Revenue expenditure provides temporary benefits within the accounting year and does not result in acquisition of an asset. It is recurring and reduces profit. Capital expenditure provides long-term benefits over several years through acquisition or improvement of an asset. It is non-recurring and does not reduce profit. The document uses examples to distinguish between capital and revenue expenditures such as wages, transportation costs, repairs, and improvements to assets.

Capital expenditure & Revenue expenditureMudassir Raza

Capital expenditures are typically one-time large purchases of fixed assets that will be used for revenue generation over a longer period. Revenue expenditures are the ongoing operating expenses, which are short-term expenses used to run the daily business operations.

Marginal costing is a costing technique wherein the marginal cost, i.e. variable cost is charged to units of cost, while the fixed cost for the period is completely written off against the contribution.

Capital expenditure & Revenue expenditureMudassir Raza

Capital expenditures are typically one-time large purchases of fixed assets that will be used for revenue generation over a longer period. Revenue expenditures are the ongoing operating expenses, which are short-term expenses used to run the daily business operations.

Marginal costing is a costing technique wherein the marginal cost, i.e. variable cost is charged to units of cost, while the fixed cost for the period is completely written off against the contribution.

The owners or the management may desire to ascertain the trading results of each department and the overall result of the organization. The method of accounting which is followed to obtain such results is known as departmental accounting.

Fund flow statement is a statement that compares the two balance sheets by analyzing the sources of funds (debt and equity capital) and the application of funds (assets) and its reasons for any differences.

This is one of the hardest topic in Accounting. To make it easier I have prepared this one. It is according to AS 7. These are some of the basics of Contract Accounting. How to account Contact?

Like if it proves to be useful for you.

Presentation on Budget, Budgeting & Budgetary control

Contents:

1) Budgeting [characteristics]

2) Budgetary control

3) Difference in budget, budgeting, budgetary control

4) Essentials in budgetary control

5) Requisites for budgetary control system

6) Merits & limitations

7) Zero-based budgeting

8) Difference in Traditional & Zero based budgeting.

1.1 identify the type of accounting

1.2 difference between Cost Accounting , Cost Accountancy and Costing

1.3 understand the Management information needs

1.4 identify the objectives of cost accounting

1.5 difference between Cost Accounting Vs. Financial Accounting

1.6 identify the role of cost accountant

The owners or the management may desire to ascertain the trading results of each department and the overall result of the organization. The method of accounting which is followed to obtain such results is known as departmental accounting.

Fund flow statement is a statement that compares the two balance sheets by analyzing the sources of funds (debt and equity capital) and the application of funds (assets) and its reasons for any differences.

This is one of the hardest topic in Accounting. To make it easier I have prepared this one. It is according to AS 7. These are some of the basics of Contract Accounting. How to account Contact?

Like if it proves to be useful for you.

Presentation on Budget, Budgeting & Budgetary control

Contents:

1) Budgeting [characteristics]

2) Budgetary control

3) Difference in budget, budgeting, budgetary control

4) Essentials in budgetary control

5) Requisites for budgetary control system

6) Merits & limitations

7) Zero-based budgeting

8) Difference in Traditional & Zero based budgeting.

1.1 identify the type of accounting

1.2 difference between Cost Accounting , Cost Accountancy and Costing

1.3 understand the Management information needs

1.4 identify the objectives of cost accounting

1.5 difference between Cost Accounting Vs. Financial Accounting

1.6 identify the role of cost accountant

Capital and Revenue Expenditure

Before preparing the financial statements of business organisation’s, we should get information about capital and income expenses and capital and income receipts, because having a clear knowledge of these helps in preparing the income statement and balance sheet.

At the end of the financial year, Final Accounts are prepared by every business, in which Trading and Profit & Loss Account and Balance Sheet are included. Items given in the trial balance are entered either in the trading and profit and loss account or in the balance sheet. For this, it is very important to divide the items given in the trial balance into income and capital, because all the income items given in the balance sheet ie income expenditure and income receipts are written in the business and profit and loss account, while all the capital expenditure and capital receipts are written in the balance sheet. (Position Details) are written in.

Therefore, before preparing the final accounts, it is very necessary to divide the items of trial balance into capital and income. Due to wrong classification of any item into capital and income, the amount of profit or loss reported by the profit and loss account will be wrong and the balance sheet will also not give the correct and proper financial position as on that date.

Classification of Expenditure

Expenses can be divided into three categories :

Expenditure

1. Capital Expenditure

2. Revenue Expenditure

3. Deferred Revenue Expenditure

Is accounting troubling you? Are you confused about accounting concepts and standards? Our experts follow analytical approach to resolve accounting problems in proper and efficient manner for better understanding and improved grades. Browse our website to know more on accounting assignment help.

1Acquisition cost of long-lived assets the following items repr.docxfelicidaddinwoodie

1

Acquisition cost of long-lived assets: the following items represent expenditures (or receipts) related to construction of a new home office for Lowery company.

Cost of land site, which include an old apartment building appraised at $75,000 $165,000

Legal fees, including fee for title search $2100

Payment of apartment building mortgage and related interest due at time of sale $9300

Payment for delinquent property taxes assumed by the purchaser $4000

Cost of razing the apartment building $17,000

Proceeds from sale of salvaged materials ($3800)

Grading to establish proper drainage flow on land site $1900

Architects fee on new building $300,000

Proceeds from sales of excess dirt (from basement excavation) to owner of adjoining property (that was used to fill in a low area on property) ($2000)

Payment to building contractor $5,000,000

Payment of medical bills of employee accidentally injured while inspecting building construction

$1400

Special assessment for paving city sidewalks (paid to city) $18,000

Cost of paving driveway parking lot $25,000

Cost of installing lights in parking lot $9200

Premium for insurance on building during construction $7500

Cost of open house party to celebrate the opening of new building $8000

Required

From the given data, calculate the proper balances for land, building, and land improvements accounts of Lowery Company.

