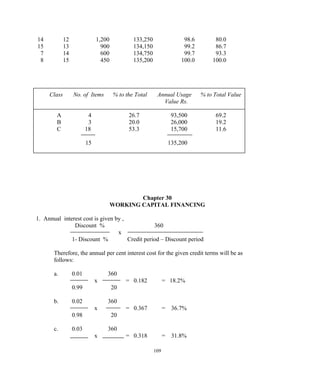

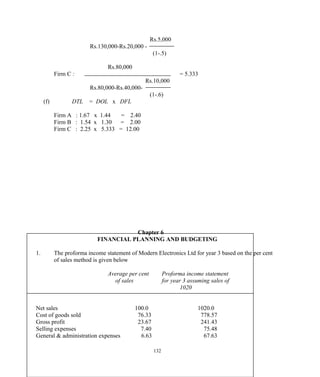

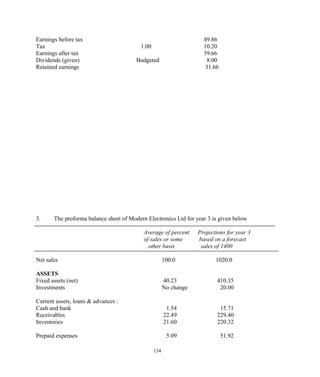

This document contains 32 numerical problems related to time value of money concepts. Some key details summarized:

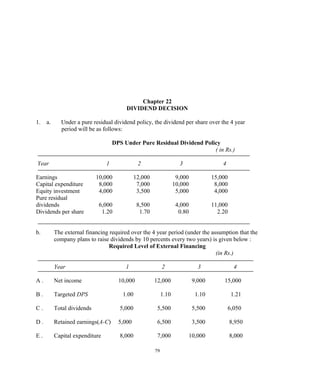

- Problem 1 calculates future values over 5 years at interest rates of 8%, 10%, 12%, and 15%.

- Problem 15 uses linear interpolation to find an implied interest rate of 15.1% between given values.

- Problem 32 calculates the present value of expected iron ore mining revenues over 15 years, discounting for price escalation of 6% annually.

![PVIF (12%, 4 years) + Rs.500 x PVIF (12%, 5 years) +

Rs.600 x PVIF (12%, 6 years) + Rs.700 x PVIF (12%, 7 years) +

Rs.800 x PVIF (12%, 8 years) + Rs.900 x PVIF (12%, 9 years) +

Rs.1,000 x PVIF (12%, 10 years)

= Rs.100 x 0.893 + Rs.200 x 0.797 + Rs.300 x 0.712

+ Rs.400 x 0.636 + Rs.500 x 0.567 + Rs.600 x 0.507

+ Rs.700 x 0.452 + Rs.800 x 0.404 + Rs.900 x 0.361

+ Rs.1,000 x 0.322

= Rs.2590.9

Similarly,

PV (Stream B) = Rs.3,625.2

PV (Stream C) = Rs.2,851.1

17. FV5 = Rs.10,000 [1 + (0.16 / 4)]5x4

= Rs.10,000 (1.04)20

= Rs.10,000 x 2.191

= Rs.21,910

18. FV5 = Rs.5,000 [1+( 0.12/4)] 5x4

= Rs.5,000 (1.03)20

= Rs.5,000 x 1.806

= Rs.9,030

19 A B C

Stated rate (%) 12 24 24

Frequency of compounding 6 times 4 times 12 times

Effective rate (%) (1 + 0.12/6)6

- 1 (1+0.24/4)4

–1 (1 + 0.24/12)12

-1

= 12.6 = 26.2 = 26.8

Difference between the

effective rate and stated

rate (%) 0.6 2.2 2.8

20. Investment required at the end of 8th

year to yield an income of Rs.12,000 per year from the

end of 9th

year (beginning of 10th

year) for ever:

Rs.12,000 x PVIFA(12%, ∞ )

4](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-4-320.jpg)

![= Rs.12,000 / 0.12 = Rs.100,000

To have a sum of Rs.100,000 at the end of 8th

year , the amount to be deposited now is:

Rs.100,000 Rs.100,000

= = Rs.40,388

PVIF(12%, 8 years) 2.476

21. The interest rate implicit in the offer of Rs.20,000 after 10 years in lieu of Rs.5,000 now is:

Rs.5,000 x FVIF (r,10 years) = Rs.20,000

Rs.20,000

FVIF (r,10 years) = = 4.000

Rs.5,000

From the tables we find that

FVIF (15%, 10 years) = 4.046

This means that the implied interest rate is nearly 15%.

I would choose Rs.20,000 for 10 years from now because I find a return of 15% quite

acceptable.

22. FV10 = Rs.10,000 [1 + (0.10 / 2)]10x2

= Rs.10,000 (1.05)20

= Rs.10,000 x 2.653

= Rs.26,530

If the inflation rate is 8% per year, the value of Rs.26,530 10 years from now, in terms of

the current rupees is:

Rs.26,530 x PVIF (8%,10 years)

= Rs.26,530 x 0.463 = Rs.12,283

23. A constant deposit at the beginning of each year represents an annuity due.

PVIFA of an annuity due is equal to : PVIFA of an ordinary annuity x (1 + r)

To provide a sum of Rs.50,000 at the end of 10 years the annual deposit should

be

Rs.50,000

A = FVIFA(12%, 10 years) x (1.12)

Rs.50,000

= = Rs.2544

17.549 x 1.12

5](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-5-320.jpg)

![PVIFA (2%, 24) = 18.914

Using a linear interpolation

21.244 – 20.000

r = 1% + ---------------------- x 1%

21.244 – 18,914

= 1.53%

Thus, the bank charges an interest rate of 1.53% per month.

