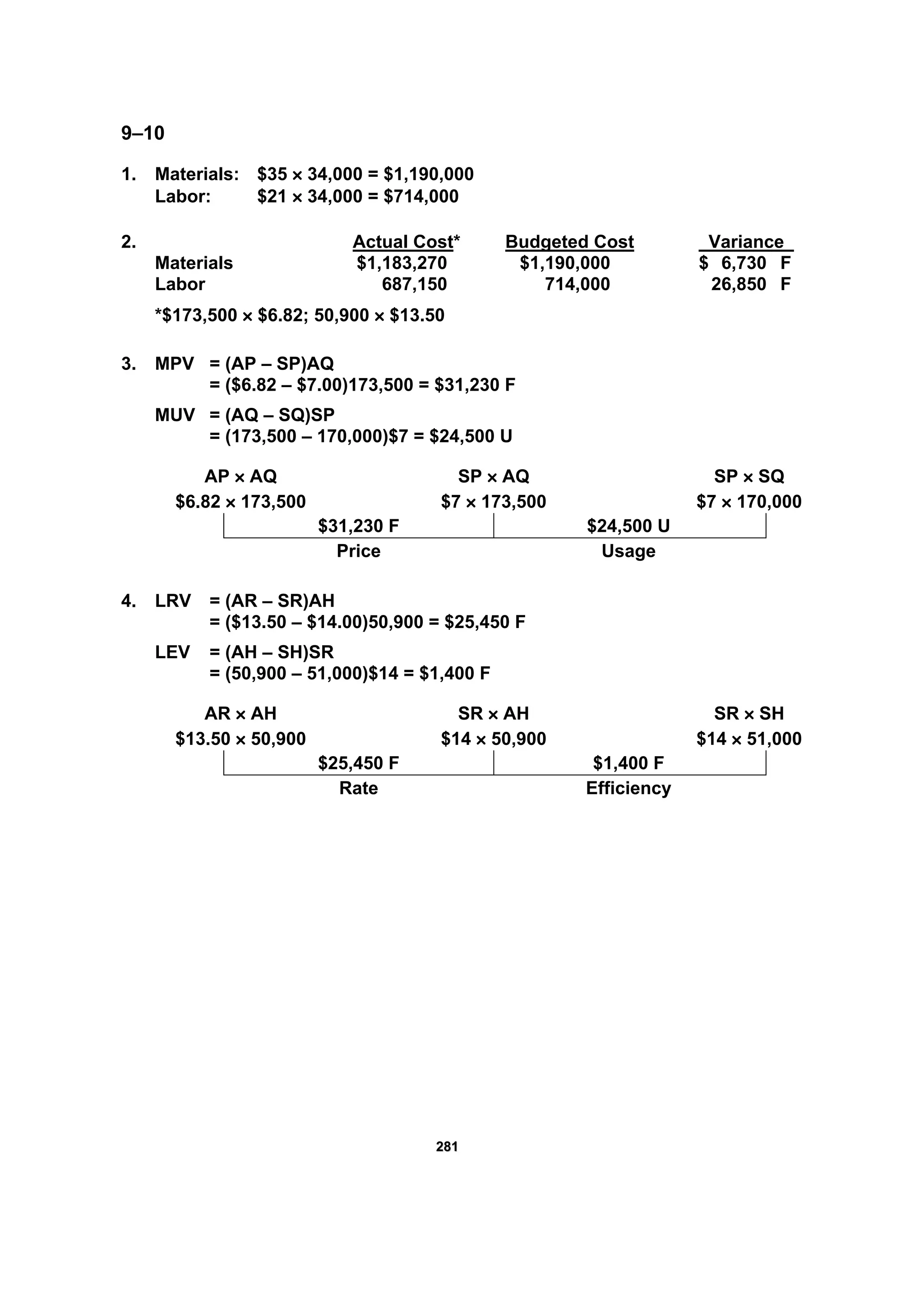

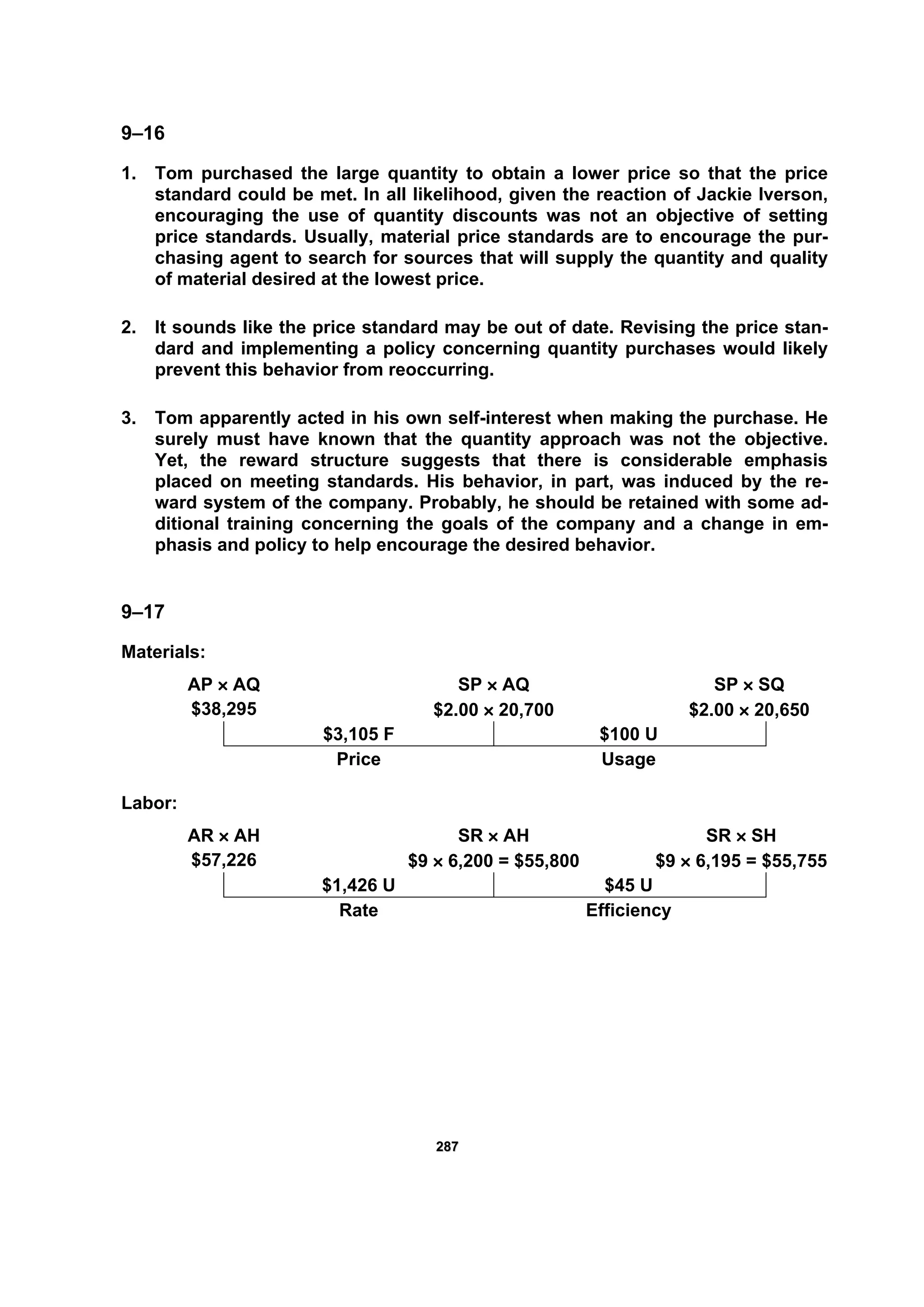

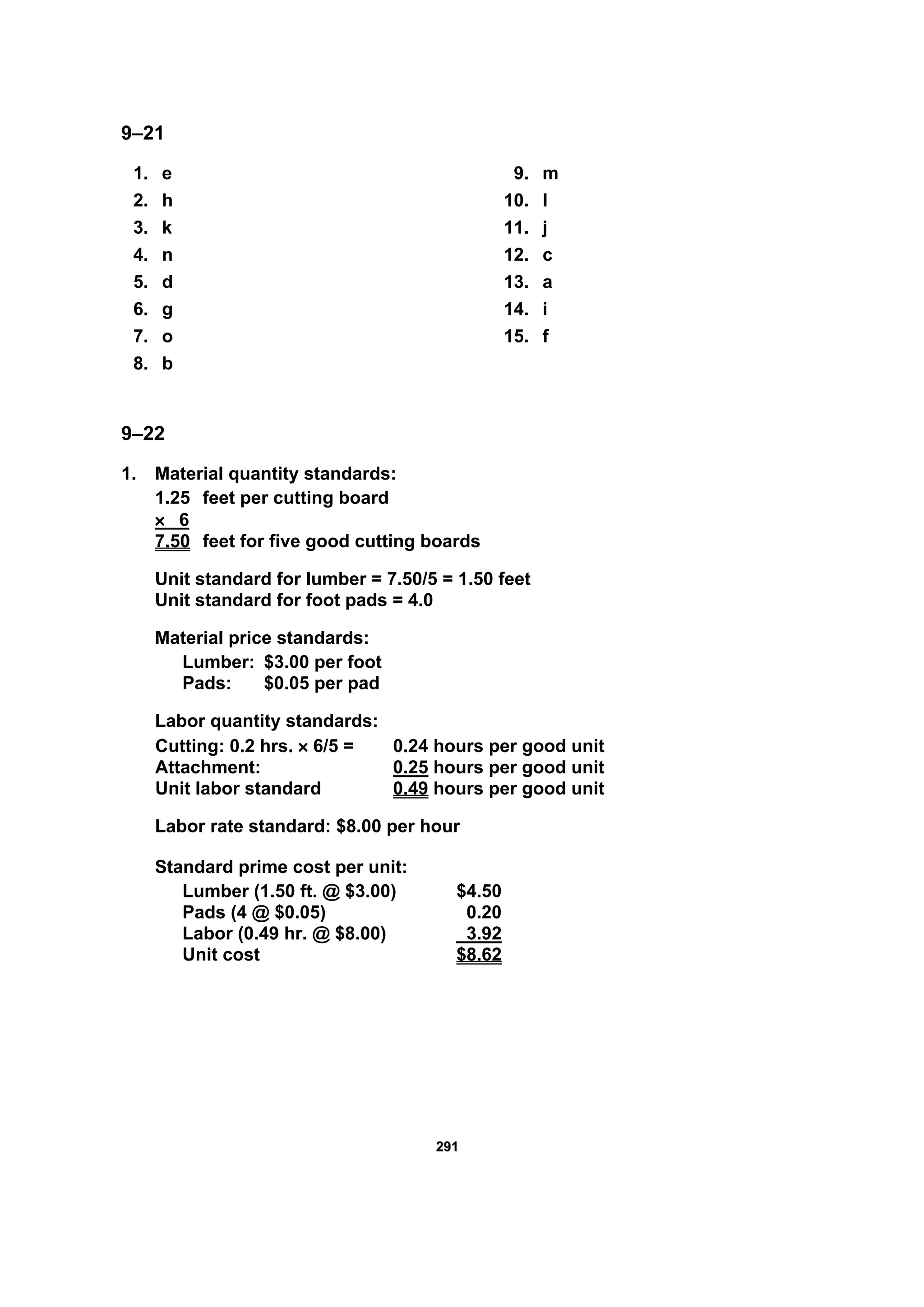

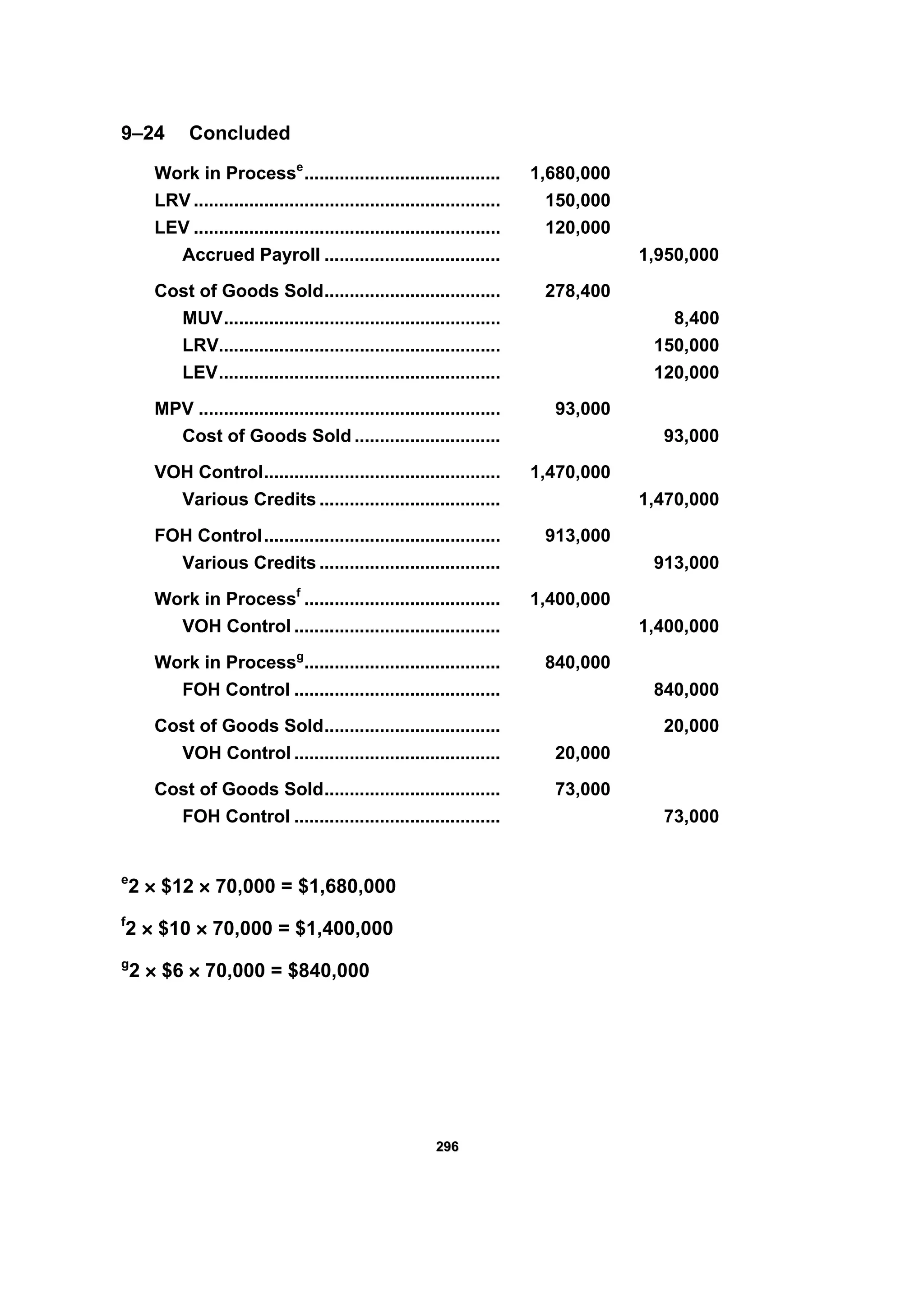

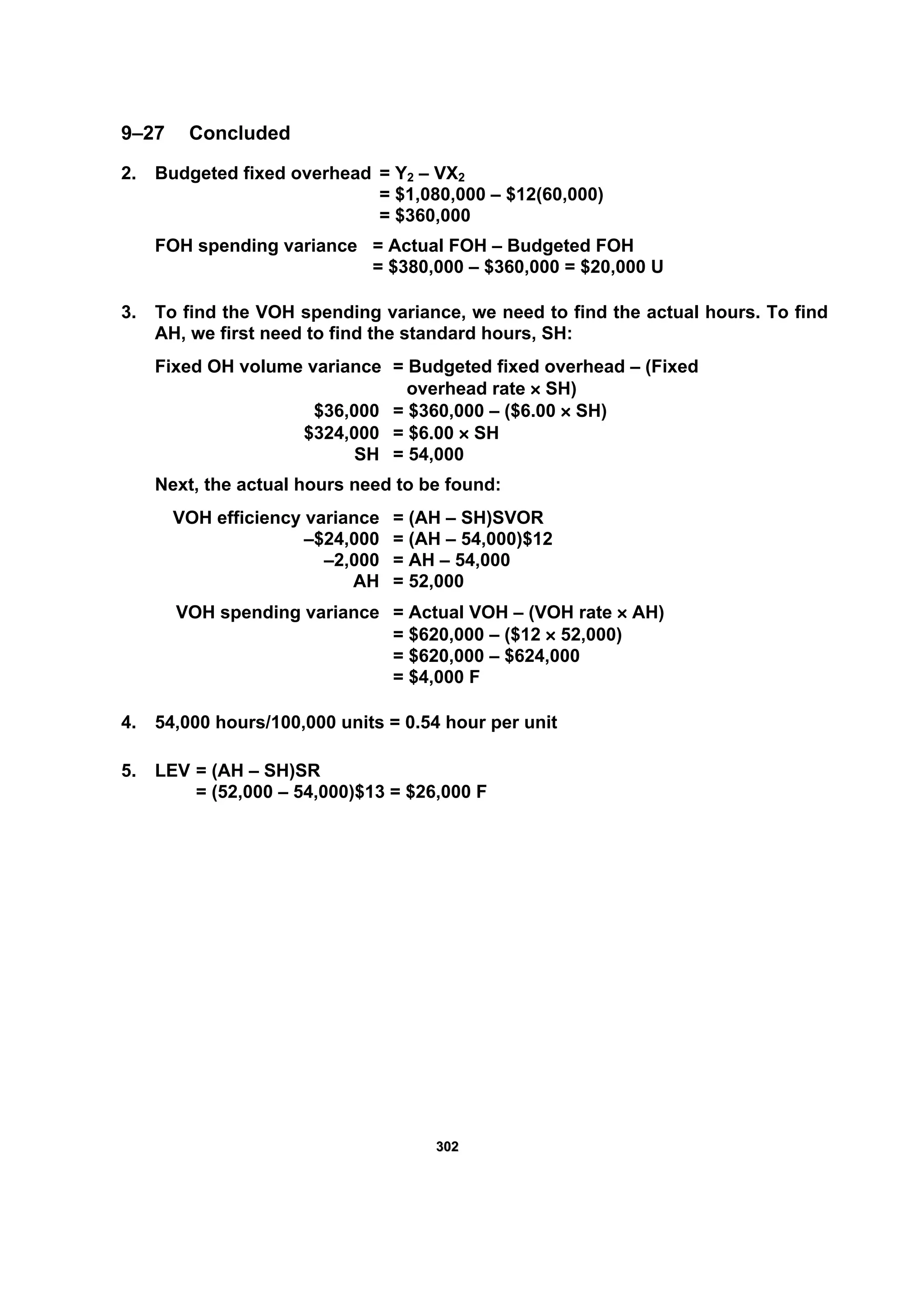

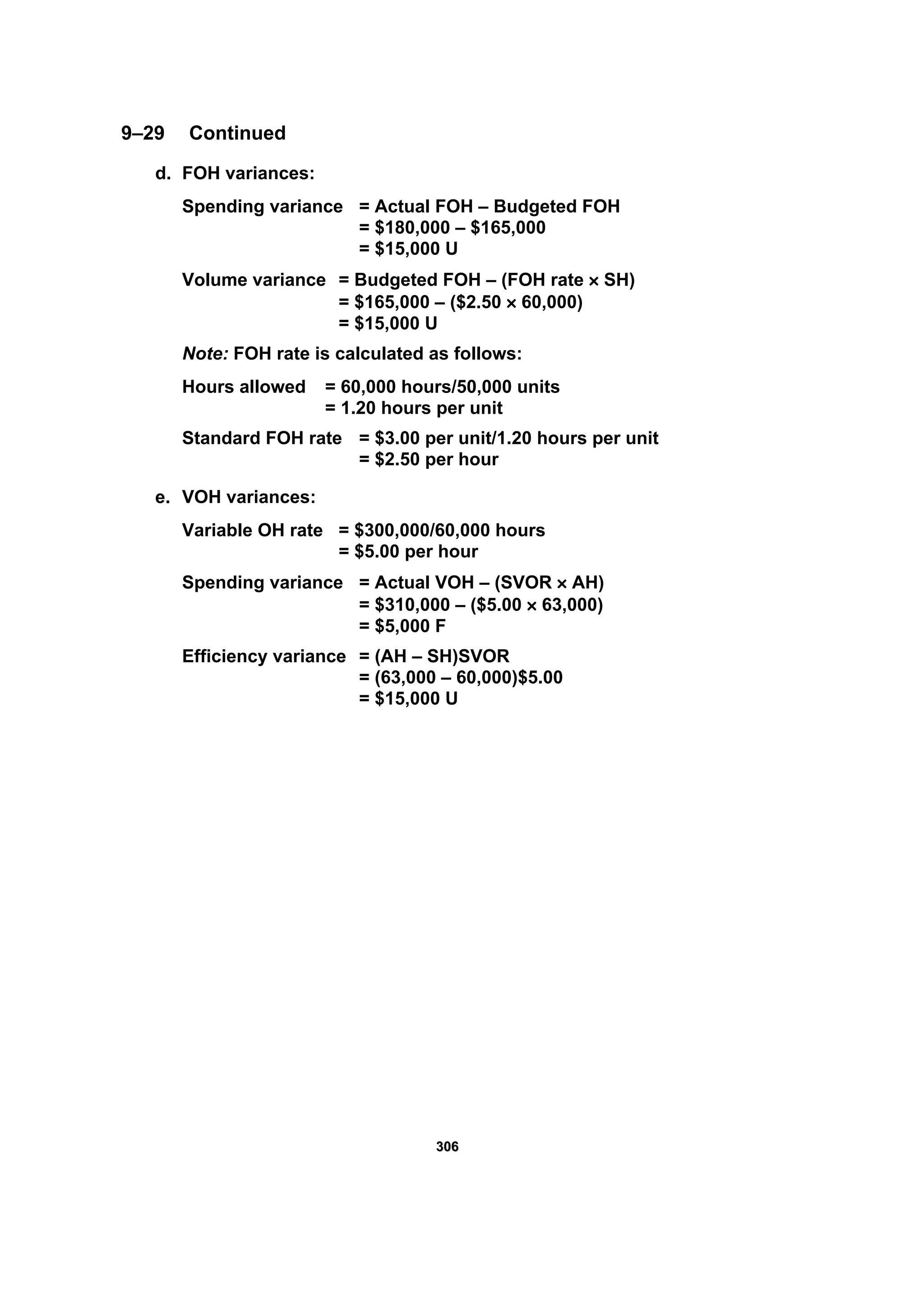

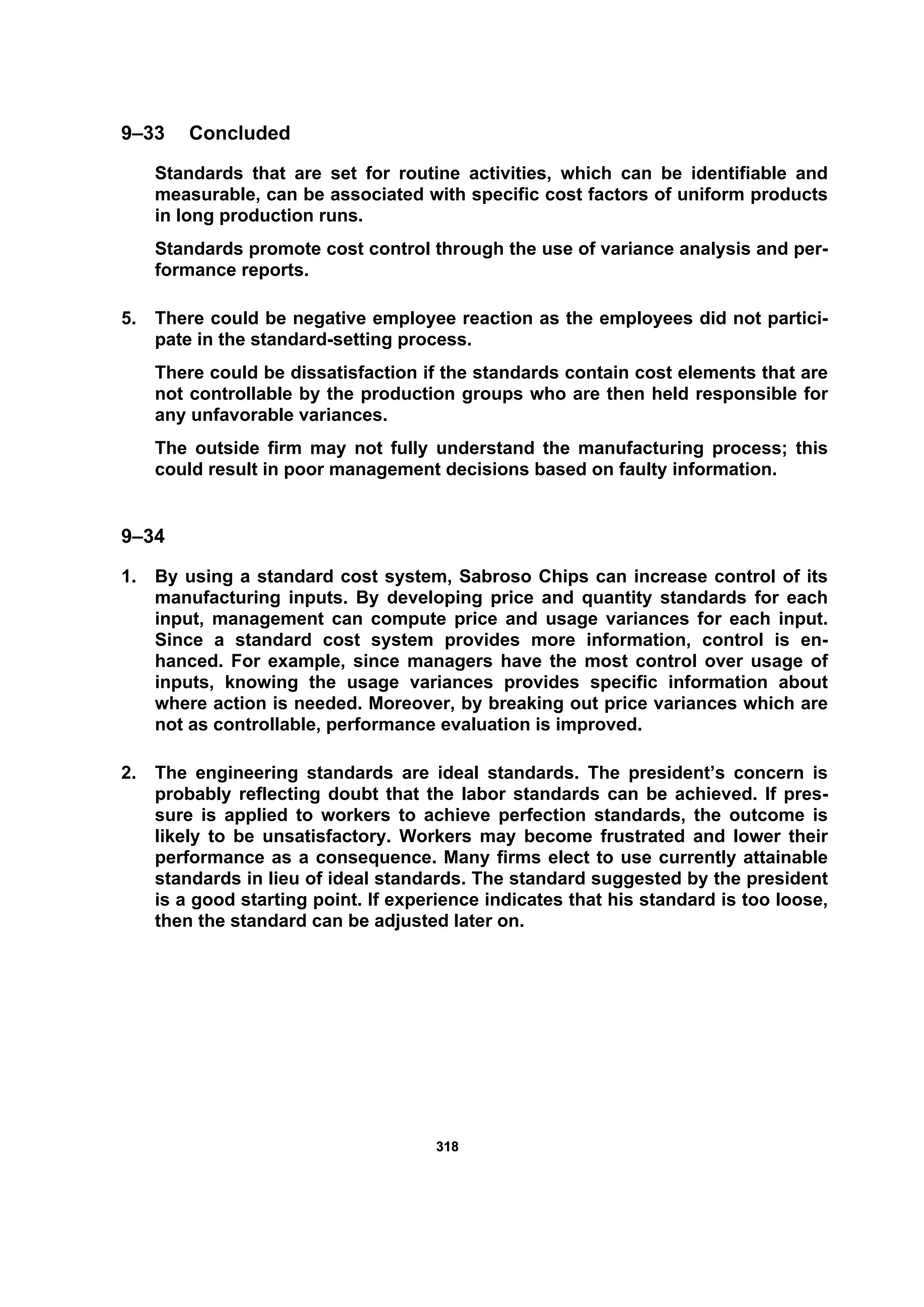

![229933

9–23

1. The cumulative average time per unit is an average. It includes the 2.5 hours

per unit when 40 units are produced as well as the 1.024 hours per unit when

