Basis period and changes in accounting dates

•

2 likes•632 views

Basis period and changes in accounting dates

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Basis period and changes in accounting dates

Similar to Basis period and changes in accounting dates (20)

More from sakura rena

More from sakura rena (20)

Recently uploaded

Recently uploaded (20)

Basis period and changes in accounting dates

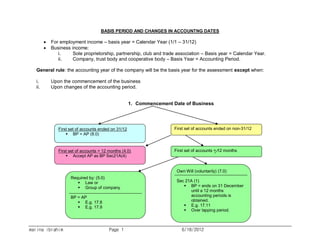

- 1. marina ibrahim Page 1 6/18/2012 BASIS PERIOD AND CHANGES IN ACCOUNTNG DATES For employment income – basis year = Calendar Year (1/1 – 31/12) Business income: i. Sole proprietorship, partnership, club and trade association – Basis year = Calendar Year. ii. Company, trust body and cooperative body – Basis Year = Accounting Period. General rule: the accounting year of the company will be the basis year for the assessment except when: i. Upon the commencement of the business ii. Upon changes of the accounting period. 1. Commencement Date of Business First set of accounts ended on 31/12 BP = AP (8.0) First set of accounts ended on non-31/12 First set of accounts = 12 months (4.0) Accept AP as BP Sec21A(4) First set of accounts = 12 months Required by: (5.0) Law or Group of company BP = AP E.g. 17.8 E.g. 17.9 Own Will (voluntarily) (7.0) Sec 21A (1) BP = ends on 31 December until a 12 months accounting periods is obtained. E.g. 17.11 Over lapping period.

- 2. marina ibrahim Page 2 6/18/2012 2. Change of Accounting Date 31 DECEMBER (10.0) NORMAL ACCOUNTING DATE NON 31 DECEMBER (9.0) Sec 21A (2) BP = ends on 31 December until a 12 months accounting periods is obtained. Over lapping period E.g. 17.22, 17.23, 17.24. New Accounts MORE than 12 months (9.1) New Accounts LESS than 12 months (9.2) A. New accounts end in the following year. AP = BP E.g.17.16 B. New accounts end in the third year. Apportion the new accounts into 2 BPs, therefore created 2 YAs. E.g. 17.17 A. New accounts end in the following year. AP = BP E.g. 17.18, 17.19, 17.20 B. New accounts & normal accounts end in the same year. New AP + Following AP. The aggregate of the above will be the BP (YA). E.g. 17.21,