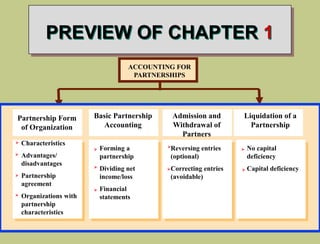

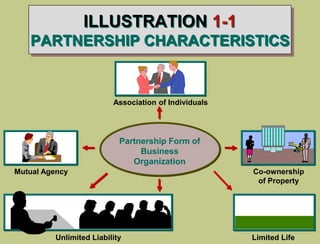

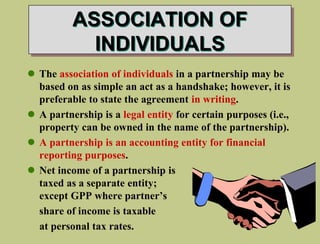

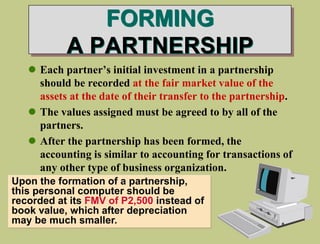

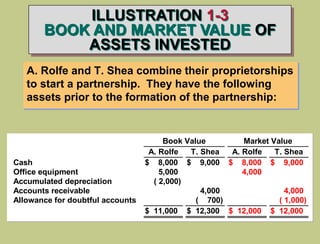

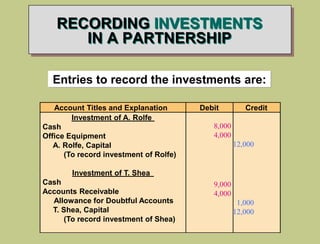

The document provides an overview of chapter 1 of the textbook "Advanced Financial Accounting and Reporting, Part 1" which covers accounting for partnerships. The chapter objectives are to understand the characteristics of partnerships, accounting entries related to forming, admitting, and withdrawing partners from a partnership, bases for dividing net income/loss, and partnership financial statements. The summary covers partnership characteristics like association of individuals, mutual agency, limited life, unlimited liability, and co-ownership of property. It also discusses the accounting entries for forming a partnership such as recording partners' investments.