The corresponding effective rate of interest per annum is

[ (1.0153)12

– 1 ] x 100 = 20%

28. The discounted value of the debentures to be redeemed between 8 to 10 years evaluated at

the end of the 5th

year is:

Rs.10 million x PVIF (8%, 3 years)

+ Rs.10 million x PVIF (8%, 4 years)

+ Rs.10 million x PVIF (8%, 5 years)

= Rs.10 million (0.794 + 0.735 + 0.681)

= Rs.2.21 million

If A is the annual deposit to be made in the sinking fund for the years 1 to 5,

then

A x FVIFA (8%, 5 years) = Rs.2.21 million

A x 5.867 = Rs.2.21 million

A = 5.867 = Rs.2.21 million

A = Rs.2.21 million / 5.867 = Rs.0.377 million

29. Let `n’ be the number of years for which a sum of Rs.20,000 can be withdrawn annually.

Rs.20,000 x PVIFA (10%, n) = Rs.100,000

PVIFA (15%, n) = Rs.100,000 / Rs.20,000 = 5.000

From the tables we find that

PVIFA (10%, 7 years) = 4.868

PVIFA (10%, 8 years) = 5.335

Thus n is between 7 and 8. Using a linear interpolation we get

5.000 – 4.868

n = 7 + ----------------- x 1 = 7.3 years

5.335 – 4.868

7](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-7-320.jpg)

![Bond A Bond B

* Post-tax interest (C ) 12(1 – 0.3) 10 (1 – 0.3)

=Rs.8.4 =Rs.7

* Post-tax maturity value (M) 100 - 100 -

[ (100-70)x 0.1] [ (100 – 60)x 0.1]

=Rs.97 =Rs.96

The post-tax YTM, using the approximate YTM formula is calculated below

8.4 + (97-70)/10

Bond A : Post-tax YTM = --------------------

0.6 x 70 + 0.4 x 97

= 13.73%

7 + (96 – 60)/6

Bond B : Post-tax YTM = ----------------------

0.6x 60 + 0.4 x 96

= 17. 47%

7.

14 6 100

P = ∑ +

t=1 (1.08) t

(1.08)14

= Rs.6 x PVIFA(8%, 14) + Rs.100 x PVIF (8%, 14)

= Rs.6 x 8.244 + Rs.100 x 0.341

= Rs.83.56

8. Do = Rs.2.00, g = 0.06, r = 0.12

Po = D1 / (r – g) = Do (1 + g) / (r – g)

= Rs.2.00 (1.06) / (0.12 - 0.06)

= Rs.35.33

Since the growth rate of 6% applies to dividends as well as market price, the market

price at the end of the 2nd

year will be:

P2 = Po x (1 + g)2

= Rs.35.33 (1.06)2

= Rs.39.70

13](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-13-320.jpg)

![= 330 + 300 + 240 + 280

= Rs.1,150

Standard deviation of the return = [(1,100 – 1,150)2

x 0.3 + (1,000 – 1,150)2

x

0.3 + (1,200 – 1,150)2

x 0.2 + (1,400 – 1,150)2

x 0.2]1/2

= Rs.143.18

(b) For Rs.1,000, 20 shares of Beta’s stock can be acquired. The probability distribution of the

return on 20 shares is:

Economic condition Return (Rs) Probability

High growth 20 x 75 = 1,500 0.3

Low growth 20 x 65 = 1,300 0.3

Stagnation 20 x 50 = 1,000 0.2

Recession 20 x 40 = 800 0.2

Expected return = (1,500 x 0.3) + (1,300 x 0.3) + (1,000 x 0.2) + (800 x 0.2)

= Rs.1,200

Standard deviation of the return = [(1,500 – 1,200)2

x .3 + (1,300 – 1,200)2

x .3

+ (1,000 – 1,200)2

x .2 + (800 – 1,200)2

x .2]1/2

= Rs.264.58

(c ) For Rs.500, 10 shares of Alpha’s stock can be acquired; likewise for Rs.500, 10

shares of Beta’s stock can be acquired. The probability distribution of this option is:

Return (Rs) Probability

(10 x 55) + (10 x 75) = 1,300 0.3

(10 x 50) + (10 x 65) = 1,150 0.3

(10 x 60) + (10 x 50) = 1,100 0.2

(10 x 70) + (10 x 40) = 1,100 0.2

Expected return = (1,300 x 0.3) + (1,150 x 0.3) + (1,100 x 0.2) +

(1,100 x 0.2)

= Rs.1,175

Standard deviation = [(1,300 –1,175)2

x 0.3 + (1,150 – 1,175)2

x 0.3 +

(1,100 – 1,175)2

x 0.2 + (1,100 – 1,175)2

x 0.2 ]1/2

= Rs.84.41

d. For Rs.700, 14 shares of Alpha’s stock can be acquired; likewise for Rs.300, 6

shares of Beta’s stock can be acquired. The probability distribution of this

option is:

18](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-18-320.jpg)

![Return (Rs) Probability

(14 x 55) + (6 x 75) = 1,220 0.3

(14 x 50) + (6 x 65) = 1,090 0.3

(14 x 60) + (6 x 50) = 1,140 0.2

(14 x 70) + (6 x 40) = 1,220 0.2

Expected return = (1,220 x 0.3) + (1,090 x 0.3) + (1,140 x 0.2) + (1,220 x 0.2)

= Rs.1,165

Standard deviation = [(1,220 – 1,165)2

x 0.3 + (1,090 – 1,165)2

x 0.3 +

(1,140 – 1,165)2

x 0.2 + (1,220 – 1,165)2

x 0.2]1/2

= Rs.57.66

The expected return to standard deviation of various options are as follows :

Option

Expected return

(Rs)

Standard deviation

(Rs)

Expected / Standard

return deviation

a 1,150 143 8.04

b 1,200 265 4.53

c 1,175 84 13.99

d 1,165 58 20.09

Option `d’ is the most preferred option because it has the highest return to risk ratio.