640 units are produced. As more units are produced, the cumulative average

time per unit will decrease.

2. The standard should be 0.768 hour per unit as this is the average time taken

per unit once efficiency is achieved:

[(1.024 × 640) – (1.28 × 320)]/(640 – 320)

3. Std. Price Std. Usage Std. Cost

Direct materials $ 4 25.000 $100.00

Direct labor 15 0.768 11.52

Variable overhead 8 0.768 6.14

Fixed overhead 12 0.768 9.22*

Standard cost per unit $126.88*

*Rounded

4. There would be unfavorable efficiency variances for the first 320 units be-

cause the standard hours are much lower than the actual hours at this level.

Actual hours would be approximately 409.60 (320 × 1.28), and standard hours

would be 245.76 (320 × 0.768).

9–24

1. MPV = (AP – SP)AQ

= ($5.80 – $6.00)465,000 = $93,000 F

MUV = (AQ – SQ)SP

= (491,400* – 490,000)$6 = $8,400 U

* AQ = 26,400 + 465,000 − 0 = 491,400

The materials usage variance is viewed as the most controllable because

prices for materials are often market-driven and thus not controllable. Re-

sponsibility for the variance in this case likely would be assigned to purchas-

ing. The lower-quality materials are probably the cause of the extra usage.](https://image.slidesharecdn.com/ch9-171016134546/75/Chapter-9-Standard-Costing-A-Managerial-Control-Tool-19-2048.jpg)

