Downloaded 123 times

![

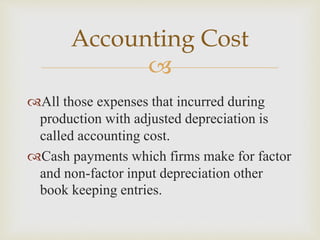

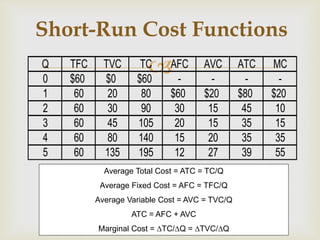

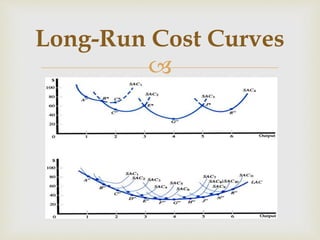

Cost Function

Long Run

Marginal

Costs (LMC)

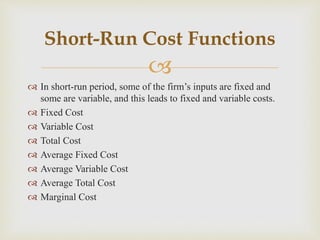

Costs According to Time Period

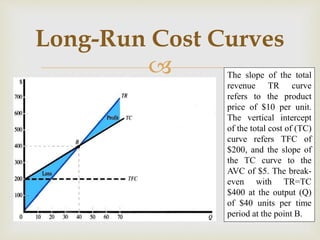

Short Run Cost Curve Long Run Cost Curve

Total Cost

(TC)

Average

Cost

(AC)

Marginal

Cost (MC)

Long Run

Total Costs

(LTC)

Long Run

Average

Costs (LAC)

Total

Fixed

Costs

(TFC)

Total

Variabl

e

Costs

(TVC)

Averag

e Fixed

Costs

(AFC)

Averag

e

Variabl

e

Costs

(AVC)

[TC =TFC+TVC] [AC = AFC+AVC]

MC = TCn – TCn-1

Or

MC = ΔTC

ΔQ](https://image.slidesharecdn.com/ecopptgroup4-160209081423/85/Economic-Presentation-Cost-Theory-and-Analysis-9-320.jpg)

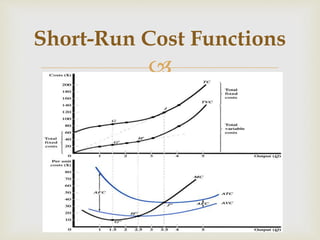

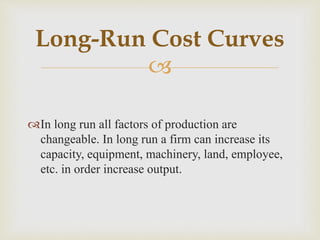

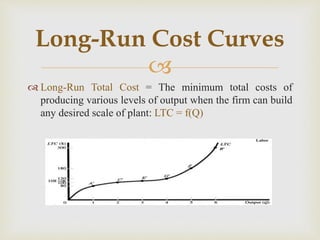

The document discusses different types of costs including: 1. Accounting costs include expenses incurred during production adjusted for depreciation, while economic costs include explicit payments to factors of production as well as implicit opportunity costs. 2. In the short-run, costs are classified as fixed, variable, total, average fixed, average variable, and marginal based on their relationship to changing output levels. 3. In the long-run, all factors are variable and long-run total, average, and marginal cost curves are defined based on minimum cost production at different output scales.