3. Expected rates of returns on equity stock A, B, C and D can be computed as follows:

A: 0.10 + 0.12 + (-0.08) + 0.15 + (-0.02) + 0.20 = 0.0783 = 7.83%

6

B: 0.08 + 0.04 + 0.15 +.12 + 0.10 + 0.06 = 0.0917 = 9.17%

6

C: 0.07 + 0.08 + 0.12 + 0.09 + 0.06 + 0.12 = 0.0900 = 9.00%

6

D: 0.09 + 0.09 + 0.11 + 0.04 + 0.08 + 0.16 = 0.095 = 9.50%

6

(a) Return on portfolio consisting of stock A = 7.83%

(b) Return on portfolio consisting of stock A and B in equal

proportions = 0.5 (0.0783) + 0.5 (0.0917)

= 0.085 = 8.5%

19](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-19-320.jpg)

![+ 40000 x PVIF (15,4)

+ 30000 x PVIF (15,5)

= 122646 (A)

Investment = 100,000 (B)

Benefit cost ratio = 1.23 [= (A) / (B)]

8. The NPV’s of the three projects are as follows:

Project

P Q R

Discount rate

0% 400 500 600

5% 223 251 312

10% 69 40 70

15% - 66 - 142 - 135

25% - 291 - 435 - 461

30% - 386 - 555 - 591

9. NPV profiles for Projects P and Q for selected discount rates are as follows:

(a)

Project

P Q

Discount rate (%)

0 2950 500

5 1876 208

10 1075 - 28

15 471 - 222

20 11 - 382

b) (i) The IRR (r ) of project P can be obtained by solving the following

equation for `r’.

-1000 -1200 x PVIF (r,1) – 600 x PVIF (r,2) – 250 x PVIF (r,3)

+ 2000 x PVIF (r,4) + 4000 x PVIF (r,5) = 0

Through a process of trial and error we find that r = 20.13%

(ii) The IRR (r') of project Q can be obtained by solving the following equation for r'

32](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-32-320.jpg)

![MIRR = 11.62%

10

(a) Project A

NPV at a cost of capital of 12%

= - 100 + 25 x PVIFA (12,6)

= Rs.2.79 million

IRR (r ) can be obtained by solving the following equation for r.

25 x PVIFA (r,6) = 100

i.e., r = 12,98%

Project B

NPV at a cost of capital of 12%

= - 50 + 13 x PVIFA (12,6)

= Rs.3.45 million

IRR (r') can be obtained by solving the equation

13 x PVIFA (r',6) = 50

i.e., r' = 14.40% [determined through a process of trial and error]

(b) Difference in capital outlays between projects A and B is Rs.50 million

Difference in net annual cash flow between projects A and B is Rs.12 million.

NPV of the differential project at 12%

= -50 + 12 x PVIFA (12,6)

= Rs.3.15 million

IRR (r'') of the differential project can be obtained from the equation

12 x PVIFA (r'', 6) = 50

i.e., r'' = 11.53%

11

(a) Project M

The pay back period of the project lies between 2 and 3 years. Interpolating in

this range we get an approximate pay back period of 2.63 years/

Project N

The pay back period lies between 1 and 2 years. Interpolating in this range we

get an approximate pay back period of 1.55 years.

34](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-34-320.jpg)

![(c) Accounting break even point (under ‘expected’ scenario)

Fixed costs + depreciation = Rs. 45 million

Contribution margin ratio = 60 / 200 = 0.3

Break even level of sales = 45 / 0.3 = Rs.150 million

Financial break even point (under ‘xpected’ scenario)

i. Annual net cash flow = 0.7143 [ 0.3 x sales – 45 ] + 25

= 0.2143 sales – 7.14

ii. PV (net cash flows) = [0.2143 sales – 7.14 ] x PVIFA (13,10)

= 1.1628 sales – 38.74

iii. Initial investment = 200

iv. Financial break even level

of sales = 238.74 / 1.1628 = Rs.205.31 million

2.

(a) Sensitivity of NPV with respect to quantity manufactured and sold:

(in Rs)

Pessimistic Expected Optimistic

Initial investment 30000 30000 30000

Sale revenue 24000 42000 54000

Variable costs 16000 28000 36000

Fixed costs 3000 3000 3000

Depreciation 2000 2000 2000

Profit before tax 3000 9000 13000

Tax 1500 4500 6500

Profit after tax 1500 4500 6500

Net cash flow 3500 6500 8500

NPV at a cost of

capital of 10% p.a

and useful life of

5 years -16732 - 5360 2222

(b) Sensitivity of NPV with respect to variations in unit price.

Pessimistic Expected Optimistic

Initial investment 30000 30000 30000

Sale revenue 28000 42000 70000

44](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-44-320.jpg)

![= 5.8

A3 = 3 x 0.3 + 4 x 0.5 + 5 x 0.2

= 3.9

NPV = 4.7 / 1.1 +5.8 / (1.1)2

+ 3.9 / (1.1)3

– 10

= Rs.2.00 million

σ1

2

= 0.41

σ2

2

= 0.56

σ3

2

= 0.49

σ1

2

σ2

2

σ3

2

σ2

NPV = + +

(1.1)2

(1.1)4

(1.1)6

= 1.00

σ (NPV) = Rs.1.00 million

4. Expected NPV

4 At

= ∑ - 25,000

t=1 (1.08)t

= 12,000/(1.08) + 10,000 / (1.08)2

+ 9,000 / (1.08)3

+ 8,000 / (1.08)4

– 25,000

= [ 12,000 x .926 + 10,000 x .857 + 9,000 x .794 + 8,000 x .735]

- 25,000

= 7,708

Standard deviation of NPV

4 σt

∑

t=1 (1.08)t

= 5,000 / (1.08) + 6,000 / (1.08)2

+ 5,000 / (1,08)3

+ 6,000 / (1.08)4

= 5,000 x .926 + 6,000 x .857 + 5000 x .794 + 6,000 x .735

= 18,152

5. Expected NPV

46](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-46-320.jpg)

![4 At

= ∑ - 10,000 …. (1)

t=1 (1.06)t

A1 = 2,000 x 0.2 + 3,000 x 0.5 + 4,000 x 0.3

= 3,100

A2 = 3,000 x 0.4 + 4,000 x 0.3 + 5,000 x 0.3

= 3,900

A3 = 4,000 x 0.3 + 5,000 x 0.5 + 6,000 x 0.2

= 4,900

A4 = 2,000 x 0.2 + 3,000 x 0.4 + 4,000 x 0.4

= 3,200

Substituting these values in (1) we get

Expected NPV = NPV

= 3,100 / (1.06)+ 3,900 / 1.06)2

+ 4,900 / (1.06)3

+ 3,200 / (1,06)4

- 10,000 = Rs.3,044

The variance of NPV is given by the expression

4 σ2

t

σ2

(NPV) = ∑ …….. (2)

t=1 (1.06)2t

σ1

2

= [(2,000 – 3,100)2

x 0.2 + (3,000 – 3,100)2

x 0.5

+ (4,000 – 3,100)2

x 0.3]