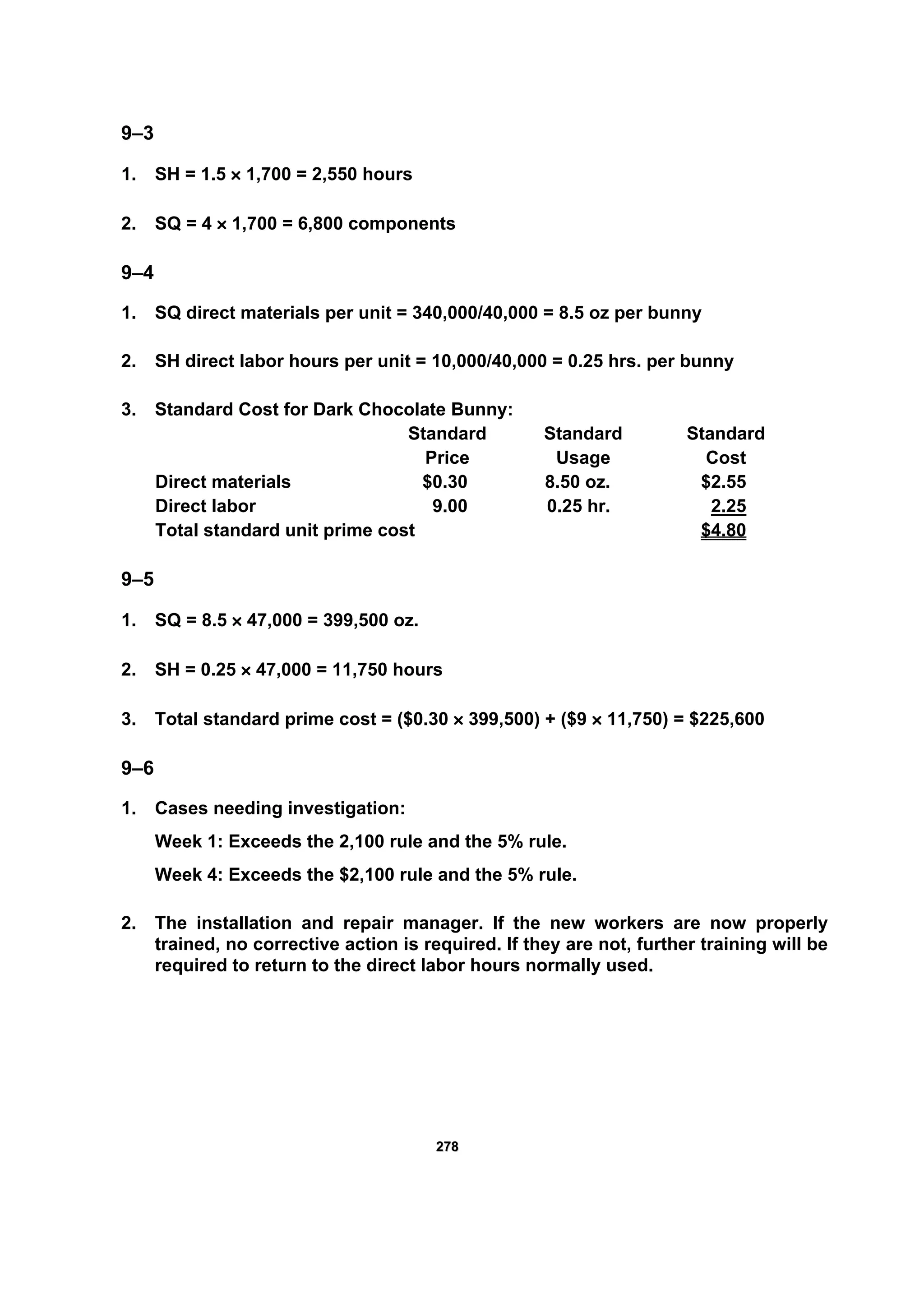

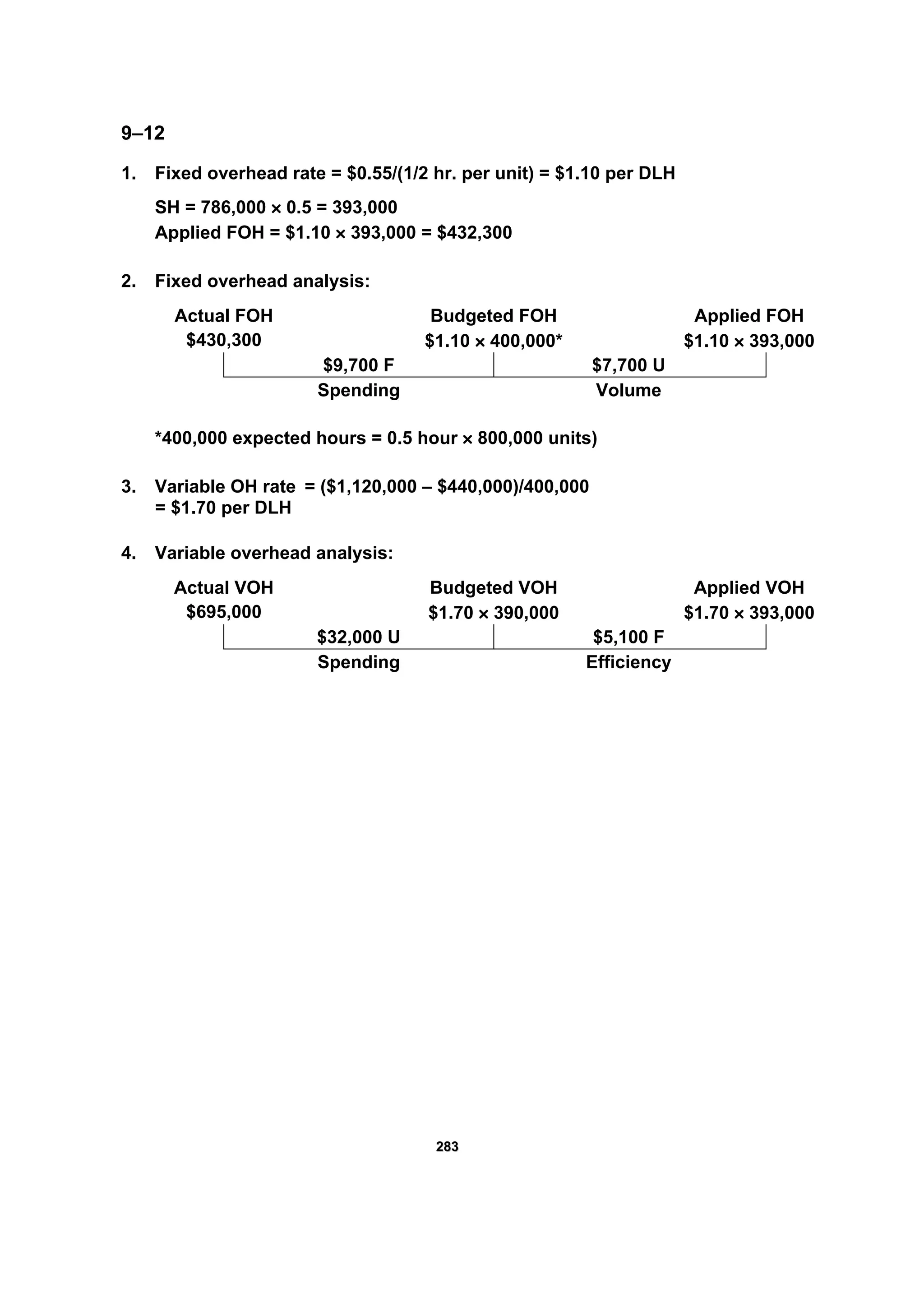

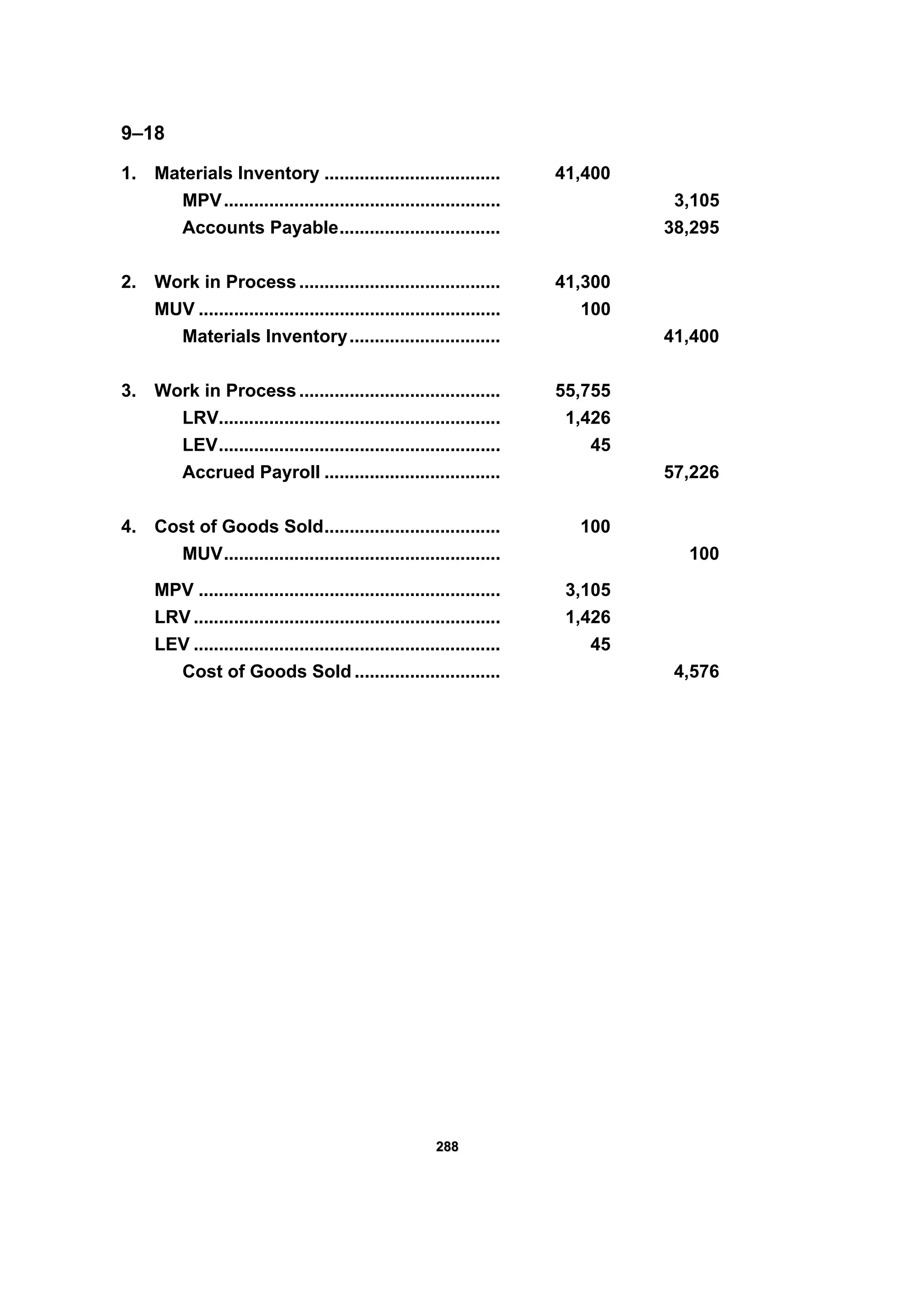

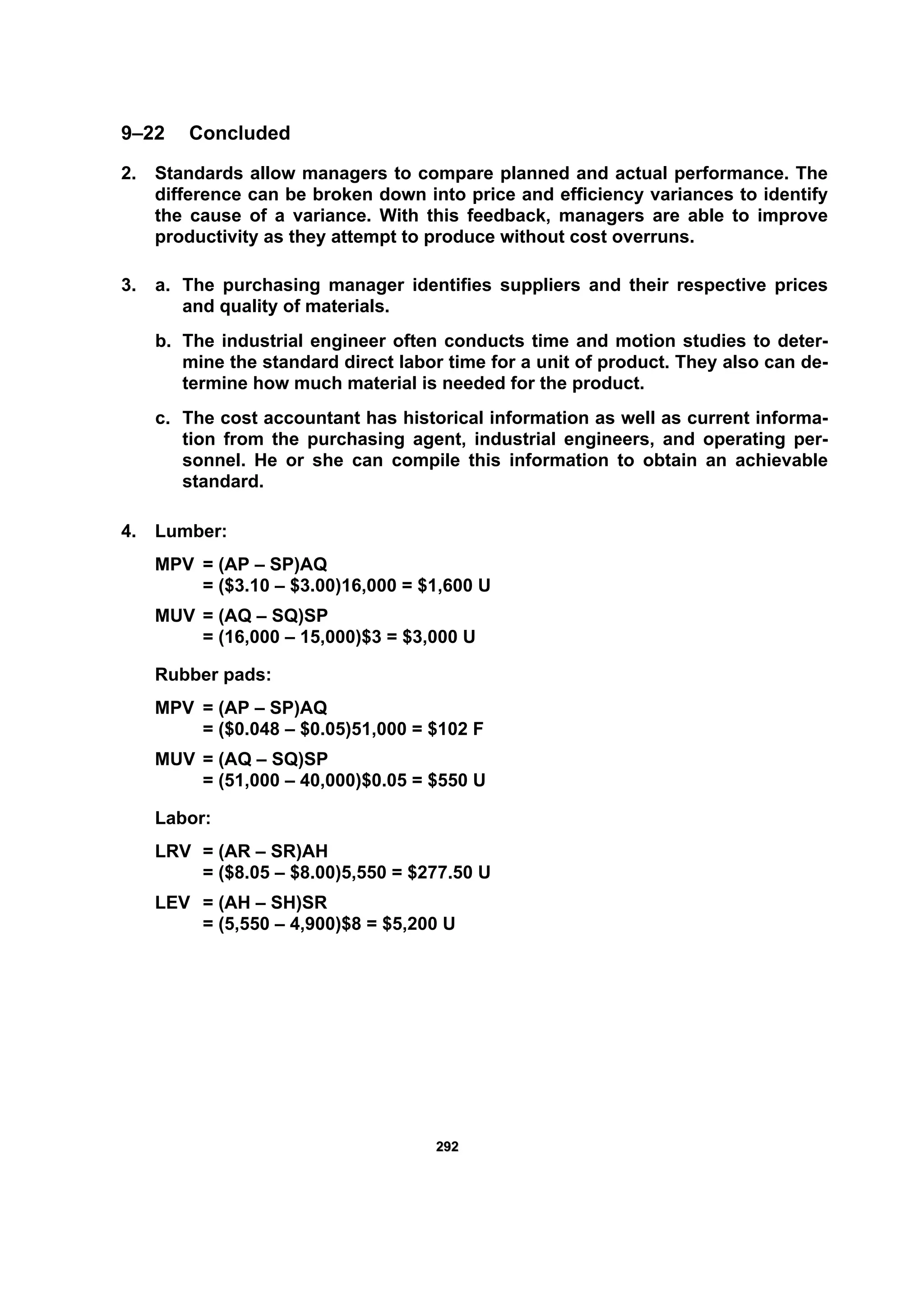

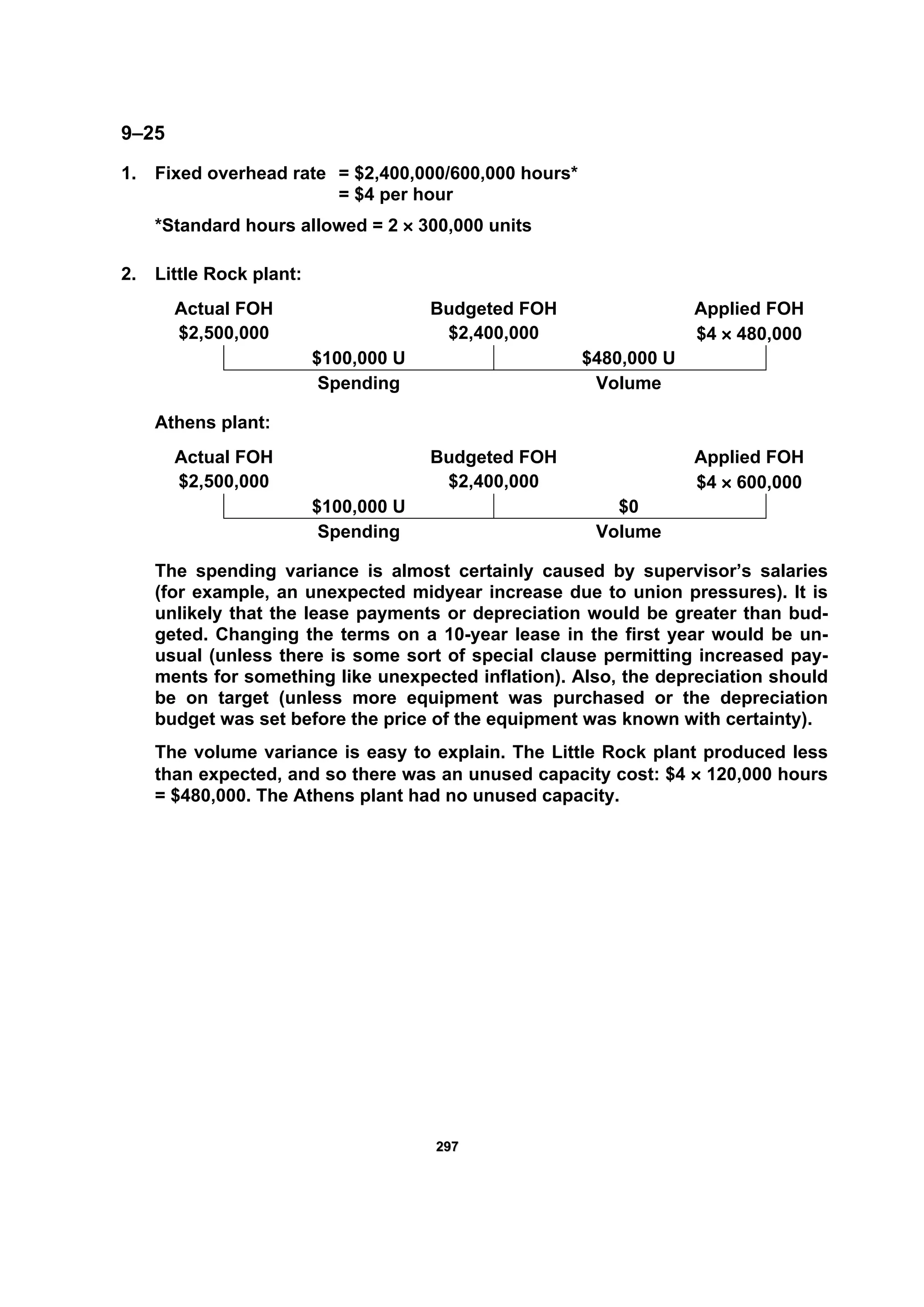

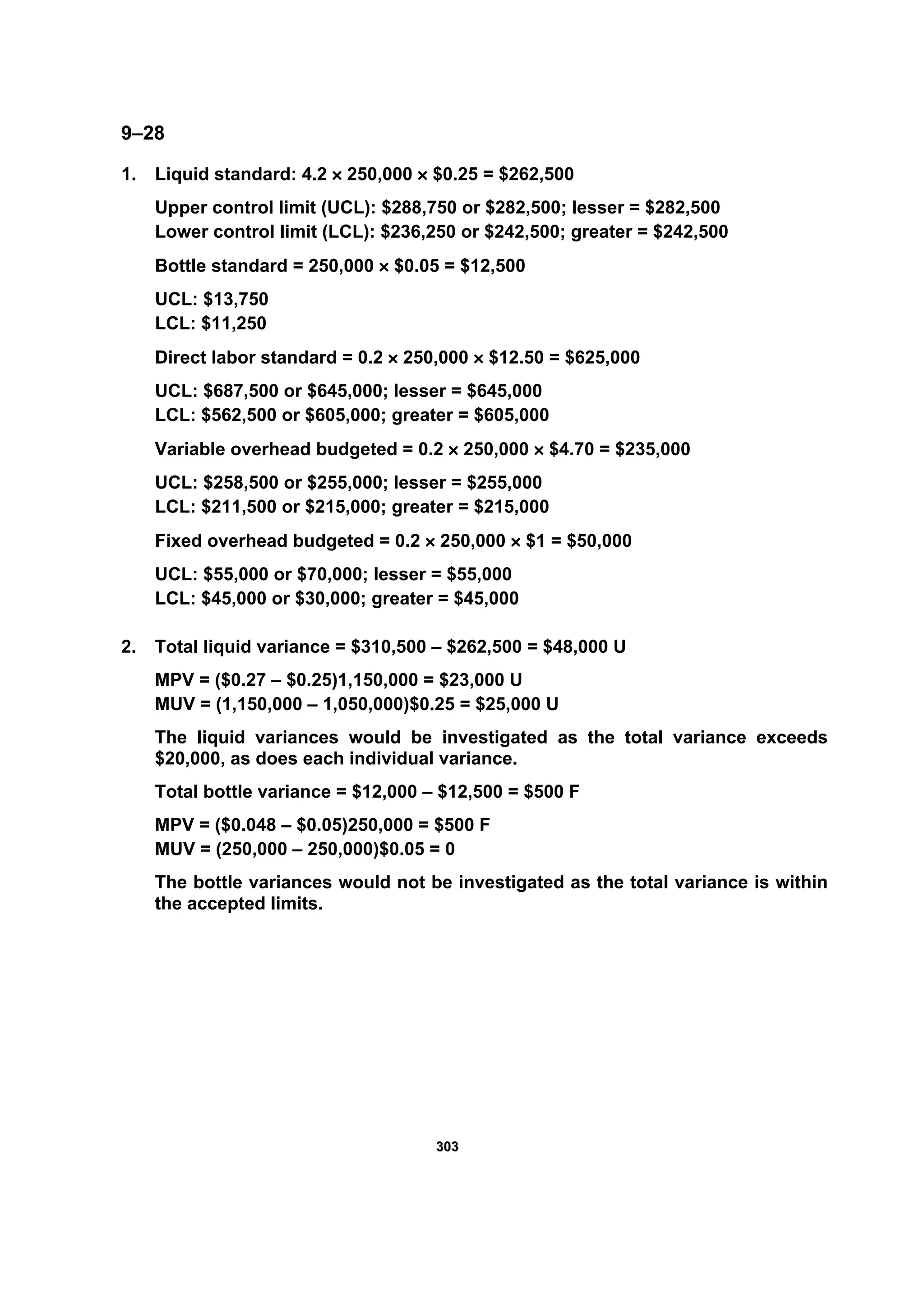

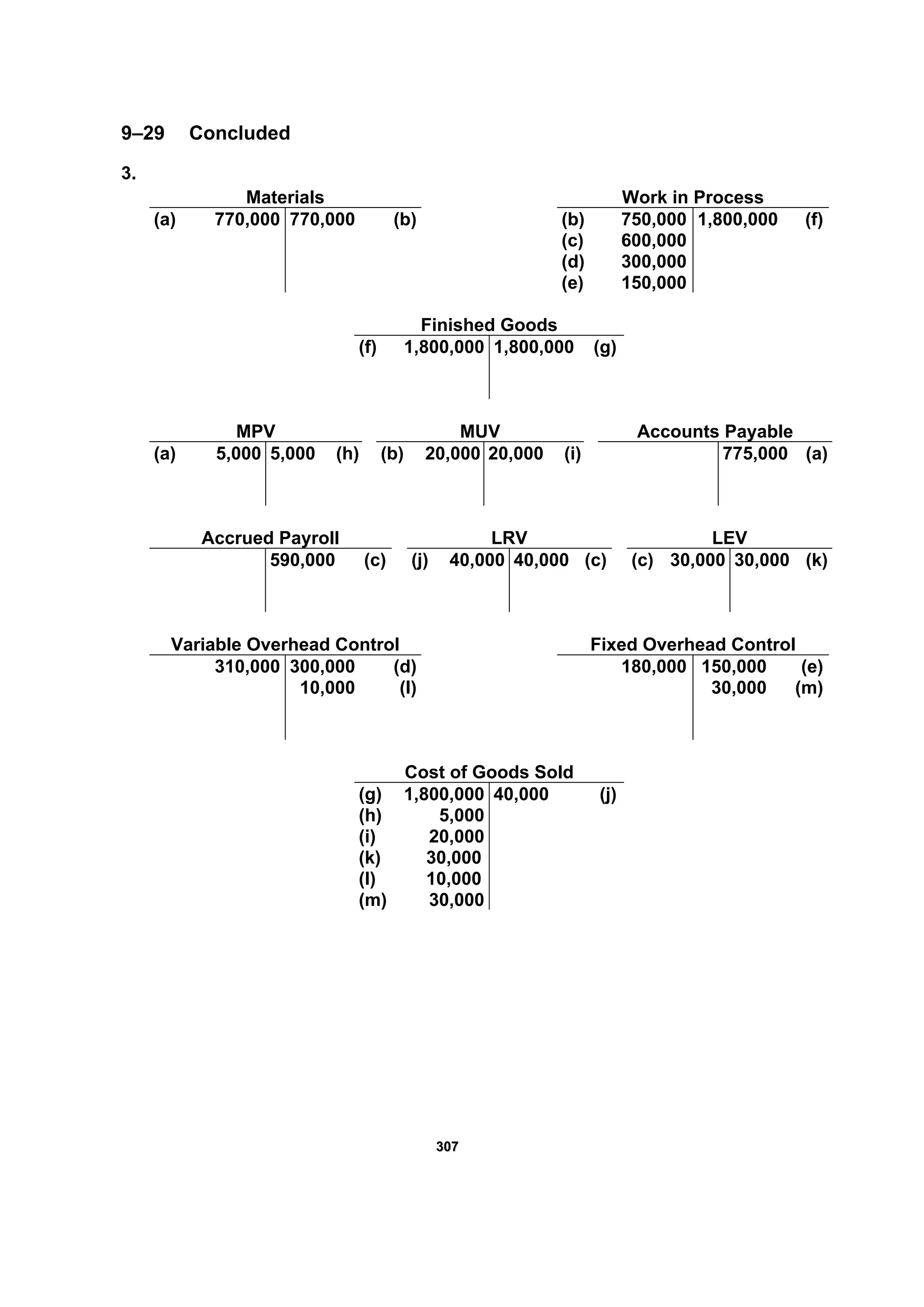

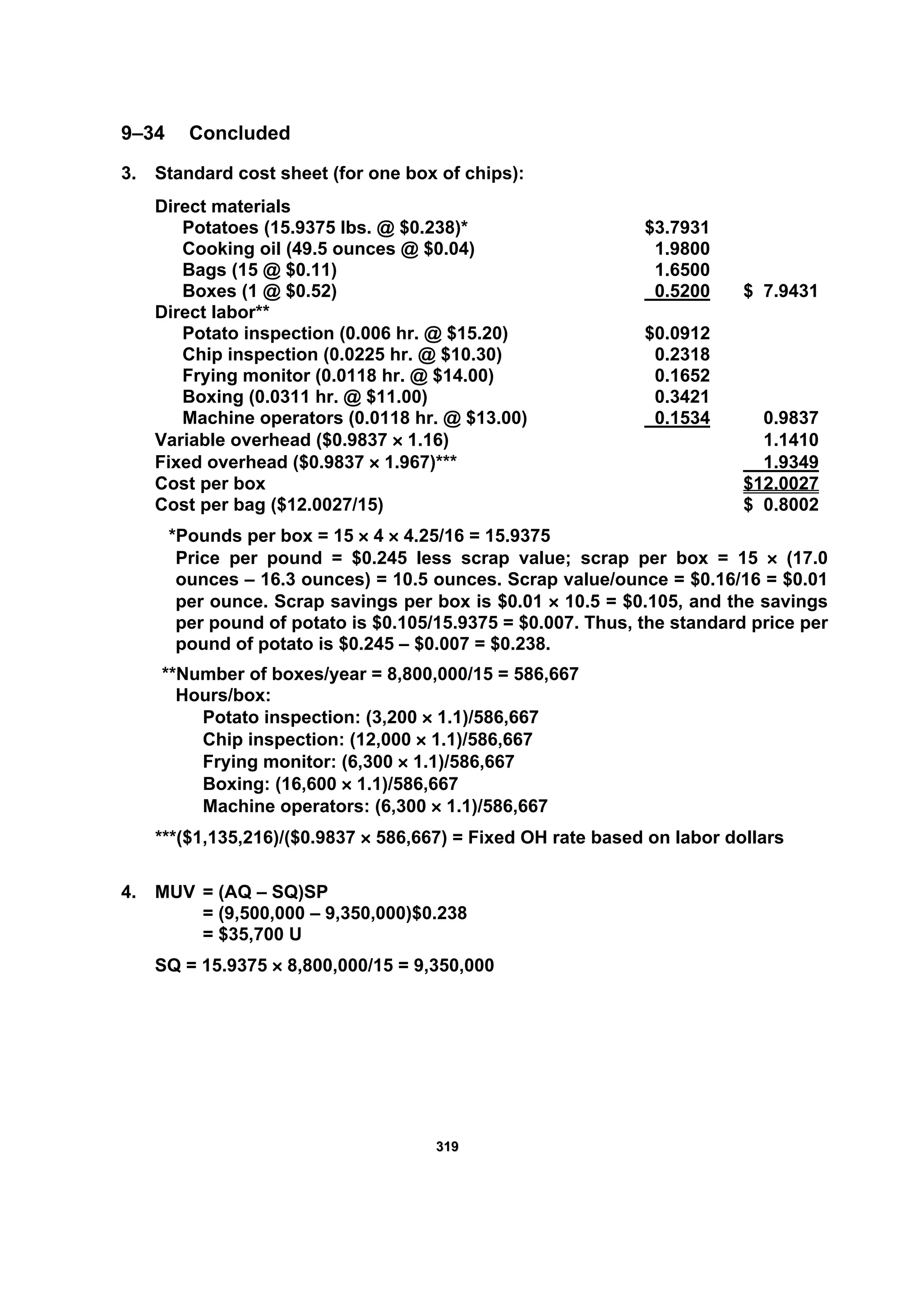

![229999

9–26

1. Normal Patient Day:

Standard Standard Standard

Price Usage Cost

Direct materials $10.00 8.00 lb. $ 80.00

Direct labor 16.00 2 hr. 32.00

Variable overhead 30.00 2 hr. 60.00

Fixed overhead 40.00 2 hr. 80.00

Unit cost $252.00

Cesarean Patient Day:

Standard Standard Standard

Price Usage Cost

Direct materials $10.00 20.00 lb. $200.00

Direct labor 16.00 4 hr. 64.00

Variable overhead 30.00 4 hr. 120.00

Fixed overhead 40.00 4 hr. 160.00

Unit cost $544.00

2. MPV = (AP – SP)AQ

