Downloaded 2,369 times

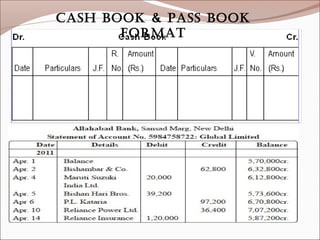

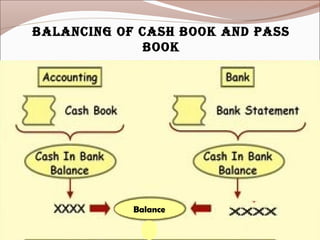

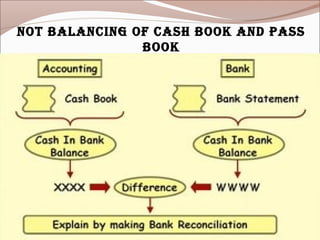

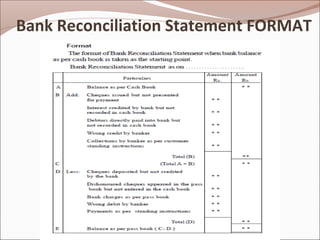

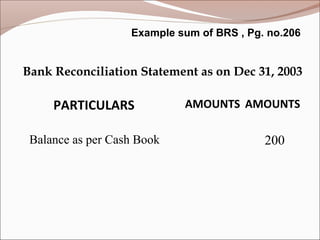

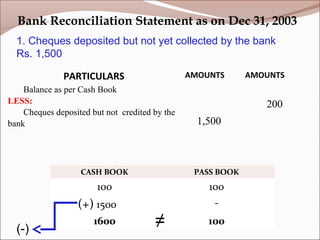

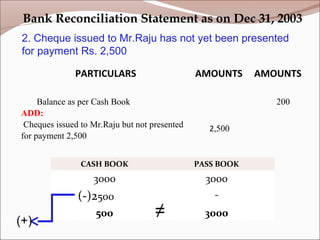

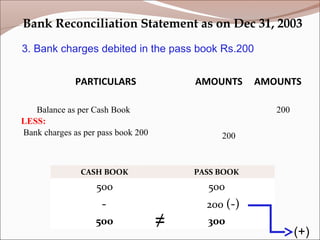

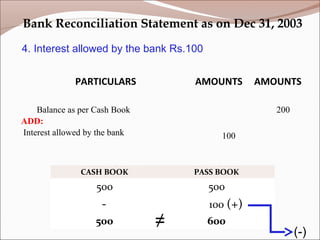

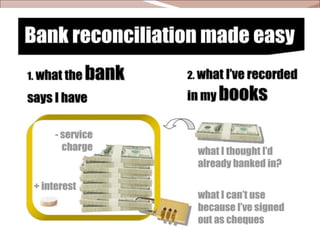

A bank is a financial institution that creates money by lending money to borrowers, generating corresponding deposits on its balance sheet. Cash books and pass books are accounting records used by banks and customers. A bank reconciliation statement reconciles the balance in a cash book to the balance in a pass book, accounting for discrepancies like outstanding deposits or checks. Common reconciling items include checks that have been deposited but not cleared, checks issued but not cashed, bank charges, interest earned, and direct payments made by the bank.