= 490,000

σ2

2

= [(3,000 – 3,900)2

x 0.4 + (4,000 – 3,900)2

x 0.3

+ (5,000 – 3900)2

x 0.3]

= 690,000

σ3

2

= [(4,000 – 4,900)2

x 0.3 + (5,000 – 4,900)2

x 0.5

+ (6,000 – 4,900)2

x 0.2]

= 490,000

σ4

2

= [(2,000 – 3,200)2

x 0.2 + (3,000 – 3,200)2

x 0.4

+ (4,000 – 3200)2

x 0.4]

= 560,000

47](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-47-320.jpg)

![Substituting these values in (2) we get

490,000 / (1.06)2

+ 690,000 / (1.06)4

+ 490,000 / (1.06)6

+ 560,000 / (1.08)8

[ 490,000 x 0.890 + 690,000 x 0.792

+ 490,000 x 0.705 + 560,000 x 0.627 ]

= 1,679,150

σ NPV= 1,679,150 = Rs.1,296

NPV – NPV 0 - NPV

Prob (NPV < 0) = Prob. <

σ NPV σ NPV

0 – 3044

= Prob Z <

1296

= Prob (Z < -2.35)

The required probability is given by the shaded area in the following normal curve.

P (Z < - 2.35) = 0.5 – P (-2.35 < Z < 0)

= 0.5 – P (0 < Z < 2.35)

= 0.5 – 0.4906

= 0.0094

So the probability of NPV being negative is 0.0094

Prob (P1 > 1.2) Prob (PV / I > 1.2)

Prob (NPV / I > 0.2)

Prob. (NPV > 0.2 x 10,000)

Prob (NPV > 2,000)

Prob (NPV >2,000)= Prob (Z > 2,000- 3,044 / 1,296)

Prob (Z > - 0.81)

The required probability is given by the shaded area of the following normal

curve:

P(Z > - 0.81) = 0.5 + P(-0.81 < Z < 0)

= 0.5 + P(0 < Z < 0.81)

= 0.5 + 0.2910

= 0.7910

So the probability of P1 > 1.2 as 0.7910

48](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-48-320.jpg)

![6. Given values of variables other than Q, P and V, the net present value model of Bidhan

Corporation can be expressed as:

[Q(P – V) – 3,000 – 2,000] (0.5)+ 2,000 0

5

NPV ∑ + - 30,000

t =1 (1.1)t

(1.1)5

0.5 Q (P – V) – 500

5

∑ = ------------------------------------ - 30,000

t=1 (1.1)t

= [ 0.5Q (P – V) – 500] x PVIFA (10,5) – 30,000

= [0.5Q (P – V) – 500] x 3.791 – 30,000

= 1.8955Q (P – V) – 31,895.5

Exhibit 1 presents the correspondence between the values of exogenous variables and the two

digit random number. Exhibit 2 shows the results of the simulation.

Exhibit 1

Correspondence between values of exogenous variables and

two digit random numbers

QUANTITY PRICE VARIABLE COST

Valu

e

Pro

b

Cumulati

ve Prob.

Two digit

random

numbers Valu

e

Pro

b

Cumulati

ve Prob.

Two digit

random

numbers Value Pro

b

Cum

u-

lative

Prob.

Two digit

random

numbers

800 0.1

0

0.10 00 to 09 20 0.4

0

0.40 00 to 39 15 0.3

0

0.30 00 to 29

1,00

0

0.1

0

0.20 10 to 19 30 0.4

0

0.80 40 to 79 20 0.5

0

0.80 30 to 79

1,20

0

0.2

0

0.40 20 to 39 40 0.1

0

0.90 80 to 89 40 0.2

0

1.00 80 to 99

1,40

0

0.3

0

0.70 40 to 69 50 0.1

0

1.00 90 to 99

1,60

0

0.2

0

0.90 70 to 89

1,80

0

0.1

0

1.00 90 to 99

49](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-49-320.jpg)

![31 52 1,400 61 30 58 20 -5,359

32 76 1,600 18 20 41 20 -31,896

33 43 1,400 04 20 49 20 -31,896

34 70 1,600 11 20 59 20 -31,896

35 67 1,400 35 20 26 15 -18,627

36 26 1,200 63 30 22 15 2,224

QUANTITY (Q) PRICE (P) VARIABLE COST (V) NPV

Ru

n

Random

Number

Corre

s-

pondi

ng

Value

Random

Number

Corres-

ponding

value

Rando

m

Numbe

r

Corres-

pondin

g value

1.8955 Q(P-V)-

31,895.5

37 89 1,600 86 40 59 20 28,761

38 94 1,800 00 20 25 15 -14,836

39 09 .800 15 20 29 15 -24,314

40 44 1,400 84 40 21 15 34,447

41 98 1,800 23 20 79 20 -31,896

42 10 1,000 53 30 77 20 -12,941

43 38 1,200 44 30 31 20 -9,150

44 83 1,600 30 20 10 15 -16,732

45 54 1,400 71 30 52 20 -5,359

46 16 1,000 70 30 19 15 -3,463

47 20 1,200 65 30 87 40 -54,642

48 61 1,400 61 30 70 20 -5,359

49 82 1,600 48 30 97 40 -62,224

50 90 1,800 50 30 43 20 2,224

Expected NPV = NPV

50

= 1/ 50 ∑ NPVi

i=1

= 1/50 (-7,20,961)

= 14,419

50

Variance of NPV = 1/50 ∑ (NPVi – NPV)2

i=1

= 1/50 [27,474.047 x 106

]

= 549.481 x 106

51](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-51-320.jpg)

![Standard deviation of NPV = 549.481 x 106

= 23,441

7. To carry out a sensitivity analysis, we have to define the range and the most likely values of

the variables in the NPV Model. These values are defined below

Variable Range Most likely value

I Rs.30,000 – Rs.30,000 Rs.30,000

k 10% - 10% 10%

F Rs.3,000 – Rs.3,000 Rs.3,000

D Rs.2,000 – Rs.2,000 Rs.2,000

T 0.5 – 0.5 0.5

N 5 – 5 5

S 0 – 0 0

Q Can assume any one of the values - 1,400*

800, 1,000, 1,200, 1,400, 1,600 and 1,800

P Can assume any of the values 20, 30, 30**

40 and 50

V Can assume any one of the values 20*

15,20 and 40

----------------------------------------------------------------------------------------

