Downloaded 38 times

![559966

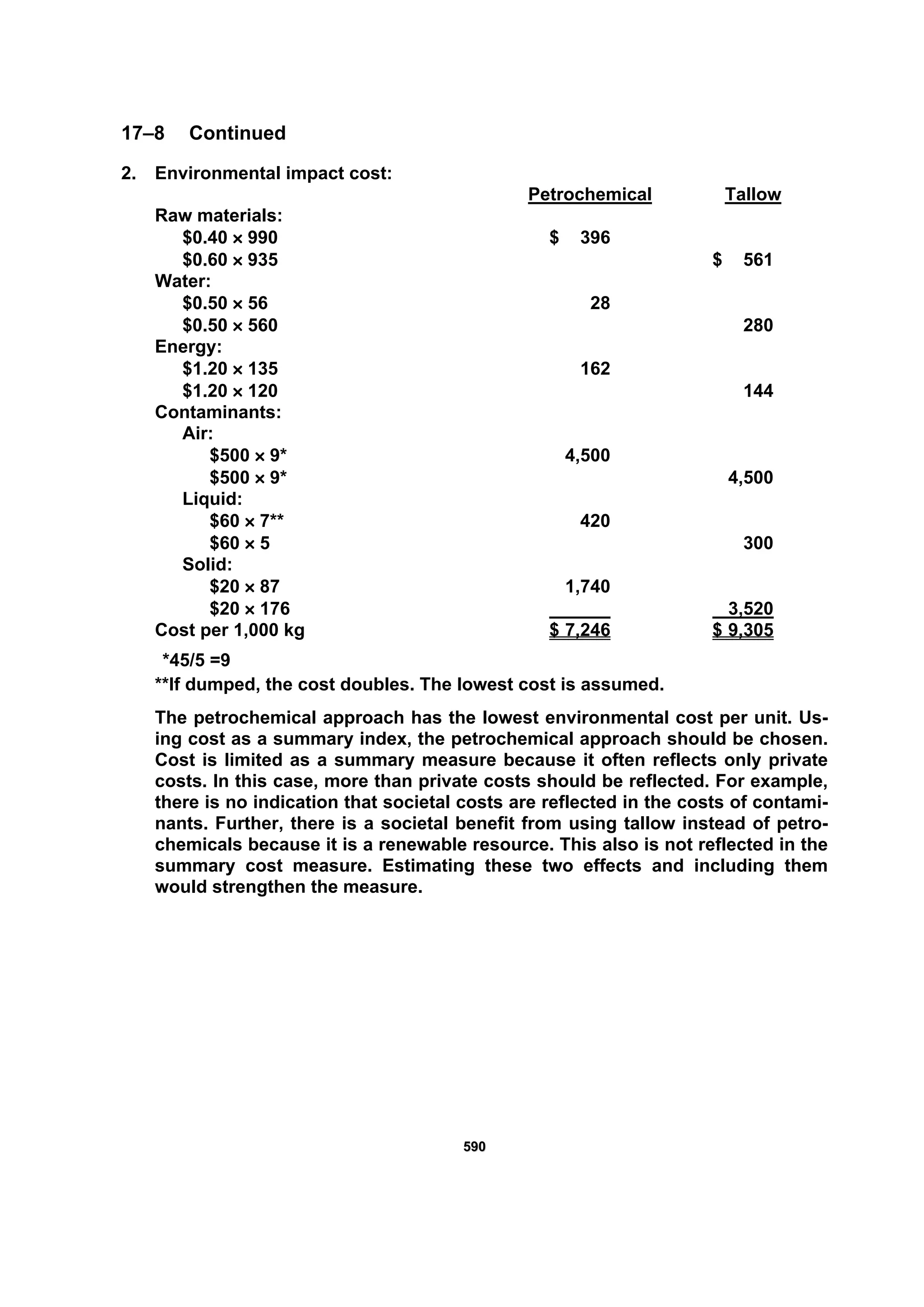