= ($9.50 – $10.00)172,000 = $86,000 F

MUV = (AQ – SQ)SP

MUV (Normal) = [30,000 – (8 × 3,500)]$10 = $20,000 U

MUV (Cesarean) = [142,000 – (20 × 7,000)]$10 = $20,000 U

Materials..................................................... 1,720,000

MPV....................................................... 86,000

Accounts Payable................................ 1,634,000

Work in Process........................................ 1,680,000

MUV ............................................................ 40,000

Materials ............................................... 1,720,000

MPV ............................................................ 86,000

MUV ............................................................ 40,000

Cost of Services Sold.......................... 46,000](https://image.slidesharecdn.com/ch9-171016134546/75/Chapter-9-Standard-Costing-A-Managerial-Control-Tool-25-2048.jpg)

![330000

9–26 Continued

3. LRV = (AR – SR)AH

= ($15.90 – $16.00)36,500 = $3,650 F

LEV = (AH – SH)SR

LEV (Normal) = [7,200 – (2 × 3,500)]$16 = $3,200 U

LEV (Cesarean) = [29,300 – (4 × 7,000)]$16 = $20,800 U

Work in Process........................................ 560,000*

LEV ............................................................. 24,000

LRV........................................................ 3,650

Accrued Payroll ................................... 580,350

*[(2 × 3,500) + (4 × 7,000)] × $16 = $560,000

Cost of Services Sold ............................... 20,350

LRV ............................................................. 3,650

LEV........................................................ 24,000

4. Variable overhead variances:

Actual VOH Budgeted VOH Applied VOH

$1,215,000 $40 × 36,500 $40 × 35,000

$245,000 F $60,000 U

Spending Efficiency

Fixed overhead variances:

Actual FOH Budgeted FOH Applied FOH

$700,000 $720,000 $30 × 35,000

$20,000 F $330,000 F

Spending Volume

Note: SH = (2 × 3,500) + (4 × 7,000) = 35,000](https://image.slidesharecdn.com/ch9-171016134546/75/Chapter-9-Standard-Costing-A-Managerial-Control-Tool-26-2048.jpg)

1. The document discusses standard costing and variances. It provides sample calculations for setting standards and analyzing variances. 2. Standard costs are set for direct materials, direct labor, and overhead. Variances are calculated between actual and standard amounts to identify areas for improvement. 3. Managers are responsible for investigating significant variances that they can control, such as labor efficiency or spending variances, to determine the cause and take corrective action if needed.