* The most likely values in the case of Q, P and V are the values that have the

highest probability associated with them

** In the case of price, 20 and 30 have the same probability of occurrence viz 0.4. We

have chosen 30 as the most likely value because the expected value of the

distribution is closer to 30

Sensitivity Analysis with Reference to Q

The relationship between Q and NPV given the most likely values of other

variables is given by

5 [Q (30-20) – 3,000 – 2,000] x 0.5 + 2,000 0

NPV = ∑ + - 30,000

t=1 (1.1)t

(1.1)5

5 5Q - 500

= ∑ - 30,000

t=1 (1.1)t

The net present values for various values of Q are given in the following table:

52](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-52-320.jpg)

![Q 800 1,000 1,200 1,400 1,600 1,800

NPV -16,732 -12,941 -9,150 -5,359 -1,568 2,224

Sensitivity analysis with reference to P

The relationship between P and NPV, given the most likely values of other variables is defined as

follows:

5 [1,400 (P-20) – 3,000 – 2,000] x 0.5 + 2,000 0

NPV = ∑ + - 30,0

t=1 (1.1)t

(1.1)5

5 700 P – 14,500

= ∑ - 30,000

t=1 (1.1)t

The net present values for various values of P are given below :

P (Rs) 20 30 - 40 50

NPV(Rs) -31,896 -5,359 21,179 47,716

8. NPV - 5 0 5 10 15 20

(Rs.in lakhs)

PI 0.9 1.00 1.10 1.20 1.30 1.40

Prob. 0.02 0.03 0.10 0.40 0.30 0.15

6

Expected PI = PI = ∑ (PI)j Pj

j=1

= 1.24

6

Standard deviation of P1 = ∑ (PIj - PI) 2

Pj

j=1

= √ .01156

= .1075

The standard deviation of P1 is .1075 for the given investment with an expected PI of 1.24.

The maximum standard deviation of PI acceptable to the company for an investment with an

expected PI of 1.25 is 0.30.

53](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-53-320.jpg)

![6,580 7,040 7,380 7,600 5,600

+ + + +

(1.08) (1.08)2

(1.08)3

(1.08)4

(1.08)5

= 27,386

Net present value of the Project = (27,386 – 30,000

= Rs. –2,614

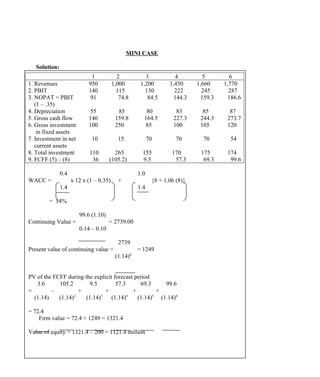

MINICASE

Solution:

1. The expected NPV of the turboprop aircraft

0.65 (5500) + 0.35 (500)

NPV = - 11000 +

(1.12)

0.65 [0.8 (17500) + 0.2 (3000)] + 0.35 [0.4 (17500) + 0.6 (3000)]

+

(1.12)2

= 2369

2. If Southern Airways buys the piston engine aircraft and the demand in year 1 turns out to be

high, a further decision has to be made with respect to capacity expansion. To evaluate the

piston engine aircraft, proceed as follows:

First, calculate the NPV of the two options viz., ‘expand’ and ‘do not expand’ at decision

point D2:

0.8 (15000) + 0.2 (1600)

Expand : NPV = - 4400 +

1.12

= 6600

0.8 (6500) + 0.2 (2400)

Do not expand : NPV =

1.12

= 5071

55](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-55-320.jpg)

![Second, truncate the ‘do not expand’ option as it is inferior to the ‘expand’ option. This

means that the NPV at decision point D2 will be 6600

Third, calculate the NPV of the piston engine aircraft option.

0.65 (2500+6600) + 0.35 (800)

NPV = – 5500 +

1.12

0.35 [0.2 (6500) + 0.8 (2400)]

+

(1.12)2

= – 5500 + 5531 + 898 = 929

3. The value of the option to expand in the case of piston engine aircraft

If Southern Airways does not have the option of expanding capacity at the end of year 1, the

NPV of the piston engine aircraft would be:

0.65 (2500) + 0.35 (800)

NPV = – 5500 +

1.12

0.65 [0.8 (6500) + 0.2 (2400)] + 0.35 [0.2 (6500) + 0.8 (2400)]

+

(1.12)2

= - 5500 + 1701 + 3842 = 43

Thus the option to expand has a value of 929 – 43 = 886

4. Value of the option to abandon if the turboprop aircraft can be sold for 8000 at the end of year

1

If the demand in year 1 turns out to be low, the payoffs for the ‘continuation’ and

‘abandonment’ options as of year 1 are as follows.

0.4 (17500) + 0.6 (3000)

Continuation: = 7857

1.12

56](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-56-320.jpg)

![Abandonment : 8000

Thus it makes sense to sell off the aircraft after year 1, if the demand in year 1 turns out to be

low.

The NPV of the turboprop aircraft with abandonment possibility is

0.65 [5500 +{0.8 (17500) + 0.2 (3000)}/ (1.12)] + 0.35 (500 +8000)

NPV = - 11,000 +

(1.12)

12048 + 2975

= - 11,000 + = 2413

1.12

Since the turboprop aircraft without the abandonment option has a value of 2369, the

value of the abandonment option is : 2413 – 2369 = 44

5. The value of the option to abandon if the piston engine aircraft can be sold for 4400 at the

end of year 1:

If the demand in year 1 turns out to be low, the payoffs for the ‘continuation’ and

‘abandonment’ options as of year 1 are as follows:

0.2 (6500) + 0.8 (2400)

Continuation : = 2875

1.12

Abandonment : 4400

Thus, it makes sense to sell off the aircraft after year 1, if the demand in year 1 turns out to

be low.

