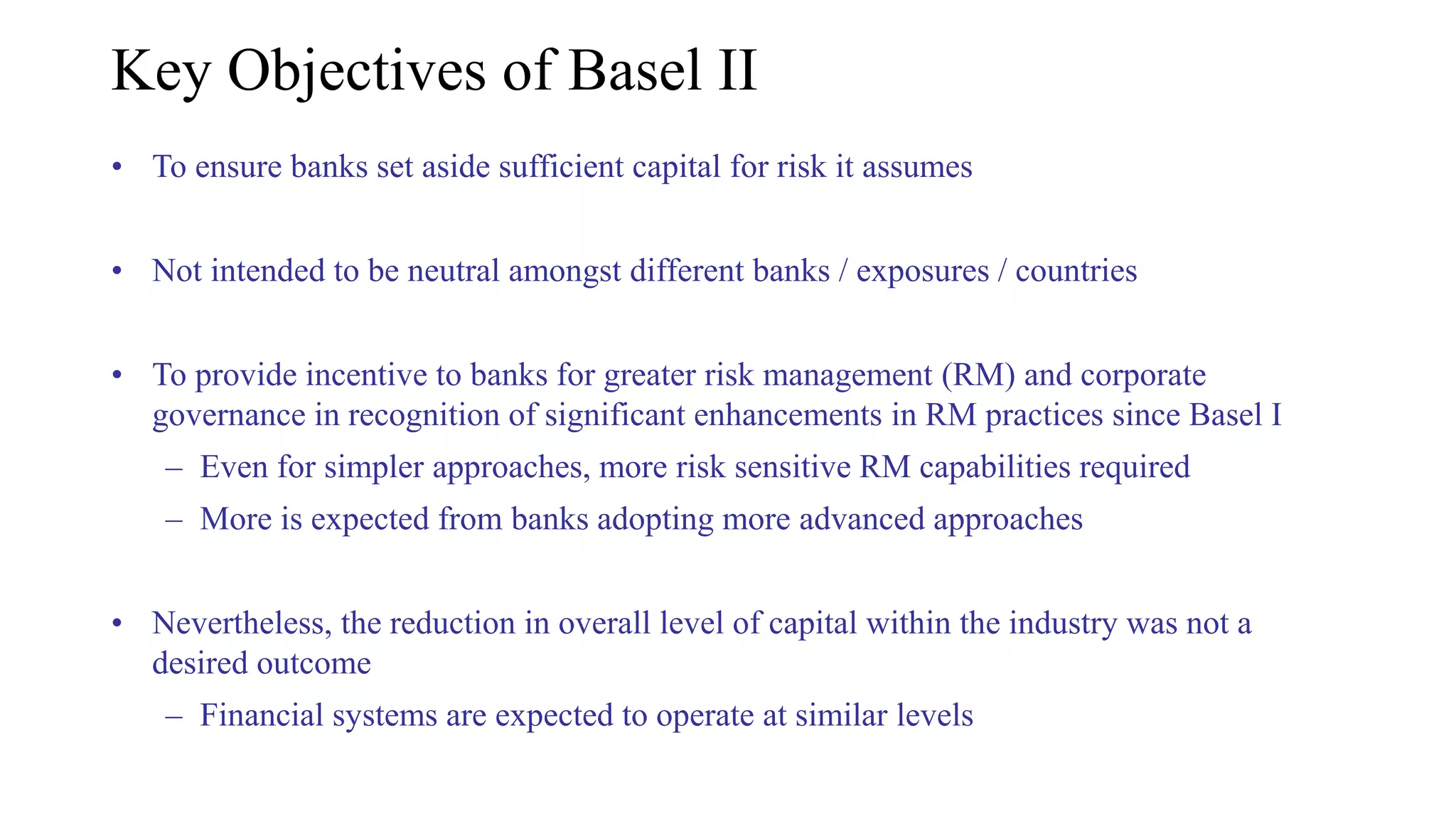

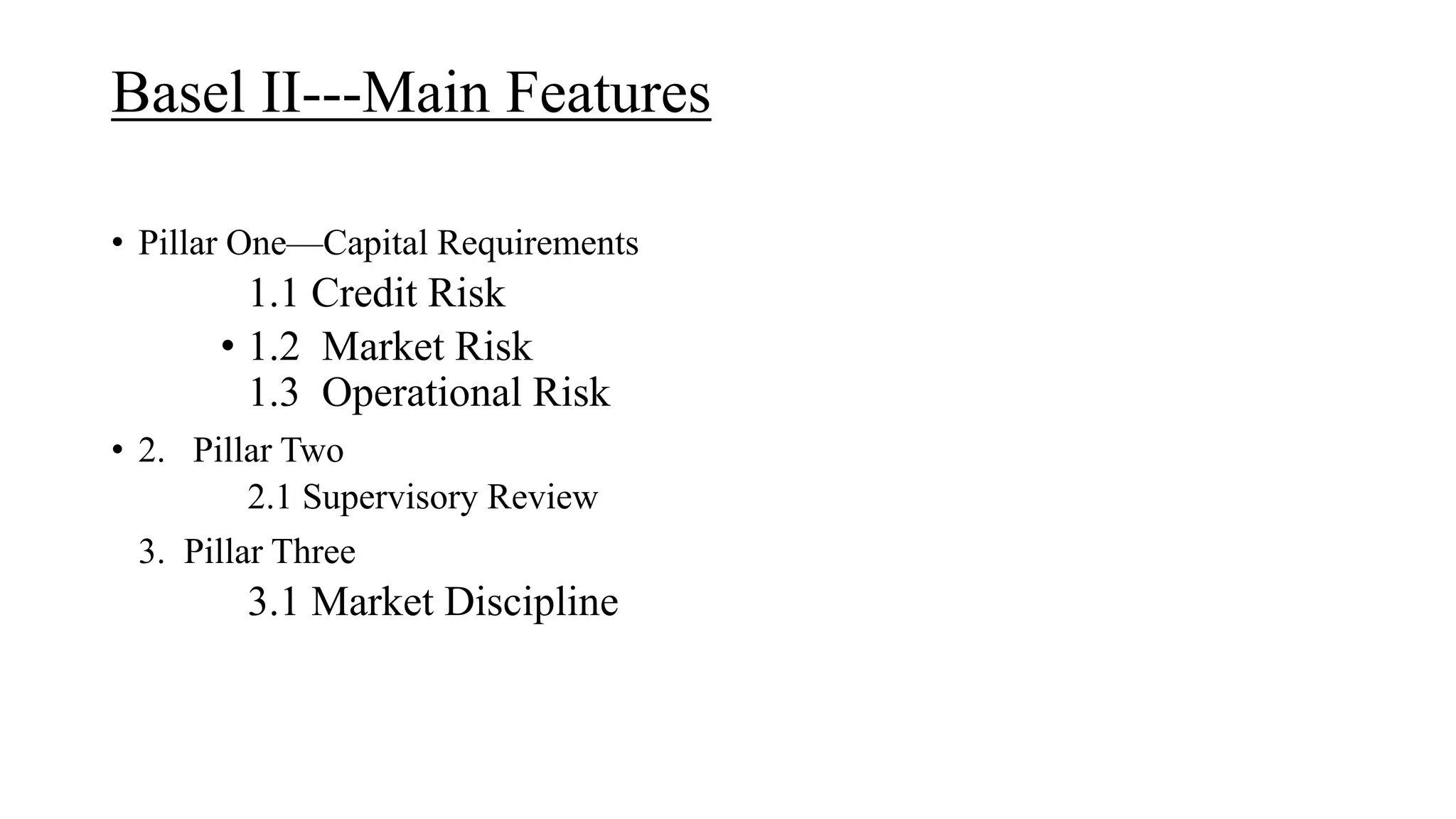

The document discusses the Basel I, II, and III frameworks aimed at ensuring banks maintain adequate capital to manage risk effectively. Basel II introduced a three-pillar framework addressing capital requirements, supervisory review, and market discipline, while Basel III emphasized improved capital quality, additional capital buffers, leverage ratios, and liquidity management. Key changes in Basel III include raising minimum capital requirements and introducing measures for systemically important financial institutions.

![Basel III, Challenges in developing countriesSV[1]](https://cdn.slidesharecdn.com/ss_thumbnails/87082c28-5f8b-4abe-8ba3-2ea11a74ebbf-170104093056-thumbnail.jpg?width=640&height=640&fit=bounds)