Downloaded 32 times

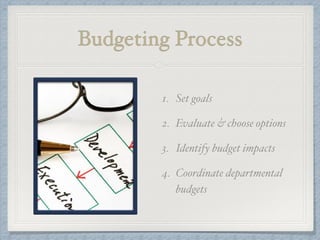

The document provides an overview of budgeting, describing it as a financial blueprint that translates strategic plans into measurable expenditures over time. It outlines the budgeting process, types of budgets (operating, capital, and cash), and different approaches such as traditional and alternate methods. Key budgeting concepts discussed include fixed and variable costs, goal setting, and variance analysis.