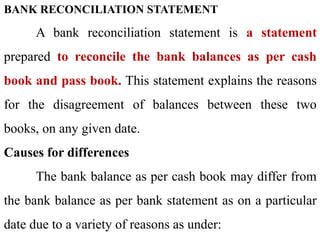

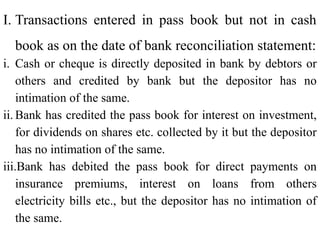

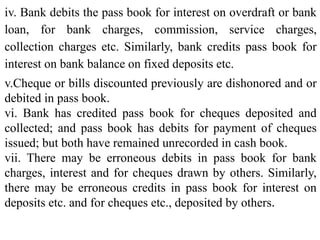

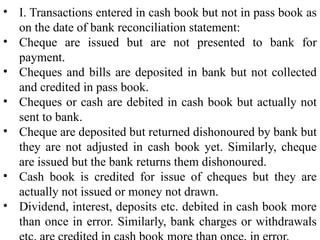

A bank reconciliation statement is prepared to reconcile the balances between a cash book and a pass book, detailing the reasons for any discrepancies. Differences may arise due to transactions not recorded in one of the books, such as direct deposits or dishonored checks. Preparing this statement ensures accuracy, detects errors, and prevents fraudulent transactions in financial records.