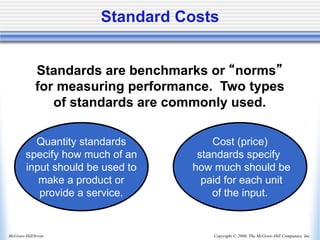

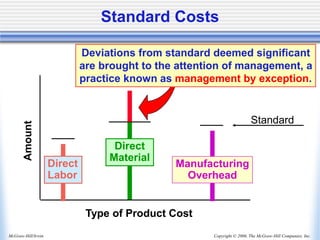

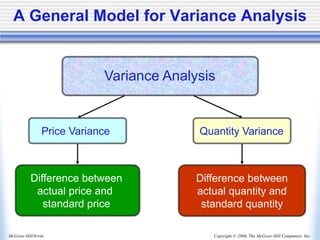

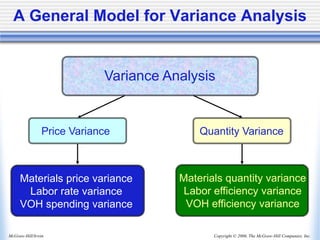

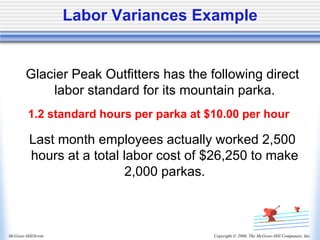

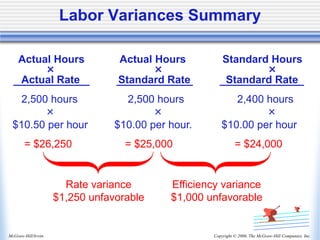

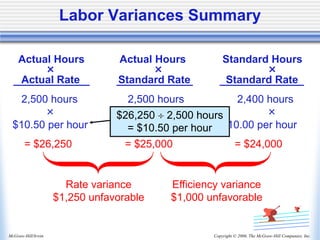

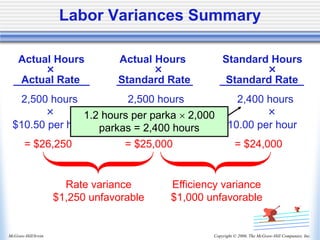

1. Standard costs are benchmarks used to measure performance against targets for inputs like direct materials, direct labor, and manufacturing overhead. Variances from standards are identified and reported.

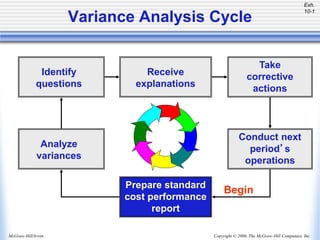

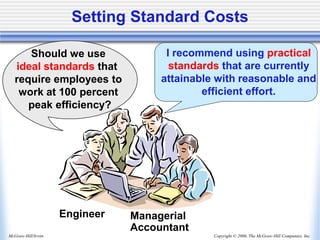

2. Managers from different departments work together to set reasonable and attainable standards for direct materials, direct labor hours and rates, and variable overhead rates and activities. Variance analysis is used to identify issues.