The NPV of the piston engine aircraft with abandonment possibility is:

0.65 [2500 + 6600] + 0.35 [800 + 4400]

NPV = - 5500 +

1.12

5915 + 1820

= - 5500 + = 1406

1.12

For the piston engine aircraft the possibility of abandonment increases the NPV

57](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-57-320.jpg)

![= 7.35 + 0.75 + 2.22

= 10.32%

g. Cost of capital for the new business

0.5 [7 + 1.5 (7)] + 0.5 [ 11 (1 – 0.3)]

8.75 + 3.85

= 12.60%

64](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-64-320.jpg)

![Chapter 15

CAPITAL BUDGETING : EXTENSIONS

1. EAC

(Plastic Emulsion) = 300000 / PVIFA (12,7)

= 300000 / 4.564

= Rs.65732

EAC

(Distemper Painting) = 180000 / PVIFA (12,3)

= 180000 / 2.402

= Rs.74938

Since EAC of plastic emulsion is less than that of distemper painting, it is the preferred

alternative.

2. PV of the net costs associated with the internal transportation system

= 1 500 000 + 300 000 x PVIF (13,1) + 360 000 x PVIF (13,2)

+ 400 000 x PVIF (13,3) + 450 000 x PVIF (13,4)

+ 500 000 x PVIF (13,5) - 300 000 x PVIF (13,5)

= 2709185

EAC of the internal transportation system

= 2709185 / PVIFA (13,5)

= 2709185 / 3.517

= Rs.770 311

3. EAC [ Standard overhaul]

= 500 000 / PVIFA (14,6)

= 500 000 / 3.889

= Rs.128568 ……… (A)

EAC [Less costly overhaul]

= 200 000 / PVIFA (14,2)

= 200 000 / 1.647

= Rs.121433 ……… (B)

Since (B) < (A), the less costly overhaul is preferred alternative.

65](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-65-320.jpg)

![4.

(a) Base case NPV

= -12,000,000 + 3,000,000 x PVIFA (20,6)

= -12,000,000 + 997,8000

= (-) Rs.2,022,000

(b) Issue costs = 6,000,000 / 0.88 - 6,000,000

= Rs.818 182

Adjusted NPV after adjusting for issue costs

= - 2,022,000 – 818,182

= - Rs.2,840,182

(c) The present value of interest tax shield is calculated below :

Year Debt outstanding at Interest Tax shield Present value of

the beginning tax shield

1 6,000,000 1,080,000 324,000 274,590

2 6,000,000 1,080,000 324,000 232,697

3 5,250,000 945,000 283,000 172,538

4 4,500,000 810,000 243,000 125,339

5 3,750,000 675,000 202,000 88,513

6 3,000,000 540,000 162,000 60,005

7 2,225,000 400,500 120,000 37,715

8 1,500,000 270,000 81,000 21,546

9 750,000 135,000 40,500 9,133

Present value of tax shield = Rs.1,022,076

5.

(a) Base case BPV

= - 8,000,000 + 2,000,000 x PVIFA (18,6)

= - Rs.1,004,000

(b) Adjusted NPV after adjustment for issue cost of external equity

= Base case NPV – Issue cost

= - 1,004,000 – [ 3,000,000 / 0.9 – 3,000,000]

= - Rs.1,337,333

66](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-66-320.jpg)

![1,800,000

(EBIT – 1,500,000) (1 – 0.6)

EPSB =

1,000,000

Equating EPSA and EPSB , we get

(EBIT – 0 ) (1 – 0.6) (EBIT – 1,500,000) (1 – 0.6)

=

1,800,000 1,000,000

Solving this we get EBIT = 3,375,000 or 3.375 million

Thus the debt alternative is better than the equity alternative when

EBIT > 3.375 million

EBIT – EBIT 3.375 – 7.000

Prob(EBIT>3,375,000) = Prob >

σ EBIT 3.000

= Prob [z > - 1.21]

= 0.8869

4. ROE = [ ROI + ( ROI – r ) D/E ] (1 – t )

15 = [ 14 + ( 14 – 8 ) D/E ] ( 1- 0.5 )

D/E = 2.67

5. ROE = [12 + (12 – 9 ) 0.6 ] (1 – 0.6)

= 5.52 per cent

6. 18 = [ ROI + ( ROI – 8 ) 0.7 ] ( 1 – 0.5)

ROI = 24.47 per cent

EBIT

7. a. Interest coverage ratio =

Interest on debt

150

=

40

= 3.75

EBIT + Depreciation

b. Cash flow coverage ratio =

Loan repayment instalment

75](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-75-320.jpg)

![Chapter 23

Debt Analysis and Management

1. (i) Initial Outlay

(a) Cost of calling the old bonds

Face value of the old bonds 250,000,000

Call premium 15,000,000

265,000,000

(b) Net proceeds of the new bonds

Gross proceeds 250,000,000

Issue costs 10,000,000

240,000,000

(c) Tax savings on tax-deductible expenses

Tax rate[Call premium+Unamortised issue cost on

the old bonds] 9,200,000

0.4 [ 15,000,000 + 8,000,000]

Initial outlay i(a) – i(b) – i(c) 15,800,000

(ii) Annual Net Cash Savings

(a) Annual net cash outflow on old bonds

Interest expense 42,500,000

- Tax savings on interest expense and amortisation of

issue expenses 17,400,000

0.4 [42,500,000 + 8,000,000/10]

25,100,000

(b) Annual net cash outflow on new bonds

Interest expense 37,500,000

- Tax savings on interest expense and amortisation of

issue cost 15,500,000

0.4 [ 37,500,000 – 10,000,000/8]

22,000,000

Annual net cash savings : ii(a) – ii(b) 3,100,000

82](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-82-320.jpg)

![(iii) Present Value of the Annual Cash Savings

Present value of an 8-year annuity of 3,100,000 at a

discount rate of 9 per cent which is the post –tax cost

of new bonds 3,100,000 x 5.535 17,158,500

(iv) Net Present Value of Refunding the Bonds

(a) Present value of annual cash savings 17,158,500

(b) Net initial outlay 15,800,000

(c) Net present value of refunding the bonds :

iv(a) – iv(b). 1,358,500

2. (i) Initial Outlay

(a) Cost of calling the old bonds

Face value of the old bonds 120,000,000

Call premium 4,800,000

124,800,000

(b) Net proceeds of the new issue

Gross proceeds 120,000,000

Issue costs 2,400,000

117,600,000

(c) Tax savings on tax-deductible expenses 3,120,000

Tax rate[Call premium+Unamortised issue costs on

the old bond issue]

