Downloaded 49 times

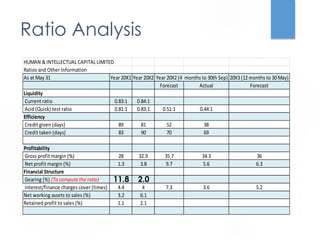

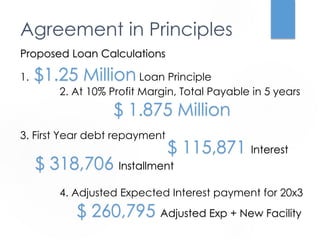

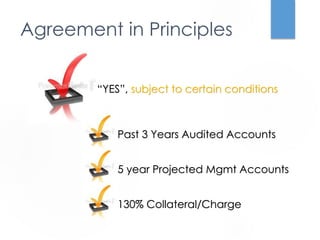

The bank manager met with the MD of HICL, a six-year-old consumer company going through rapid expansion. HICL is seeking medium-term financing of $1.2 million to consolidate operations across three locations into a new single office. The bank analyzed HICL's financial ratios and statements over several years, forecasted projections, and proposed a $1.25 million loan at 10% interest over 5 years, subject to certain conditions.