17–12 Concluded

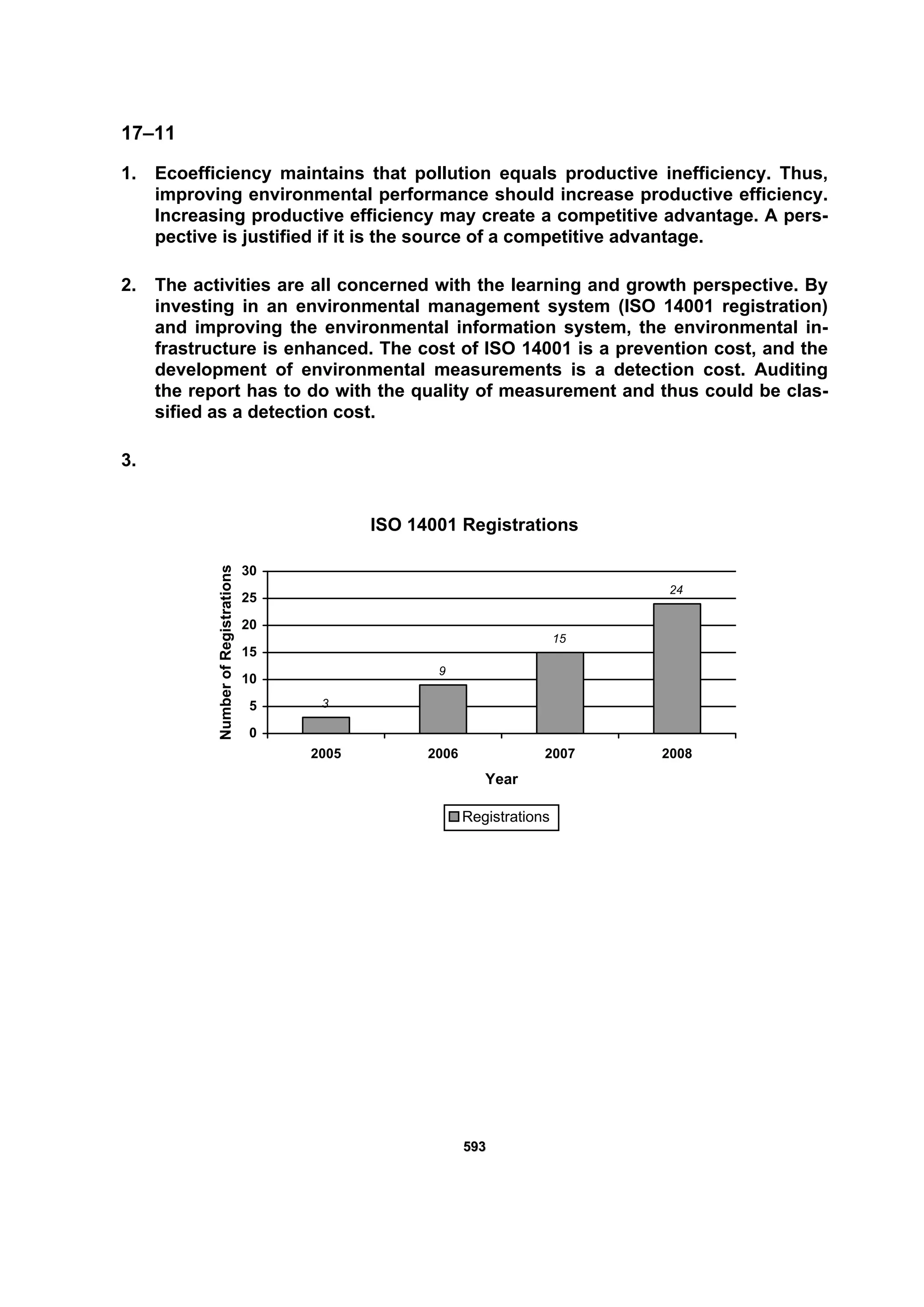

2.