0.4 [ 4,800,000 + 3,000,000]

Initial outlay i(a) – i(b) – i(c) 4,080,000

(ii) Annual Net Cash Savings

(a) Annual net cash out flow on old bonds

Interest expense 19,200,000

- Tax savings on interest expense and amortisation of

issue costs 7,920,000

0.4[19,200,000 + 3,000,000/5]

11,280,000

(b) Annual net cash outflow on new bonds

Interest expense 18,000,000

- Tax savings on interest expense and amortistion of issue

costs 7,392,000

0.4[18,000,000 + 2,400,000/5]

10,608,000

Annual net cash savings : ii(a) – ii(b) 672,000

(iii) Present Value of the Annual Net Cash Savings

83](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-83-320.jpg)

- k ΔI

Δ S

Δ I = x ACP x V

360

Δ S = Rs.10 million, V=0.85, bn =0.08, ACP= 60 days, k=0.15, t = 0.40

Hence, ΔRI = [ 10,000,000(1-0.85)- 10,000,000 x 0.08 ] (1-0.4)

-0.15 x 10,000,000 x 60 x 0.85

360

= Rs. 207,500

2. Δ RI = [ΔS(1-V)- ΔSbn] (1-t) – k Δ I

So ΔS

Δ I = (ACPN – ACPo) +V(ACPN)

360 360

98](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-98-320.jpg)

![ΔS=Rs.1.5 million, V=0.80, bn=0.05, t=0.45, k=0.15, ACPN=60, ACPo=45, So=Rs.15 million

Hence ΔRI = [1,500,000(1-0.8) – 1,500,000 x 0.05] (1-.45)

-0.15 (60-45) 15,000,000 + 0.8 x 60 x 1,500,000

360 360

= 123750 – 123750 = Rs. 0

3. Δ RI = [ΔS(1-V) –Δ DIS ] (1-t) + k Δ I

Δ DIS = pn(So+ΔS)dn – poSodo

So ΔS

Δ I = (ACPo-ACPN) - x ACPN x V

360 360

So =Rs.12 million, ACPo=24, V=0.80, t= 0.50, r=0.15, po=0.3, pn=0.7,

ACPN=16, ΔS=Rs.1.2 million, do=.01, dn= .02

Hence

ΔRI = [ 1,200,000(1-0.80)-{0.7(12,000,000+1,200,000).02-

0.3(12,000,000).01}](1-0.5)

12,000,000 1,200,000

+ 0.15 (24-16) - x 16 x 0.80

360 360

= Rs.79,200

4. Δ RI = [ΔS(1-V)- ΔBD](1-t) –kΔ I

ΔBD=bn(So+ΔS) –boSo

So ΔS

ΔI = (ACPN –ACPo) + x ACPN x V

360 360

So=Rs.50 million, ACPo=25, V=0.75, k=0.15, bo=0.04, ΔS=Rs.6 million,

ACPN=40 , bn= 0.06 , t = 0.3

ΔRI = [ Rs.6,000,000(1-.75) –{.06(Rs.56,000,000)-.04(Rs.50,000,000)](1-0.3)

99](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-99-320.jpg)

– kΔI

So=Rs.50 million, ΔS=Rs.10 million, do=0.02, po=0.70, dn=0.03,pn=0.60,

ACPo=20 days, ACPN=24 days, V=0.85, k=0.12 , and t = 0.40

ΔDIS = 0.60 x 60 x 0.03 – 0.70 x 50 x 0.2

= Rs.0.38 million

50 10

Δ I = (24-20) + x 24 x 0.85

360 360

= Rs.1.2222 million

Δ RI = [ 10,000,000 (1-.85) – 380,000 ] (1-.4) – 0.12 x 1,222,222

100](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-100-320.jpg)

![• Post-tax cost of capital : 12 percent

• ACP on credit sales : 20 days

Effect of Relaxing the Credit Standards on Residual Income

Incremental sales : Rs.50 million

Bad debt losses on incremental sales: 12 percent

ACP remains unchanged at 20 days

∆RI = [∆S(1 – V) - ∆Sbn] (1 – t) – R ∆ I

∆S

where ∆ I = x ACP x V

360

∆ RI = [50,000,000 (1-0.8) – 50,000,000 x 0.12] (1 – 0.3)

50,000,000

- 0.12 x x 20 x 0.8

360

= 2,800,000 – 266,667 = 2,533,333

Effect of Extending the Credit Period on Residual Income

∆ RI = [∆S(1 – V) - ∆Sbn] (1 – t) – R ∆ I

So ∆S

where ∆I = (ACPn – ACPo) + V (ACPn)

360 360

∆RI = [50,000,000 (1 – 0.8) – 50,000,000 x 0] (1 – 0.3)

800,000,000 50,000,000

- 0.12 (50 – 20) x + 0.8 x 50 x

360 360

= 7,000,000 – 8,666,667

= - Rs.1,666,667

Effect of Relaxing the Cash Discount Policy on Residual Income

∆RI = [∆S (1 – V) - ∆ DIS] (1 – t) + R ∆ I

102](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-102-320.jpg)

![where ∆ I = savings in receivables investment

So ∆S

= (ACPo – ACPn) – V x ACPn

360 360

800,000,000 20,000,000

= (20 – 16) – 0.8 x x 16

360 360

= 8,888,889 – 711,111 = 8,177,778

∆ DIS = increase in discount cost

= pn (So + ∆S) dn – po So do

= 0.7 (800,000,000 + 20,000,000) x 0.02 – 0.5 x 800,000,000 x 0.01

= 11,480,000 – 4,000,000 = 7,480,000

So, ∆RI = [20,000,000 (1 – 0.8) – 7,480,000] (1 – 0.3) + 0.12 x 8,177,778

= - 2,436,000 + 981,333

= - 1,454,667

Chapter 29

INVENTORY MANAGEMENT

1.

a. No. of Order Ordering Cost Carrying Cost Total Cost

Orders Per Quantity (U/Q x F) Q/2xPxC of Ordering

Year (Q) (where and Carrying

(U/Q) PxC=Rs.30)

Units Rs. Rs. Rs.