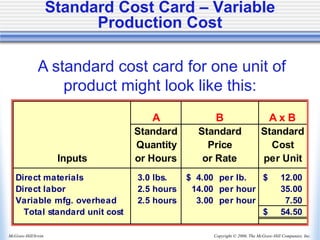

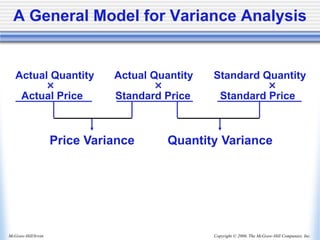

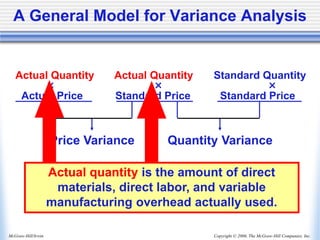

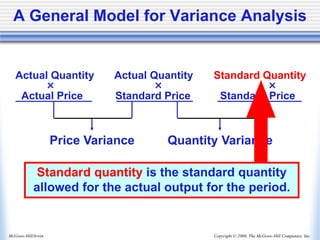

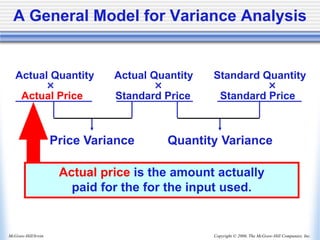

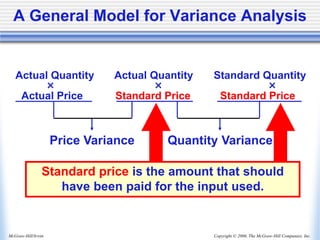

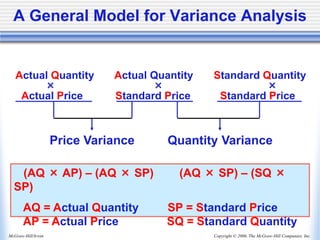

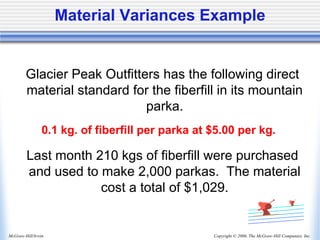

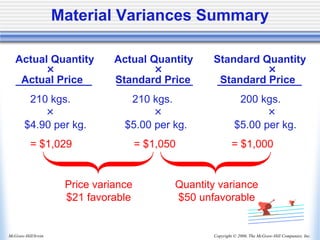

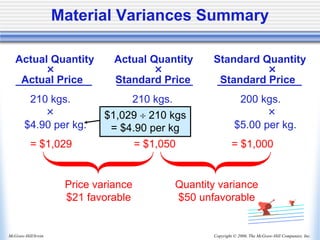

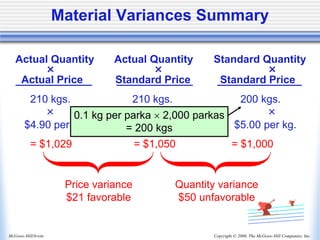

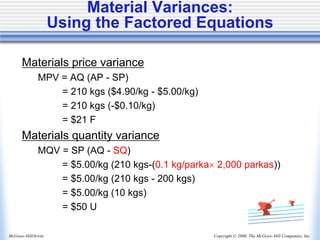

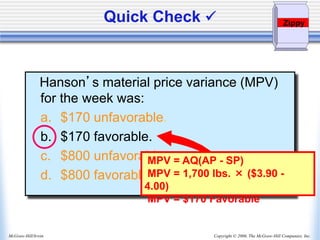

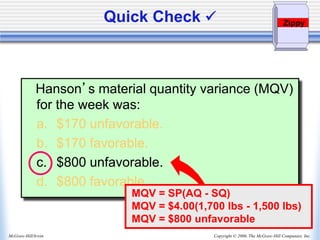

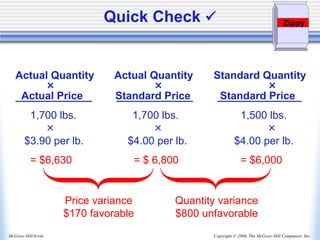

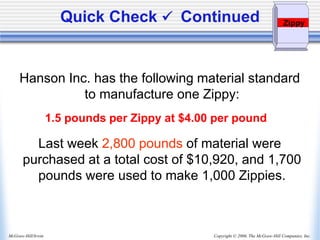

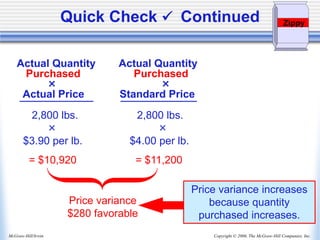

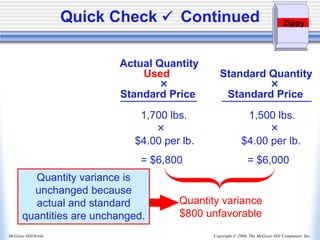

3. Material variances are calculated based on the actual quantity purchased and price paid versus the standard quantity needed and price. The price variance is calculated on total quantity purchased while the quantity variance is only on amount used in production.