Downloaded 78 times

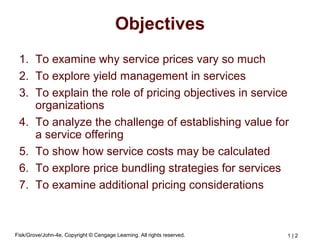

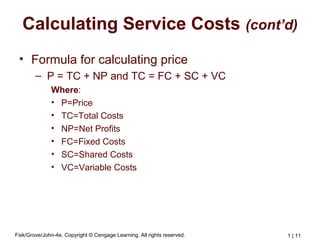

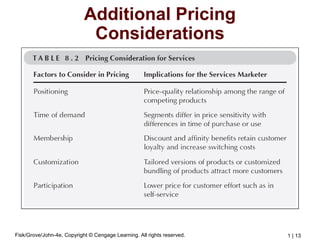

The document discusses several factors to consider when setting prices for services. It examines why service prices vary, the role of yield management and pricing objectives. Pricing objectives can be profit-oriented, volume-oriented or based on costs, customers or competition. When establishing value, services consider cost-benefit analysis and price elasticity. Calculating costs involves direct, indirect, fixed, variable and allocated costs. Price bundling groups services at one price. Additional considerations include inseparability, perishability, maximizing revenues and reducing costs per customer.