1 250 200 3,750 3,950

2 125 400 1,875 2,275

5 50 1,000 750 1,750

10 25 2,000 375 2,375

2 UF 2x250x200

103](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-103-320.jpg)

![b. Economic Order Quantity (EOQ) = =

PC 30

2UF = 58 units (approx)

2. a EOQ =

PC

U=10,000 , F=Rs.300, PC= Rs.25 x 0.25 =Rs.6.25

2 x 10,000 x 300

EOQ = = 980

6.25

10000

b. Number of orders that will be placed is = 10.20

980

Note that though fractional orders cannot be placed, the number of orders

relevant for the year will be 10.2 . In practice 11 orders will be placed during the year. However,

the 11th

order will serve partly(to the extent of 20 percent) the present year and partly(to the

extent of 80 per cent) the following year. So only 20 per cent of the ordering cost of the 11th

order relates to the present year. Hence the ordering cost for the present year will be 10.2 x

Rs.300

c. Total cost of carrying and ordering inventories

980

= [ 10.2 x 300 + x 6.25 ] = Rs.6122.5

2

3. U=6,000, F=Rs.400 , PC =Rs.100 x 0.2 =Rs.20

2 x 6,000 x 400

EOQ = = 490 units

20

U U Q’(P-D)C Q* PC

Δπ = UD + - F- -

Q* Q’ 2 2

6,000 6,000

= 6000 x .5 + - x 400

490 1,000

1,000 (95)0.2 490 x 100 x 0.2

- -

2 2

104](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-104-320.jpg)

![*

Note that if the DUR is 4 units with a probability of 0.3 and the LT is 5 days with

a probability of 0.6, the requirement for the combination DUR = 4 units and LT =

5 days is 20 units with a probability of 0.3x0.6 = 0.18. We have assumed that the

probability distributions of DUR and LT are independent. All other entries in the

table are derived similarly.

The normal (expected) consumption during the lead time is :

20x0.18 + 30x0.30 + 40x0.12 + 40x0.06 + 60x0.10 + 80x0.04 + 60x0.06 + 90x0.10 +

120x0.04 = 46.4 tonnes

a. Costs associated with various levels of safety stock are given below :

Safety Stock Stock out Probability Expected Carrying Total Cost

Stock* outs(in Cost Stock out Cost

tonnes)

1 2 3 4 5 6 7

[3x4] [(1)x1,000] [5+6]

Tonnes Rs. Rs. Rs.

73.6 0 0 0 0 73,600 73,600

43.6 30 120,000 0.04 4,800 43,600 48,400

33.6 10 40,000 0.10

40 160,000 0.04 10,400 33,600 44,000

13.6 20 80,000 0.04

30 120,000 0.10 24,800 13,600 38,400

60 240,000 0.04

106](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-106-320.jpg)

![(a) Key ratios for 20 X 5

12.4

Current ratio = = 0.93

13.4

8.8 + 6.7

Debt-equity ratio = = 0.98

6.5 + 9.3

57.4

Total assets turnover ratio = = 1.96

[(34 – 6.6) + (38 – 6.7)] / 2

3.0

Net profit margin = = 5.2 percent

57.4

5

Earning power = = 17.0 percent

[(34 – 6.6) + (38 – 6.7)] / 2

3.0

Return on equity = = 20.2 percent

(13.9 + 15.8) / 2

(b) Dupont Chart for 20 x 5

–

÷

122

Return on

total assets

10.2%

Net profit

margin

5.2%

Net profit

3.0

Net sales

57.4

Net sales +/-

Non-op. surplus

deficit 57.8

Total costs

54.8](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-122-320.jpg)

![5. Working capital 400 480 576 691 829 912

6. ∆Working capital 80 96 115 138 83

7. FCFF 11 13 16 19 273

(3-4-6)

Discount factor 0.876 0.767 0.672 .589

Present value 9.64 9.97 10.76 11.19

Cost of capital for the high growth period

0.4 [12% + 1.25 x 7%] + 0.6 [15% (1 - .35)]

8.3% + 5.85%

= 14.15%

Cost of capital for the stable growth period

0.5 [12% + 1.00 x 6%] + 0.5 [14% (1 - .35)]

9% + 4.55%

= 13.55%

Present value of FCFF during the explicit forecast period

= 9.64 + 9.97 + 10.76 + 11.19 = 41.56

273 273

Horizon value = = = 7690

0.1355 – 0.10 0.0355

Present value of horizon value = 4529.5

Value of the firm = 41.56 + 4529.50 = Rs.4571.06 million

3. The WACC for different periods may be calculated :

WACC in the high growth period

Year kd(1-t) = 15% (1-t) ke = Rf + β x Market risk premium ka = wd kd (1-t)+ we ke

1 15 (0.94) = 14.1% 12 + 1.3 x 7 = 21.1% 0.5 x 14.1 + 0.5 x 21.1 = 17.6%

2 15 (0.88) = 13.2% 21.1% 0.5 x 13.2 + 0.5 x 21.1 = 17.2%

3 15 (0.82) = 12.3% 21.1% 0.5 x 12.3 + 0.5 x 21.1 = 16.7%

4 15 (0.76) = 11.4% 21.1% 0.5 x 11.4 + 0.5 x 21.1 = 16.3%

5 15 (0.70) = 10.5% 21.1% 0.5 x 10.5 + 0.5 x 21.1 = 15.8%

WACC in the transition period

kd(1-t) = 14 (1 – 0.3) = 9.8%

143](https://image.slidesharecdn.com/199776069-prasanna-chandra-financial-management-220826060839-ab52aacb/85/199776069-prasanna-chandra-financial-management-pdf-143-320.jpg)

![[wacc] weighted average cost of capital](https://cdn.slidesharecdn.com/ss_thumbnails/anuragmathur-210703072911-thumbnail.jpg?width=640&height=640&fit=bounds)