2

Depreciation method: on January 2, Roth Inc. purchased a laser cutting machine to be used in the fabrication of a part for one of its key products. The machine cost $80,000, and its estimated useful life was four years or 1 million cuttings, after which it could be sold for $5000.

Required

Calculate the depreciation expense for each year of the machines useful life under each of the following depreciation methods:

a. straight-line

b. double declining balance

c. Units of production. Assume annual production and cuttings of:

a. 200,000

b. 350,000

c. 260,000

d. 190,000

3

Depreciation method: on January 2, 2012, Alvarez Company purchased an electroplating machine to help manufacture a part for one of its key products. The machine cost $218,700 and was estimated to have a useful life of six years or 700,000 pleadings, after which it could be sold for $23,400.

Required

a. calculate each year’s depreciation expense for the period 2012-2017 under each of the following depreciation methods:

1. straight-line

2. double declining balance

3. Units of production. (Assume annual production in pleadings of:

i. 140,000

ii. 180,000

iii. 100,000

iv. 110,000

v. 80,000

vi. 90,000

b. Assume that the machine was purchased on September 1, 2012. Calculate each year’s depreciation expense for the period 2012 through 2018 under each of the following depreciation methods:

1. straight-line

2. double declining balance

4

Accounting for planting and intangible assets: selected transactions of Continental publishers Inc., ...

Difference between capital expenditure and revenue expenditure

1. Difference between Capital Expenditure and

Revenue Expenditure

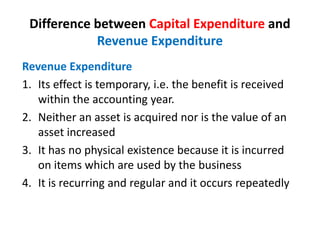

Revenue Expenditure

1. Its effect is temporary, i.e. the benefit is received

within the accounting year.

2. Neither an asset is acquired nor is the value of an

asset increased

3. It has no physical existence because it is incurred

on items which are used by the business

4. It is recurring and regular and it occurs repeatedly

2. Continued…

5. A portion of this expenditure (depreciation on

assets) is shown in trading & P & L A/c and the

balance is shown in the balance sheet on asset

side

6. This expenditure helps to maintain the business

7. The whole amount of this expenditure is shown

in trading P & L A/c or income statement

8. It does not appear in the balance sheet.

9. It reduces revenue (profit) of the business.

3. Capital Expenditure

1. Its effect is long-term, i.e. it is not exhausted within

the current accounting year-its benefit is received

for a number of years in future

2. An asset is acquired or the value of an existing asset

is increased

3. Generally it has physical existence except intangible

assets

4. It does not occur again and again. It is nonrecurring

and irregular

5. This expenditure improves the position of the

business

4. Continued…

6. It appears in the balance sheet until its

benefit is fully exhausted

7. It does not reduce the revenue of the

concern. Purchase of fixed asset does not

affect revenue.

5. Example:

State with reasons whether the following items of

expenditure are capital or revenue

• (i) Wages paid on the purchase of goods.

• (ii) Carriage paid on goods purchased.

• (iii) Transportation paid on machinery purchased.

• (iv) Duty paid on machinery.

• (v) Duty paid on goods.

6. Continued…

(vi) A second-hand car was purchased for £7,000 and

£5,000 was spent for its repairs and overhauling.

(vii) Office building was whitewashed at a cost of

£3,000.

(viii) A new machinery was purchased for £80, 000 and

a sum of £1,000 was spent on its installation and

erection.

(ix) Books were purchased for £50,000 and £1,000 was

paid for carrying books to the library.

7. Continued…

• (x) Land was purchased for £1, 00,000 and

£5,000 were paid for legal expenses.

• (xi) £50,000 was paid for customs duty and

freight on machinery purchased from Japan.

• (xii) Old furniture was repaired at a cost of

£500.

• (xiii) An additional room was constructed at a

cost of £15,000.

8. • (xiv) Damages paid on account of the breach

of contract to supply certain goods.

• (xv) Cost of replacement of an old and worn

out part of machinery.

• (xvi) Repairs to a motor car met with an

accident.

• (xvii) £10,000 paid for improving a machinery.

• (xviii) Cost of removing plant and machinery

to a new site.

8

9. Continued…

• (xix) Cost of acquiring the goodwill of an old firm.

• (xx) Cost of redecorating a cinema hall.

• (xxi) Cost of putting up a. gallery in a cinema hall.

• (xxii) Compensation paid to a director for loss of

his office.

• (xxiii) Premium paid on the redemption of

debentures.

• (xxiv) Costs of attending a mortgage.

• (xxv) Commission paid on issue of debentures.

10. Continued…

• (xxvi) Cost of air-conditioning the office of the

director of a company.

• (xxvii) Repairs and renewal of machinery.

• (xxviii) Cost of acquiring patent rights and trade

marks.

• (xxix) Compensation paid to workers for

termination of their services.

• (xxx) Compensation paid to a person injured by

company's car.

• (xxxi) Expenditures incurred on alteration in

windows ordered by local authorities.

11. • (xxxii) Painting expenditures of a newly-

constructed factory.

• (xxxiii) Expenditures incurred on renewal of

patent.

• (xxxiv) Expenditures on replacement of a slate

roof by a glass roof.

• (xxxv) £10,000 spent on

dismantling, removing and reinstalling

machinery and

fixtures.

• (xxxvi) legal expenses incurred in an income

tax appeal.