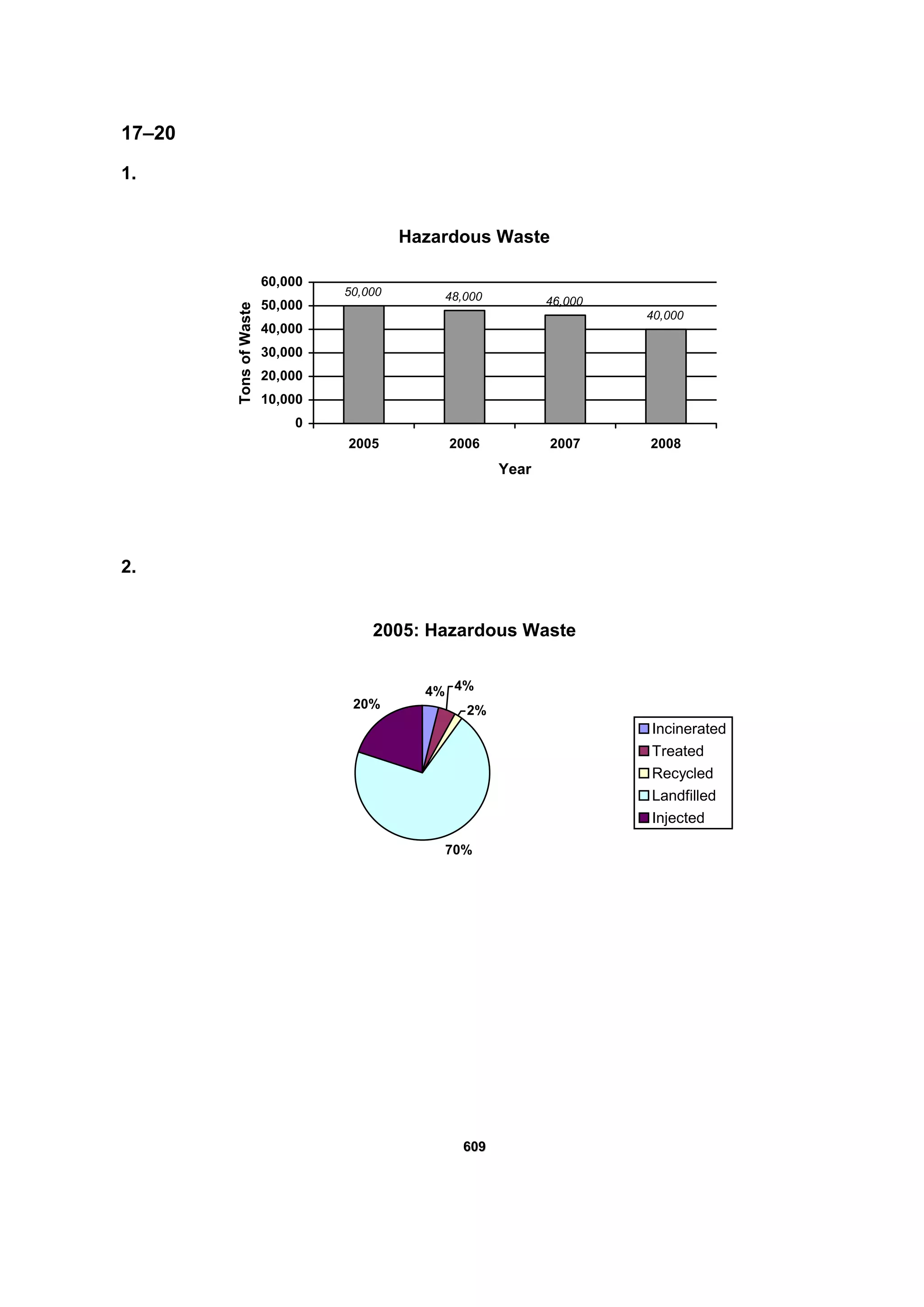

Normalized Energy Consumption

12,000

11,800

10,545

10,364

9,500

10,000

10,500

11,000

11,500

12,000

12,500

2005 2006 2007 2008

Year

BTUs/Sales

BTUs/Sales

Energy consumption has dropped from 12,000 BTUs per sales dollar to 10,364

BTUs per sales dollar, a 13.63 percent improvement [(12,000 – 10,364)/12,000].

This compares with a 5 percent improvement for the measure that is not nor-

malized. The 13.63 percent is a more meaningful measure because it reflects

the need to increase energy consumption as output increases.](https://image.slidesharecdn.com/ch17-171016223541/75/Chapter-17-Environmental-Cost-Management-16-2048.jpg)

This document discusses environmental cost management and eco-efficiency. It provides examples of how to calculate activity rates and assign environmental costs to products using activity-based costing. It shows how improving environmental performance through reducing materials usage and emissions can lower production costs. Tracking environmental costs can identify opportunities to lower costs while reducing impacts. Assigning full environmental costs provides the most complete picture, though firms often only report private costs.