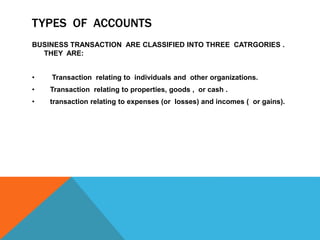

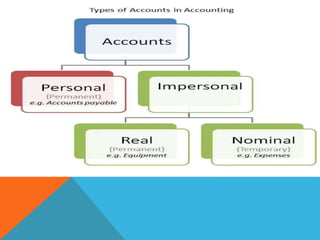

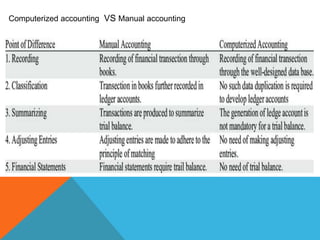

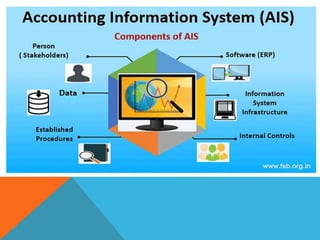

The document discusses the fundamentals of computerized accounting versus manual accounting. It explains that accounting involves systematically recording and analyzing transactions to present economic information about a business to owners and managers. This can be done through computerized accounting or manually. The principles of accounting involve recording transactions in journals and ledgers to classify accounts for individuals, properties, expenses/incomes. Computerized accounting digitizes this process for easier recording and analysis of accounting information compared to manual accounting methods.